|

|

PRESS RELEASE | NASDAQ: IPX | ASX: IPX

June 4, 2026

|

IPERIONX TITAN DFS CONFIRMS HIGH-RETURN U.S. RARE EARTHS AND CRITICAL MINERALS PROJECT

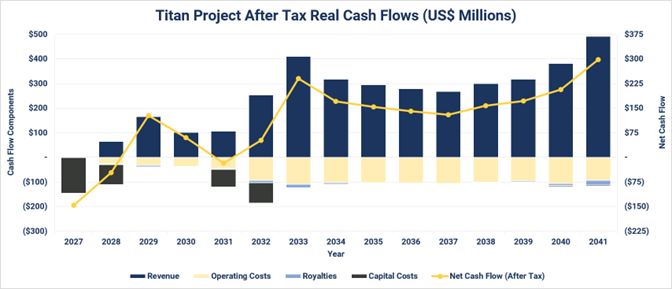

U.S. Government supported Definitive Feasibility Study delivers US$813 million after-tax NPV8, 39% IRR and US$1.9 billion after-tax free cash flow from an initial 14-year mine plan producing heavy rare earth concentrate, titanium minerals and zircon in Tennessee, U.S.A.

|

IperionX Limited (NASDAQ: IPX, ASX: IPX) (IperionX or Company) is pleased to announce the results of the Definitive Feasibility Study (DFS or Study)

for the Company’s 100%-owned Titan Critical Minerals Project (Titan or Project), located near Camden, Tennessee, United States.

The DFS confirms Titan as a large-scale, technically robust and high-return critical minerals project designed to produce titanium, zircon and a heavy rare earth concentrate from a single

domestic resource in the United States. The Study underpins an initial 14-year mine plan based entirely on Proved and Probable Ore Reserves, with no Inferred Mineral Resources included in the Production Target.

|

| ■ |

Compelling after-tax returns: DFS delivers after-tax NPV8 of US$813 million, after-tax IRR of 39% and an

after-tax payback period of 3.6 years

|

||

| ■ |

Significant

cash generation: Forecast life-of-mine EBITDA of US$2.8 billion and after-tax free cash flow of US$1.9 billion over an initial 14-year mine plan

|

||

| ■ |

Capital-efficient staged

development: Phase 1 development capital of US$228.1 million and Phase

2 incremental capital of US$153.2 million, for total development capital of US$381.3 million

|

||

|

■

|

Strong

scale-up to Phase 2 cash flow: Phase 2 forecast average annual EBITDA of US$226 million and average annual after-tax free cash flow of US$172 million.

|

||

|

■

|

Maiden

Ore Reserve: Reserves of 117 million tons at 3.2% THM, containing 3.7 million tons THM, with approximately 80% of Ore Reserves classified as Proved

|

||

|

■

|

High-value critical mineral

products: Multi-critical mineral platform for American supply-chains

from a single domestic resource base, including rare earths, titanium minerals and zircon. Phase 2 annual production forecast of approximately 5,287 tpa HREC (Heavy Rare Earth Concentrate), 118,658 tpa ilmenite, 24,656 tpa rutile and

65,668 tpa zircon concentrate

|

||

|

■

|

Heavy rare earth leverage: Titan HREC contains strategically important heavy rare earths dysprosium, terbium

and yttrium (Dy, Tb, Y) and other heavy rare earth elements representing a large share of HREC basket value. The heavy rare earths are vital for U.S. supply chains for high-performance magnets, defense, advanced ceramics, aerospace,

and semiconductor applications

|

||

|

■

|

Titanium and zircon critical

minerals: Titan is positioned as a near-term, U.S.-based critical

minerals platform for titanium and zircon critical minerals for downstream domestic metal production

|

||

|

■

|

Simple,

modular execution pathway: Titan is a near-surface, free-dig mineral sands development with no blasting or hard-rock crushing, using industry standard wet concentration, flotation and dry mineral separation

|

||

|

■

|

U.S.

infrastructure advantage: Titan Project is located in west Tennessee near road, rail, barge, power, water and gas infrastructure, with access to an established regional industrial workforce

|

||

|

■

|

U.S.

Government-supported DFS pathway: The DFS was supported under U.S. Government IBAS-related funding, reinforcing Titan’s strategic relevance to resilient domestic critical minerals and titanium supply chains for defense,

aerospace, advanced manufacturing, energy and robotics

|

||

|

■

|

Strategic

U.S. minerals-to-metals platform: Titan is positioned to underpin domestic critical mineral feedstock for U.S. heavy rare earth, titanium, zirconium and advanced materials supply chains, while complementing IperionX’s

downstream titanium metal technologies and Virginia manufacturing platform

|

||

|

Tennessee

|

Utah

|

||

|

1092 Confroy Drive

South Boston, VA 24592

|

279 West Main Street

Camden, TN 38320

|

1782 W 2300 S

West Valley City, UT 84119

|

|

|

IperionX Limited ABN 84 618 935 372

|

|||

IperionX CEO Taso Arima said:

“The Titan DFS confirms Titan as one of the most compelling, shovel-ready rare earth and critical minerals development opportunities in the United States.

The investment case is powerful: an after-tax NPV8 of US$813 million, after-tax IRR of 39.4%, US$1.9 billion of after-tax free cash flow and a 3.6-year payback. These outcomes are underpinned by key mine-area permits already in place, a Proved

and Probable Ore Reserve base, a modular staged development pathway, conventional mineral sands processing, established infrastructure and a premier U.S. critical minerals jurisdiction.

What makes Titan exceptional is the combination of strong economics, multi-critical-mineral diversity and direct relevance to U.S. supply-chain security. Titan is designed to produce a heavy rare earth concentrate enriched in dysprosium, terbium

and yttrium, together with titanium minerals and zircon concentrate. These are critical feedstocks for high-performance permanent magnets, aerospace and defense systems, semiconductors, thermal barrier coatings, nuclear materials, zirconium and

hafnium pathways, advanced ceramics and next-generation manufacturing.

Titan is the leading asset of Tennessee’s Big Sandy Critical Minerals Province — a large-scale, high-grade U.S. critical minerals system with the potential to become the largest domestic source of heavy rare earths, titanium and zircon minerals.

For IperionX, Titan is the cornerstone asset for an integrated U.S. critical minerals-to-metals strategy, connecting Tennessee rare earth and critical mineral feedstocks with downstream rare earth processing, permanent magnets, titanium metal

production and American advanced manufacturing.

Our objective is clear: to build a resilient, scalable and domestic critical minerals-to-metals platform that strengthens America’s defense industrial base, reduces reliance on foreign-controlled supply chains and creates long-term value for

IperionX shareholders.”

A copy of the Technical Report Summary (TRS), including Mineral Resources and Mineral Reserves reported for the Titan deposit using the definitions in Regulation S-K 1300 (S-K

1300), under Item 1300 promulgated by the US Securities and Exchange Commission (SEC) can be accessed here.

For further information and enquiries please contact:

info@iperionx.com

+1 980 237 8900

2

3

4

Figure 1: Key metrics from Titan DFS.

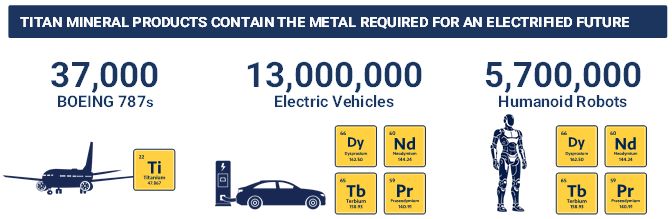

Figure 2: Titan's projected LOM production of ilmenite and rutile and HREC are estimated to contain sufficient titanium and NdPr- material to support the

production of ~37,000 Boeing 787s, ~13 million electric vehicles, and ~5.7 million humanoid robots1.

1 Figures shown are rounded. Based on Titan’s annual Phase 2 projected and LOM projected

production of titanium in ilmenite and rutile, and NdPr in HREC oxides. IPX estimates for material intensities for various end-use applications. Sources: Adamas Intelligence; Benchmark Minerals; ORNL; DoE; MDPI Minerals 2023, 13, 1274; Resources,

Conservation & Recycling (2025) 107966

5

|

METRIC

|

UNIT

|

PHASE 1

|

PHASE 2

|

|

|

Mine life

|

Years

|

1-4

|

5-14

|

|

|

Annual ore feed

|

Mt pa

|

3.5

|

10

|

|

|

Ore and waste

|

Mt

|

117.0 Mt ore; 95.6 Mt waste (strip ratio: 0.82)

|

||

|

Total development capital

|

US$

|

$228.1M

|

$153.2M

|

|

|

Operating costs

|

US$/t ore

|

$13.31

|

$10.57

|

|

|

Total LOM EBITDA

|

US$

|

$2.8B

|

||

|

Total after-tax free cash flow

|

US$

|

$1.9B

|

||

|

Phase 2 avg. annual EBITDA

|

US$ pa

|

$226M

|

||

|

Phase 2 avg. annual after-tax FCF

|

US$ pa

|

$172M

|

||

|

After-tax NPV8

|

US$

|

$813M

|

||

|

After-tax IRR

|

%

|

39.4%

|

||

|

After-tax payback period

|

Years

|

3.6

|

||

|

Phase 2 annual production

|

tpa

|

HREC: 5,287

|

||

|

Ilmenite: 118,658

|

||||

|

Rutile: 24,656

|

||||

|

Zircon concentrate.: 65,668

|

||||

Table 1: Summary DFS metrics1.

1 Units throughout the DFS are stated in metric tons

6

7

Titan Project Overview

The Titan Critical Minerals Project is IperionX’s flagship U.S. critical minerals development, located in west Tennessee approximately 80 miles west of Nashville, near the town of Camden. Titan

benefits from an established industrial setting with access to road, rail and barge logistics, power, water, gas infrastructure and a skilled regional workforce.

The Definitive Feasibility Study (DFS) confirms Titan as a large-scale, shovel-ready U.S. critical minerals asset with compelling project economics, a diversified multi-product revenue base and a

conventional execution pathway. The project is designed to produce heavy rare earth concentrate, titanium minerals and zircon concentrate from the McNairy Formation within the Big Sandy Critical Minerals Province.

IperionX commenced exploration at Titan in 2020 and has advanced the project through resource definition, technical studies, permitting and now completion of the DFS. The DFS was supported by U.S.

Government Industrial Base Analysis and Sustainment-related funding, with approximately US$5 million allocated to accelerate Titan to feasibility-study status within IperionX’s broader U.S. minerals-to-metals critical supply chain development

program.

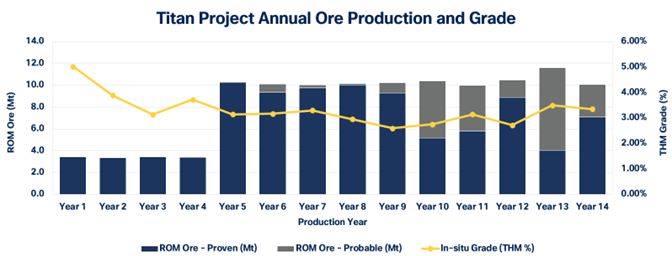

The DFS evaluates an initial 14-year mine plan and staged processing strategy. At Phase 2 run-rate, Titan is forecast to produce approximately 5,287 tpa of heavy rare

earth concentrate (HREC), 118,658 tpa of ilmenite, 24,656 tpa of rutile and 65,668 tpa of zircon concentrate.

Titan’s development plan is modular and staged. Phase 1 is designed for the initial four years of operations, followed by a scale-up to Phase 2 for the remaining ten years. The process route is

conventional and scalable, using contractor excavator-and-truck mining, ROM ore conveying, wet concentration, rare earth mineral flotation, dry mineral separation and progressive backfill.

The DFS demonstrates strong financial outcomes, with an after-tax NPV8 of US$813 million, an after-tax IRR of 39.4%,

total life-of-mine EBITDA of US$2.8 billion and total after-tax free cash flow of approximately US$1.93 billion. Phase 1 development capital is estimated at US$228.1 million, with Phase 2 incremental capital of US$153.2 million, for total development capital of US$381.3 million.

Titan is more than a mineral sands project. It is a differentiated U.S. critical minerals platform with exposure to three strategic product streams from a single domestic resource base. Its heavy rare

earth concentrate is enriched in yttrium, dysprosium and terbium — materials required for high-temperature magnets, advanced ceramics, radar, semiconductor equipment, aerospace and defense systems. Its titanium and zircon product streams extend

Titan’s relevance into U.S. defense, energy, aerospace, nuclear, robotics and advanced manufacturing supply chains.

This combination of scale, permitting, infrastructure, conventional processing and strategic product exposure positions Titan as one of the most actionable near-term U.S. critical minerals projects

capable of addressing multiple supply chain gaps from a single domestic source.

Strategic Importance to the U.S.

Titan is positioned as a cornerstone U.S. critical minerals project because it combines four attributes rarely found in one domestic mineral resource base.

First, Titan has a near-term development pathway in the United States, with key permits already in place. Second, it is designed to produce a heavy rare earth concentrate containing strategically

scarce yttrium, dysprosium and terbium. Third, it provides meaningful titanium and zircon mineral streams that are relevant to defense, aerospace, nuclear and advanced manufacturing supply chains. Fourth, it is based on a staged, lower-risk

development plan using conventional mineral sands processing methods.

The United States is actively rebuilding rare earth separation, metal, alloy and magnet manufacturing capacity. However, those midstream and downstream investments require secure upstream feedstock.

Titan directly targets this missing domestic feedstock node by providing a U.S.-based source of heavy rare earth concentrate while also supplying titanium minerals and zircon concentrate into markets that are exposed to foreign concentration and

supply chain disruption.

8

Titan is not a single-product project. It is a multi-critical-mineral industrial platform.

Titan’s permitting and execution position is a major competitive advantage. The project is located in an established industrial corridor, with key mine area permits already in place and access to

road, rail, barge, power, water and gas infrastructure. This execution setting differentiates Titan from many remote or earlier-stage critical mineral developments that require substantial greenfield infrastructure, long permitting pathways and

higher logistics complexity.

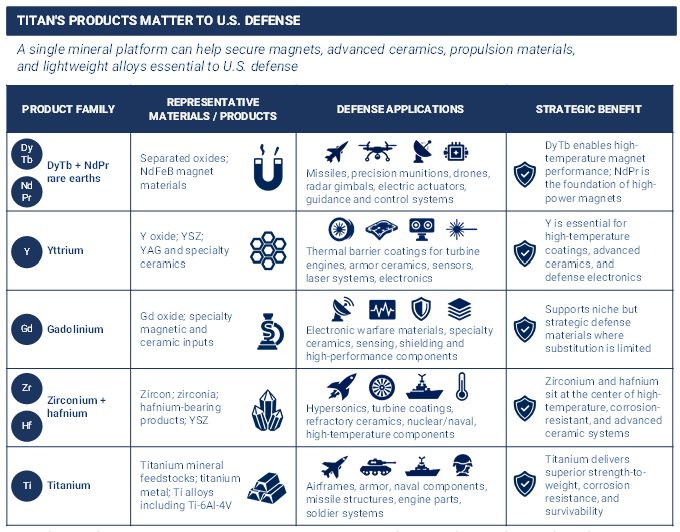

Titan’s product suite is also directly aligned with some of the most important material requirements of the U.S. defense industrial base. Through one domestic mineral platform, Titan has the potential

to support American supply chains for rare earth magnets, advanced ceramics, propulsion materials, refractory inputs and lightweight structural alloys.

Figure 3: Titan's products map to defense magnets, advanced ceramics, propulsion materials, and lightweight alloys.

Dysprosium, terbium and neodymium-praseodymium rare earths are essential to high-performance permanent magnets used in missiles, precision munitions, unmanned systems, radar platforms, electric

actuators, guidance systems and other mission-critical defense technologies. Yttrium, gadolinium, zirconium, hafnium and titanium materials support applications ranging from turbine thermal barrier coatings, armor ceramics and electronic warfare

systems to hypersonics, naval components, airframes, missile structures, engine parts and soldier systems.

9

Collectively, these materials occupy high-value positions in platforms where performance requirements are demanding, substitution is limited and secure domestic supply is increasingly strategic.

Titan therefore represents a rare combination: a near-term U.S. development project with strong financial returns and key permits already in place, conventional execution, and direct relevance to

multiple strategic supply chains. Titan offers leverage to a diversified critical minerals platform with compelling economics, staged capital intensity and strong alignment with U.S. industrial policy, defense resilience and the reshoring of

advanced manufacturing.

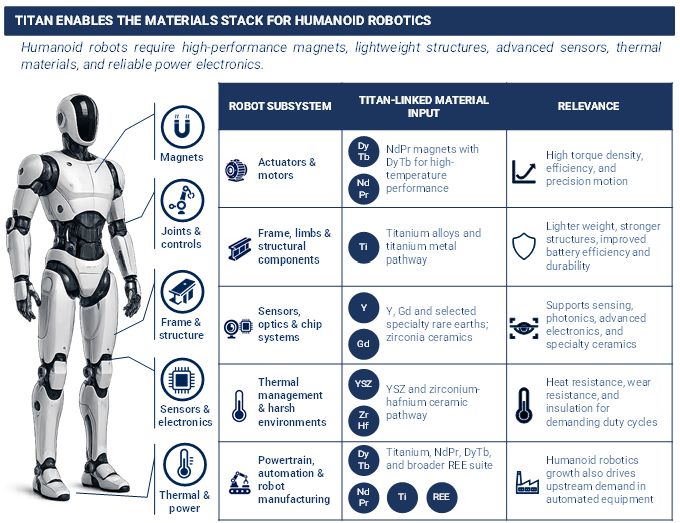

Titan’s relevance extends beyond defense into the next generation of physical AI, including humanoid robotics, factory automation and advanced manufacturing. Humanoid robots will require high-torque,

high-efficiency magnets for actuators, motors, hands and joints; titanium-based materials for lightweight frames, limbs and structural components; specialty rare earths and ceramics for sensors, optics, chips and electronics. As robotics demand

scales, Titan’s broader suite of magnets, metals and ceramic feedstocks positions the company at the intersection of national security, industrial automation and American supply-chain resilience.

Figure 4: Titan enables the materials stack for humanoid robotics and physical AI.

Rare Earths Overview

Rare earths are a group of 17 elements comprising the 15 lanthanides, plus scandium and yttrium. Although rare earths are not necessarily scarce in the earth’s crust, the economically recoverable

heavy rare earth elements — particularly dysprosium, terbium and yttrium — are geologically scarce and strategically valuable.

Their importance is driven by properties that are difficult to substitute: exceptional magnetic strength, high-temperature stability, optical performance, catalytic activity, plasma resistance and

durability in harsh operating environments. For U.S. defense and advanced industry, the most strategically important rare earths are concentrated in a small subset:

10

| • |

Neodymium and praseodymium are the foundation of high-power NdFeB permanent magnets.

|

| • |

Dysprosium and terbium enable those magnets to maintain coercivity and performance at elevated temperatures, which is essential for missiles, aircraft, electric drives,

drones, robotics, naval systems, actuators and harsh-environment industrial equipment.

|

| • |

Yttrium is a high-impact heavy rare earth used in yttria-stabilized zirconia thermal barrier coatings, YAG lasers, YIG microwave components, plasma etch chamber coatings,

advanced ceramics, specialty electronics and semiconductor manufacturing equipment.

|

The supply-chain risk is structural. China dominates major stages of the rare earth system, including mining, cracking, separation, metallization and sintered magnet manufacturing. Heavy rare earth

exposure is even more acute because global dysprosium and terbium supply has relied heavily on Myanmar-origin feedstock processed through China, while U.S. heavy rare earth and yttrium supply remains highly import-dependent.

The result is a direct vulnerability for U.S. defense, aerospace, automotive, semiconductor, energy and robotics supply chains.

This is what makes Titan strategically differentiated. Titan is not simply another light rare earth project. It is designed to produce a U.S.-sourced heavy rare earth concentrate enriched in

dysprosium, terbium and yttrium from monazite- and xenotime-bearing mineral sands. That positions Titan as a potential upstream feedstock node for the U.S. mine-to-magnet, semiconductor and advanced materials supply chains now being rebuilt with

U.S. Government support.

U.S. Rare Earth Supply Chain

The United States is actively reshoring rare earth separation, metal, alloy and permanent magnet manufacturing capacity. Federal support has been directed across multiple downstream and midstream

projects, including MP Materials, Lynas USA, E-VAC, Noveon Magnetics, TDA Magnetics, Vulcan Elements and ReElement Technologies.

This downstream investment is strategically important, but it does not solve the entire supply-chain problem. Separation plants, metal makers, alloy producers and magnet manufacturers require secure,

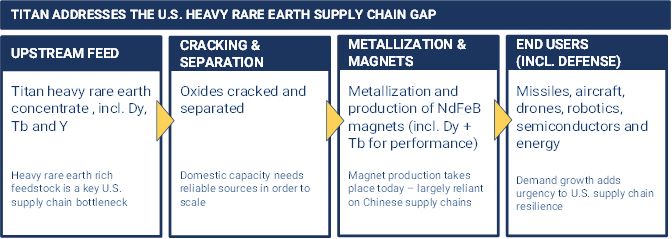

qualified and scalable upstream feedstock. Without a U.S.-based, heavy-rare-earth-rich resource, domestic magnet and semiconductor supply chains remain exposed to imported dysprosium, terbium and yttrium.

Figure 5: Titan addresses the upstream feedstock bottleneck in the U.S. rare earth supply chain by providing a potential domestic source of monazite- and

xenotime-bearing heavy rare earth concentrate.

11

The largest current U.S. rare earth mine, MP Materials’ Mountain Pass operation, is a globally important light rare earth bastnaesite deposit. However, Mountain Pass is not a material domestic source

of the heavy rare earths most constrained in U.S. supply chains. Its ores contain only trace amounts of dysprosium, terbium and yttrium.

Titan is differentiated by mineralogy. Its monazite- and xenotime-bearing mineral sands are designed to produce a heavy rare earth concentrate enriched in yttrium, dysprosium and terbium, while also

containing neodymium and praseodymium for permanent magnet supply chains.

Titan fills a different role: a U.S. mineral resource capable of feeding the separation, metal, alloy and magnet investments the United States is already building.

The U.S. requirement for rare earths now extends well beyond electric vehicles and wind turbines. High-performance magnets are embedded in precision actuators, drones, satellites, missile systems,

radar platforms, shipboard systems, EV drivetrains, industrial automation and humanoid robots. Yttrium and other specialty rare earths extend Titan’s relevance into semiconductors, lasers, photonics, microwave components, advanced ceramics and

thermal barrier coatings.

In practical terms, modern defense systems and physical AI platforms will need minerals, magnets and metals — not just software.

China’s use of rare earths as a strategic lever is no longer hypothetical. The 2010 China-Japan dispute demonstrated rare earth leverage, and China’s 2025 export controls on medium and heavy rare

earths and related magnet materials showed how quickly non-China manufacturers can face licensing risk, shortages and price dislocation. The U.S. response cannot be limited to downstream subsidies. It must also secure the upstream heavy rare earth

feedstock that makes downstream capacity viable.

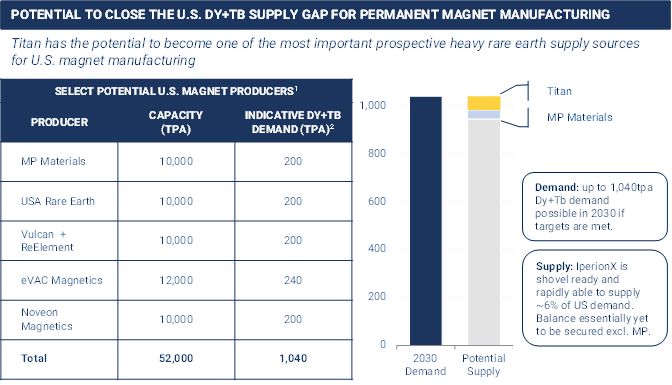

Figure 6: Illustrative Dy/Tb supply versus selected U.S. NdFeB magnet manufacturing deman1,2,3.

1 Source: Public press releases. Capacity represents targeted nameplate run-rates with

commissioning/completion targets beginning in 2027/2028/2029.

2 Illustrative Dy+Tb demand potential based on an assumed 2% Dy+Tb material intensity for magnet

making. Actual material intensity in magnet-making varies depending on product.

3 See ‘Endnote 1’ - peer comparison material assumptions, page 22.

12

Titan is one of the most actionable near-term U.S. development options to address that gap. It combines a domestic resource base, existing permits, established logistics, conventional mineral sands

processing and a heavy rare earth concentrate product designed around the materials most constrained in the U.S. supply chain.

|

SUPPLY-CHAIN NODE

|

U.S. ACTIVITY

|

STRATEGIC GAP

|

TITAN RELEVANCE

|

||||

|

Primary mining / concentrate

|

MP Materials Mountain Pass; IperionX Titan HREC

|

Mountain Pass is light rare earth dominant; U.S. lacks domestic heavy rare earth feedstock

|

Titan is positioned as a U.S. source of HREC enriched in Dy, Tb and Y

|

||||

|

Rare earth separation

|

MP Materials; Lynas USA; Energy Fuels White Mesa pathway

|

Separation capacity requires qualified, scalable feedstock

|

Titan may provide domestic monazite / xenotime-bearing feedstock

|

||||

|

Metallization / alloys

|

Vulcan Elements; E-VAC; MP Materials

|

Metal and alloy capacity needs separated oxides, including Dy/Tb for defense-grade magnets

|

Titan can support upstream feedstock security for downstream metals and alloy production

|

||||

|

Magnet manufacturing

|

E-VAC, Noveon, TDA, MP Materials 10X, Vulcan

|

High-temperature NdFeB magnets require reliable Dy/Tb supply

|

Titan targets the heavy rare earth bottleneck required for high-performance magnets

|

||||

|

Recycling and secondary recovery

|

ReElement, other recyclers

|

Valuable but not a substitute for mine-scale primary supply

|

Titan has the potential to provide primary supply that can complement recycling and circular supply chains

|

Table 2: Titan’s role across the U.S. rare earth supply chain.

|

REPRESENTATIVE U.S.

COMPANY

|

RELEVANT PLATFORMS

|

WHY RARE EARTH MAGNETS OR HREE MATTER

|

|||

|

Lockheed Martin

|

F-35, missiles, space systems

|

Permanent magnets support motors, actuators, sensors and other compact high-power-density systems; Dy/Tb support high-temperature magnet performance.

|

|||

|

RTX / Raytheon

|

Missiles, radar, air-defense systems

|

Rare earth magnets and yttrium-bearing microwave materials support guidance, actuation, radar and electronic systems.

|

|||

|

Northrop Grumman

|

Autonomous aircraft, defense electronics, space systems

|

Motors, actuators, sensors and payload systems rely on high-performance magnetic materials.

|

|||

|

General Dynamics

|

Nuclear submarines, land systems, defense platforms

|

Permanent magnets are relevant to compact motors, generators, actuators and submarine systems.

|

|||

|

Boeing

|

Aircraft, defense and space platforms

|

Aerospace systems use high-reliability motors, actuators, generators and sensor systems where rare earth magnets can reduce weight and size.

|

|||

|

GE Aerospace

|

Jet engines and aerospace power systems

|

Rare earth magnets support high-density electrical systems; yttrium is critical to thermal barrier coatings.

|

|||

|

GM / Ford

|

EVs and advanced vehicle platforms

|

NdFeB magnets are used in high-efficiency traction motors and automotive actuators; Dy/Tb improve high-temperature performance.

|

|||

|

Tesla

|

EVs, robotics and energy products

|

Permanent magnet motors and robotics systems demand nodes for NdPr and potentially Dy/Tb depending on design.

|

|||

|

Lam Research / Applied Materials

|

Semiconductor manufacturing equipment

|

Yttria coatings are used in plasma etch environments; rare earth magnets are used in equipment subsystems

|

Table 3: Representative U.S. demand for rare earth magnets and HREE/Y materials.

13

Humanoid robots, semiconductor fabs, data centers and automated factories are emerging as new critical-mineral demand centers. They require high-performance magnets for actuators and motors, titanium

and zirconium-bearing materials for lightweight structures and harsh-environment components, yttrium and gadolinium for sensors, optics and specialty ceramics, and thermally robust materials for power electronics and energy infrastructure.

Titan Project's Role in the U.S. Rare Earth Supply Chain

Titan is designed to address the missing upstream resource gap in the U.S. heavy rare earth supply chain.

The DFS forecasts total life-of-mine production of approximately 60,790 tons of HREC, including approximately 5,287 tpa at full Phase 2 run-rate. The DFS design-basis HREC is approximately 61.4% TREO

and contains important dysprosium, terbium and yttrium exposure, derived from monazite and xenotime mineralization contained within Titan’s mineral sands.

This mineralogy is fundamentally different from bastnaesite deposits such as Mountain Pass, which is a globally important light rare earth operation, but does not by itself address the heavy rare

earth supply gap. Titan is designed to produce a concentrate with meaningful exposure to the materials that remain most constrained: dysprosium, terbium and yttrium.

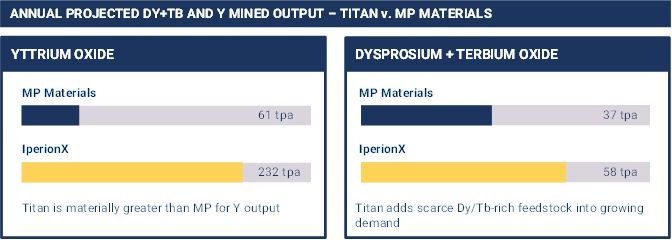

At the Phase 2 annual HREC production rate, Titan’s HREC product is forecast to contain approximately:

| • |

48 tpa Dy₂O₃

|

| • |

11 tpa Tb₄O₇

|

| • |

232 tpa Y₂O₃

|

Based on Argus 2026 forecast prices, heavy rare earth elements represent approximately 13% of TREO content by mass, but more than 70% of forecast HREC basket value. This means Titan’s HREC is not just

heavy-rare-earth-bearing; it is heavy-rare-earth-dominant by value. That is a critical distinction for investors and policymakers. Titan’s strategic value is not driven solely by total rare earth tonnage. It is driven by the value, scarcity and

strategic importance of the contained heavy rare earths and yttrium.

Titan is positioned to address one of the most important gaps in the U.S. critical minerals strategy: secure domestic feedstock for heavy rare earth separation, metals, alloys and magnets.

The project combines a U.S. resource base, existing permits, conventional mineral sands processing, established infrastructure and a differentiated HREC product enriched in dysprosium, terbium and

yttrium. This positions Titan as a potential cornerstone upstream feedstock source for U.S. defense, aerospace, semiconductor, robotics and advanced manufacturing supply chains.

Figure 7: Annual projected Dy+Tb and Y output compared to MP Materials’ Mountain Pass operation1.

1 See Endnote 1 - peer comparison material assumptions,

page 22.

14

|

TITAN HREC ATTRIBUTE

|

DFS-BASED VALUE

|

|

|

HREC production

|

5,287 tpa in Phase 2

|

|

|

TREO grade

|

61.4% TREO

|

|

|

Contained Dy2O3

|

~48 tpa at Phase 2

|

|

|

Contained Tb4O7

|

~11 tpa at Phase 2

|

|

|

Contained Y2O3

|

~232 tpa at Phase 2

|

Table 4: Titan Project heavy rare earth concentrate.

Titanium Overview

Titanium is a strategic metal with a rare combination of high strength-to-weight ratio, corrosion resistance, fatigue performance, heat tolerance and compatibility with demanding aerospace and defense

environments. These properties make titanium essential across airframes, engine-adjacent structures, landing gear, fasteners, armor, naval systems, missiles, satellites, drones, medical devices, energy infrastructure and advanced manufacturing.

For U.S. defense and industrial policy, titanium is not simply another metal. It is a qualification-heavy material embedded in mission-critical platforms where shortages, long lead times or uncertain

provenance can affect readiness, production schedules, platform cost and supply-chain resilience.

The legacy titanium metal supply chain is capital-intensive, energy-intensive and structurally inefficient. Titanium minerals are typically upgraded and chlorinated into titanium tetrachloride,

reduced by magnesium through the Kroll process to produce titanium sponge, melted and re-melted into ingot, converted through forging or rolling into mill products, and then machined into finished components. Each step adds cost, time, yield loss

and qualification complexity. One ton of titanium sponge typically yields only approximately 0.6–0.8 tons of titanium mill product, and after downstream buy-to-fly losses, can result in as little as approximately 0.2 tons of finished titanium

parts.

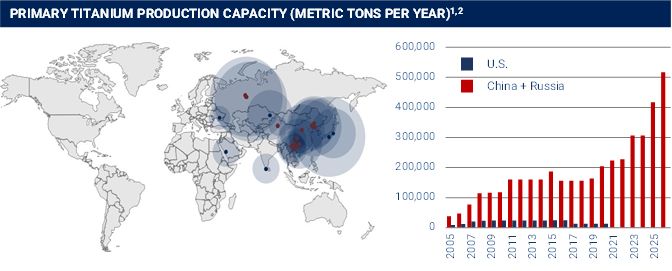

This inefficiency is a major reason titanium remains expensive and strategically sensitive. It is also why supply-chain control matters. The U.S. no longer produces commercial titanium sponge, leaving

domestic ingot, mill-product, forging and component suppliers reliant on imported sponge, imported scrap and domestic recycled scrap. USGS estimates indicate that the U.S. imported approximately 44,000 tons of titanium sponge and approximately

32,000 tons of titanium scrap in 2025.

The strategic risk is compounded by foreign concentration. Japan, Kazakhstan and Saudi Arabia were leading U.S. titanium sponge import sources through July 2025, while China has become the world’s

dominant producer and consumer of titanium mineral concentrates and has materially expanded across the titanium value chain. Russia and China also remain strategically important global sponge and titanium metal supply-chain actors, creating a

resilience challenge for U.S. defense, aerospace and advanced manufacturing customers.

The U.S. Department of Commerce’s Section 232 titanium sponge investigation found that titanium sponge imports threatened to impair U.S. national security, highlighting that the absence of domestic

sponge production capacity could limit U.S. surge capacity for defense and critical infrastructure needs during a national emergency. That finding remains highly relevant: domestic melting and downstream fabrication capacity do not fully resolve

the vulnerability if the upstream sponge and mineral feedstock inputs remain foreign-dependent.

15

Figure 8: Global primary titanium (sponge) production locations and U.S. capacity vs. China and Russia capacity over time1.

U.S. Titanium Supply Chain

The current U.S. titanium supply chain is fragmented. The United States has world-class aerospace, defense, specialty metals, forging, casting and precision component manufacturing capability.

Domestic companies can convert sponge and scrap into qualified titanium products for aerospace and defense platforms. However, those operations remain structurally dependent on imported sponge and variable scrap availability.

This creates a strategic mismatch. The U.S. has advanced titanium-consuming industries, but lacks secure domestic primary titanium input capacity at commercial scale.

For defense procurement, this matters because titanium alloys are specialty metals embedded across aircraft, missile and space systems, ships, submarines, tanks, weapon systems and ammunition. U.S.

law and DFARS provisions focus on specialty metals melted or produced in the United States or qualifying countries. However, a domestic melt step does not by itself solve the upstream vulnerability. A supply chain that begins with imported sponge

remains exposed to foreign capacity constraints, logistics disruption, price spikes, geopolitical risk and qualification bottlenecks.

The defense exposure is visible in the F-35 supply chain. Public Howmet / Alcoa materials state that titanium bulkheads and titanium material are used to manufacture airframe structures for all three

F-35 variants, including the largest titanium bulkheads for the CTOL variant. This illustrates why titanium supply security is not theoretical: titanium availability, cost and qualification directly affect high-priority aerospace and defense

programs.

|

REPRESENTATIVE U.S.

COMPANY

|

RELEVANT PRODUCTS /

PLATFORMS

|

WHY TITANIUM MATTERS

|

|||

|

Lockheed Martin

|

F-35, missiles, hypersonics, space and rotorcraft systems

|

Titanium supports airframe structures, bulkheads, fasteners and high-strength lightweight components where weight, fatigue life and heat performance matter.

|

|||

|

RTX / Pratt & Whitney / Raytheon

|

Military and commercial engines, missiles, radar and precision systems

|

Titanium is used in engine structures, rotating and static components, housings and missile / aerospace hardware that require strength-to-weight and durability.

|

|||

|

Boeing

|

Military aircraft, commercial aircraft, space systems and rotorcraft

|

Titanium supports airframes, landing gear, pylons, fasteners and composite-compatible structures while reducing weight and improving corrosion resistance.

|

1 U.S. Geological Survey. Locations shown represent titanium sponge production facilities, and

are approximate. List is not exhaustive, but is representative of American vs. RoW capacity. 2026 figures shown are estimates and projections, and Chinese data includes projections for incremental 2026 capacity from Argus Metals.

16

|

REPRESENTATIVE U.S.

COMPANY

|

RELEVANT PRODUCTS /

PLATFORMS

|

WHY TITANIUM MATTERS

|

|||

|

Northrop Grumman

|

B-21, uncrewed aircraft, space and missile systems

|

Titanium enables lightweight, qualified structures and mission-critical components for long-life defense and space platforms.

|

|||

|

General Dynamics

|

Submarines, combat vehicles, munitions and mission systems

|

Titanium provides corrosion resistance, weight reduction and survivability in marine, armor and high-reliability defense applications.

|

|||

|

Huntington Ingalls Industries

|

U.S. Navy ships, submarines and shipyard sustainment

|

Titanium is relevant to seawater-resistant piping, heat exchangers, specialty marine systems and high-integrity naval components.

|

|||

|

GE Aerospace

|

Jet engines and advanced propulsion systems

|

Titanium alloys support compressor and engine-adjacent structures where low weight and high fatigue performance are required.

|

|||

|

Honeywell Aerospace

|

Engines, APUs, avionics-adjacent and thermal systems

|

Titanium supports lightweight engine hardware, thermal management and corrosion-resistant aerospace components.

|

|||

|

Howmet Aerospace

|

F-35 bulkheads, forgings, fasteners, castings and aerospace materials

|

Howmet is a critical titanium supplier into F-35 and aerospace structures, making qualified titanium input security directly relevant.

|

|||

|

ATI / Precision Castparts / Carpenter Technology

|

Titanium mill products, forgings, specialty alloys and engineered components

|

These suppliers convert titanium input streams into qualified products that downstream defense and aerospace primes require.

|

Table 5: Representative U.S. demand for titanium.

Strategic Importance to Defense and Advanced Manufacturing

Titanium is embedded across major U.S. weapons platforms and advanced industrial systems. It supports lightweighting, survivability, fatigue resistance, corrosion resistance and high-temperature

performance.

Figure 9: Select major U.S. defense platforms that require titanium components.

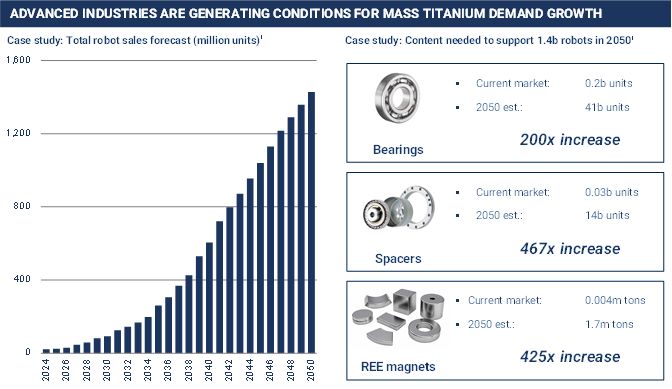

Key defense applications include:

| • |

Army: M777 Howitzer structures, lightweight armored systems and vehicle components.

|

| • |

Navy: submarine components, seawater-resistant piping, valves, fasteners, pumps and heat exchangers.

|

| • |

Air Force: F-22 and F-35 airframes, bulkheads, structural components, fasteners and engine-adjacent systems.

|

17

| • |

Missiles and hypersonics: high-strength lightweight structures, thermal-resistant components, propulsion-adjacent hardware and complex precision parts.

|

| • |

Space systems: qualified structural components, fasteners, thermal hardware and high-reliability mission components.

|

Titanium demand is also expanding beyond traditional aerospace and defense. Humanoid robotics, automated factories, advanced energy systems and physical AI platforms are likely to increase demand for

lightweight, high-strength, fatigue-resistant and corrosion-resistant materials. Robotics require low-mass structural components, precision actuators, fasteners, gears, bearings, thermal management systems and durable mechanical assemblies.

Titanium is well suited to these applications where performance, weight reduction and reliability matter.

Figure 10: Projected growth in humanoid robot sales, and demand implications for critical mechanical components that would benefit from titanium material usage1.

Titan’s Vital Role in the U.S. Titanium Supply Chain

Titan gives IperionX a differentiated pathway to address the U.S. titanium supply-chain challenge from upstream mineral resource through to finished titanium products.

The Titan DFS is designed to produce two titanium mineral products: ilmenite and rutile. At full Phase 2 run-rate, Titan is forecast to produce approximately 118,658 tpa of ilmenite and 24,656 tpa of

rutile. Using the DFS product specifications of 62.5% TiO₂ for ilmenite and 91.1% TiO₂ for rutile, this equates to approximately 58,000 tpa of titanium metal contained in Phase 2 product streams before downstream upgrading, recovery, commercial and

processing assumptions.

Over the 14-year DFS mine plan, Titan is forecast to produce approximately 1.37 million tons of ilmenite and 286,000 tons of rutile. On the same TiO₂-to-titanium metal basis, those saleable product

streams contain approximately 670,000 tons of titanium metal across the life of mine.

On an in-situ resource basis, using the DFS grand total THM of 9.163 million tons and THM assemblage of 40.8% ilmenite and 9.6% rutile, Titan contains an indicative approximately 1.71 million tons of

titanium metal in ilmenite and rutile minerals. Importantly, the Big Sandy critical minerals province is estimated to contain significantly more titanium minerals that could underpin higher production over decades.

1 Morgan Stanley research – December 2025

18

This scale is important, but the strategic significance is greater than mineral feedstock alone. IperionX is not only a mineral-feedstock developer. Titan can feed a broader integrated technology

pathway that includes:

| • |

Green Rutile™ and ARH™ enrichment / upgrading technologies to improve titanium feedstock quality.

|

| • |

HAMR™ to reduce titanium feedstock or scrap into titanium powder.

|

| • |

HSPT™ / powder metallurgy to manufacture high-performance titanium components and potential mill-product pathways.

|

This creates the strategic bridge from Tennessee titanium minerals to U.S. titanium metal production and finished titanium components.

IperionX’s Mineral-to-Metal Advantage

HAMR™ and HSPT™ are designed to address two of the largest structural inefficiencies in the incumbent titanium system.

HAMR™ is designed to bypass the Kroll process’s chlorination, sponge, melt and re-melt complexity by using hydrogen-assisted metallothermic reduction to produce titanium powder from recycled titanium

or mineral feedstocks, providing the potential to reduce titanium metal powder production costs by 40–70% relative to incumbent processes.

HSPT™ then enables near-net-shape titanium parts with wrought-quality mechanical properties, improving manufacturing yield and reducing buy-to-fly losses for defense, aerospace and advanced industrial

parts.

This matters because the legacy titanium supply chain loses value at every stage: mineral upgrading, sponge production, melting, mill-product conversion and final machining. IperionX’s pathway is

designed to compress that chain, reduce waste, lower production cost and increase U.S. supply-chain control.

Figure 11: Titan-to-titanium metal pathway from Tennessee minerals to U.S. titanium components.

IperionX is already scaling its downstream platform through development of titanium powder capacity of approximately 200 tpa, a U.S. Government-backed expansion to approximately 1,400 tpa by 2027, and

a target of more than 10,000 tpa by 20301. Titan provides the backward-integration option that can move this platform from recycled scrap dependence toward a fully

U.S. mineral-to-metal titanium supply chain.

1 Refer to ASX announcement dated September 2, 2025, titled “IperionX Commences U.S. DoD backed Titanium Expansion”

19

The strategic value is clear: Titan provides domestic titanium mineral feedstock; Green Rutile™ and ARH™ provide a potential upgrading pathway; HAMR™ provides a lower-cost titanium powder production

route; and HSPT™ provides a pathway to high-performance titanium components with reduced buy-to-fly losses.

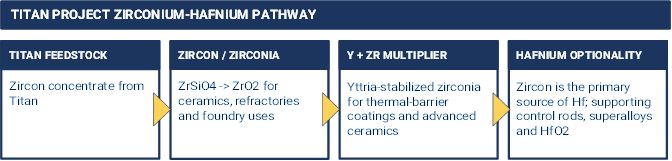

Zirconium and Hafnium Overview

Zircon’s commercial importance is broad. It is used in ceramics, refractories, investment casting, zirconia chemicals, high-temperature materials, thermal barrier coatings and chemical processing

equipment. However, its strategic importance is much greater than traditional industrial markets suggest.

Zirconium metal and zirconium alloys are vital to the nuclear industry because zirconium has low neutron absorption and excellent corrosion resistance, making zirconium alloys the dominant material

for nuclear fuel cladding. Secure zirconium supply is therefore directly relevant to civil nuclear power, naval nuclear propulsion and long-duration energy security.

Hafnium has a smaller-volume but high-strategic-value demand profile. It is used in nuclear control rods, nickel-based superalloys, plasma arc nozzles, high-temperature ceramics and semiconductor

high-k dielectric materials, including hafnium oxide. Hafnium is also relevant to refractory alloy pathways, including niobium-hafnium-titanium systems such as C-103, which are used in rocket nozzles, space propulsion, re-entry systems and

hypersonic structures.

This combination makes zircon more than a ceramic mineral. It is an upstream feedstock into some of the most demanding materials systems in nuclear energy, aerospace propulsion, hypersonics,

semiconductors, advanced ceramics and high-temperature industrial applications.

Figure 12: Titan zircon-hafnium pathway and the Y + Zr advanced-ceramics multiplier.

U.S. Zirconium + Hafnium Supply Chain

The U.S. zirconium and hafnium supply chain is specialized, qualification-heavy and strategically important. It spans upstream zircon mineral feedstock, zircon and zirconia chemicals, zirconium metal,

hafnium separation, nuclear-grade alloys, semiconductor materials and advanced ceramic systems.

The United States has downstream zirconium metal capability and significant nuclear-related expertise. However, the upstream supply chain remains exposed to global heavy mineral sands supply and

specialized processing pathways.

Despite having significant domestic resources of zircon, such as Titan and those within the Big Sandy critical minerals province, the U.S. import sources for zirconium ores and concentrates have

historically included South Africa, Australia and Senegal, highlighting the lack of a large domestic mineral production base. China lacks significant domestic resources of economic extractable zircon and is highly reliant on the same countries as

the U.S.

20

This creates a strategic vulnerability. The U.S. has high-value downstream demand in nuclear, aerospace, defense, semiconductor and advanced ceramics applications, but the upstream zircon and

hafnium-bearing mineral supply chain remains dependent on foreign sources. Titan and the Big Sandy critical minerals province can underpin long term domestic supply security of zircon and hafnium for the United States.

Zirconium and hafnium matter at the intersection of several strategic markets:

| • |

Nuclear energy and naval propulsion: zirconium alloys for nuclear fuel cladding; hafnium for control rods.

|

| • |

Hypersonics and space: hafnium-bearing superalloys, refractory alloys, high-temperature ceramics and thermal protection systems.

|

| • |

Jet engines and propulsion: zirconia and yttria-stabilized zirconia thermal barrier coatings; hafnium-bearing alloy systems.

|

| • |

Semiconductors: hafnium oxide high-k dielectrics; zirconia / yttria ceramics for plasma-facing components.

|

| • |

Advanced ceramics: zirconia and YSZ for wear resistance, heat resistance, insulation and harsh-environment reliability.

|

For U.S. policymakers and defense customers, the issue is not simply zircon pricing. It is whether the United States has secure access to upstream feedstocks required for nuclear systems, propulsion

materials, high-temperature ceramics and semiconductor manufacturing.

As such, Titan’s zircon concentrate is a strategically relevant upstream feedstock into a domestic material pathway that extends well beyond traditional mineral sands markets.

|

REPRESENTATIVE U.S.

COMPANY

|

RELEVANT PRODUCTS / PLATFORMS

|

WHY ZIRCONIUM / HAFNIUM MATTER

|

|||

|

Westinghouse

|

Nuclear fuel, fuel assemblies and reactor services

|

Zirconium alloys are core fuel-cladding materials; hafnium can be used in control rods because of neutron absorption.

|

|||

|

BWX Technologies

|

Naval nuclear components, nuclear fuel and government services

|

Zr/Hf materials are relevant to nuclear materials, reactor systems and high-specification defense supply chains.

|

|||

|

GE Vernova / GE Hitachi

|

Nuclear reactors, energy systems and industrial equipment

|

Zirconium alloys and zirconia ceramics support nuclear, turbine and high-temperature energy applications.

|

|||

|

Framatome Inc.

|

Nuclear fuel assemblies and reactor components

|

Zirconium alloy cladding and related nuclear materials require qualified supply chains.

|

|||

|

Lockheed Martin

|

Space, missile defense, hypersonics and propulsion-adjacent systems

|

Zr/Hf ceramics and refractory alloys are relevant to high-temperature structures, thermal protection and propulsion components.

|

|||

|

RTX / Pratt & Whitney / Raytheon

|

Jet engines, missiles, sensors and defense electronics

|

YSZ coatings, hafnium-bearing superalloys and advanced ceramics support high-temperature propulsion and electronics reliability.

|

|||

|

Northrop Grumman

|

Space systems, missiles, propulsion and autonomous platforms

|

Zr/Hf pathways support thermal protection, propulsion hardware and mission-critical high-temperature materials.

|

|||

|

Applied Materials / Lam Research

|

Semiconductor fabrication equipment and process systems

|

Zirconia/yttria ceramics and hafnium oxide are relevant to plasma-facing components and high-k dielectric materials.

|

|||

|

CoorsTek / Saint-Gobain Ceramics

|

Advanced technical ceramics and industrial components

|

Zirconia and YSZ ceramics provide wear resistance, heat resistance and electrical / thermal performance.

|

|||

|

Corning / specialty glass and ceramics suppliers

|

Specialty glass, ceramics, optics and industrial products

|

Zircon and zirconia improve heat, chemical and mechanical performance in specialty glass and ceramic systems.

|

Table 6: Representative U.S. demand for zirconium and hafnium.

21

Titan’s Role in the Zirconium Supply Chain

Titan is designed to produce zircon concentrate as a saleable product alongside heavy rare earth concentrate, ilmenite and rutile. This gives Titan a multi-product revenue base and positions the

project as a potential domestic source of rare earth, titanium and zircon-bearing mineral feedstocks from a single U.S. resource base.

The DFS projects production of approximately 767,168 tons of zircon concentrate over the life of mine and approximately 65,668 tpa of zircon concentrate at Phase 2 run-rate. The DFS product

specification of 34.4% ZrO₂ for zircon concentrate equates to approximately 34,000 tpa on a premium zircon basis.

That scale is important. It is not so large that it would overwhelm global zircon markets, but it is meaningful as a domestic U.S. feedstock source for strategic zirconium-related supply chains.

Titan’s zircon concentrate product contains approximately 195,000 tons of zirconium metal over the life of mine and approximately 16,700 tpa at Phase 2 run-rate, before downstream processing and recovery assumptions.

A further advantage is the Y + Zr multiplier given that Titan’s HREC is enriched in yttrium while its zircon concentrate provides a zirconium feedstock. Together, these streams are relevant to

yttria-stabilized zirconia and advanced ceramic systems used in thermal barrier coatings, turbine engines, high-temperature electronics, armor ceramics, semiconductor equipment and harsh-environment sensors. This makes Titan more than a standalone

zircon project: it is a potential domestic platform for zirconium, hafnium and yttrium-linked materials systems.

Endnote 1 – peer comparison material assumptions

|

Company / project

|

Status

|

Proved reserves

|

Probable reserves

|

Total reserves

|

Grade

|

|

|

IperionX / Titan

|

DFS

|

93.3 Mt

|

23.7 Mt

|

117.0

|

3.2% THM

|

|

|

MP Materials / Mountain Pass

|

Producer

|

1.0 Mt

|

27.9 Mt

|

29.0

|

5.9% TREO

|

Source: IperionX – Titan Project Definitive Feasibility Study, June 4, 2026 (this report), MP Materials – Form 10K Annual Report, February 26, 2026 (link)

Notes: Values subject to rounding. Titan reserve grade presented in Total Heavy Mineral (THM). Mountain Pass reserve grade presented in Total Rare Earth Oxide (TREO). The Mountain

Pass reserve is reported pursuant to the requirements of Regulation S-K Subpart 1300 (“S-K 1300”), and the Titan reserve is reported under the JORC Code (2012). The Competent Person has not undertaken sufficient work to classify the S-K 1300

estimates as JORC Compliant Mineral Resources or Ore Reserves, meaning that following further evaluation the estimate may change or not achieve JORC status. Nonetheless, the comparison is reasonable because:

- The comparator projects are disclosed under alternative recognised reporting standards (i.e. S-K 1300), with broadly equivalent scale, grade ranges and development status.

- All data inputs are sourced from public filings (e.g. public reports and investor presentations) and referenced to the original source and date.

- The comparative metrics are clearly contextual – intended as industry benchmarks for scale and stage, rather than definitive reserve/resource values.

22

23

DFS Summary

Introduction and Background

IperionX is pleased to announce the completion of the DFS for the commercial-scale development of the Titan Project, located near Camden, Tennessee (“Titan”, the “Titan Project”, or the “Project”).

The DFS design considers the mining and processing of heavy mineral sands from the McNairy Formation to produce saleable ilmenite, rutile, zircon concentrate and heavy rare earth concentrate (“HREC”) over a 14-year mine life based on proved and

probable reserves.

The Titan Project is strategically significant because it combines a large, domestic mineral resource, a conventional and simple mineral sands processing route, a multi-product revenue base and a

location within an established U.S. industrial jurisdiction. These characteristics distinguish Titan from many remote mineral sands and rare earth projects and support its potential role as a domestic upstream source of critical minerals. The DFS

confirms the Titan Project as a technically and economically robust development, supported by a maiden Ore Reserve and a multi-product revenue base including critical mineral product lines, as defined by the U.S. federal government.

The DFS was prepared by Marshall Miller & Associates, Inc. (MM&A). While MM&A fulfilled the responsibility as the integrator of the DFS, other consulting firms also completed vital aspects

of the Study. Karst Geo Solutions, LLC (KGS) was responsible for exploration results for the Project. Mineral Technologies Pty Ltd (MT) completed the process plant design and related modular plant cost estimation. Primero Group Americas Inc.

(Primero) completed the non-process infrastructure (NPI) design and related cost estimates and was responsible for integrating the mining, process and NPI costs into a discounted cash flow financial model for the DFS.

The Company has included supporting technical information in Appendix 1 and JORC Table 1 disclosure in Appendix 2. Appendix 1 summarizes the technical workstreams and assumptions supporting the DFS

outcomes. Information relating to Exploration Results, Mineral Resources and Ore Reserves has been prepared and reported in accordance with the JORC Code 2012 and is supported by the Competent Persons Statements included in this announcement.

Key DFS Work Programs and Assumptions

The DFS builds upon prior exploration, mineral resource estimation, metallurgical test work, process design, infrastructure design, environmental baseline work, permitting analysis, mine planning and

financial modeling. The DFS has been prepared to support estimation of Ore Reserves and provide a detailed basis for decision-making on project development, financing and implementation planning.

Work completed for the DFS included updated geologic modeling and resource estimation, pit optimization, mine scheduling, process flowsheet development, engineering design, infrastructure design,

capital and operating cost estimation, financial modeling, environmental and permitting analysis and market studies.

Capital and operating cost estimates are prepared to a ±15% level of accuracy. All costs are expressed in real 2026 United States dollars.

Project Overview

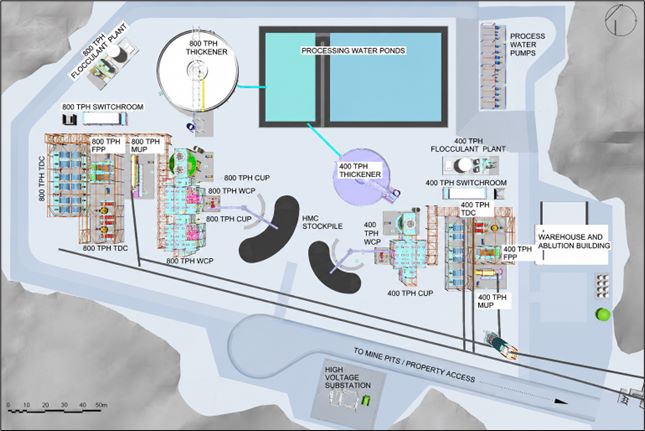

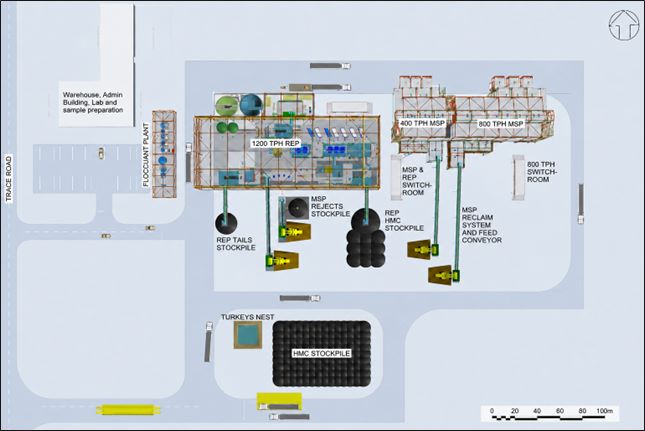

The Titan Project is a proposed critical minerals mining and mineral processing operation near Camden, Tennessee. The Project is designed to recover mineral sands from the McNairy Formation and

process those minerals into saleable ilmenite, rutile, zircon concentrate and HREC. The mine and Wet Concentrator Plant (“WCP”) are located near the mineral deposit, while the Rare Earth Plant (“REP”) and Mineral Separation Plant (“MSP”) are

planned to be located at a separate industrial site in the Camden area.

The Project benefits from its location in the United States, including access to road and rail infrastructure, skilled labor, industrial services, utilities and customers in critical mineral sectors.

The project location is a core strategic differentiator when compared with remote projects that require long-distance logistics, greenfield camp infrastructure, airstrips and isolated power solutions.

24

Ownership and Tenure

IperionX has a large regional ground holding prospective for valuable mineral sands, of which a small subset of the mineral tenure hosts the current Mineral Resource and

Ore Reserve estimates. For the purposes of this Report, the term “Property” is used for the larger ground holding, and the term “Study Area” is used for the area that hosts the Mineral Resource and Ore Reserve estimates.

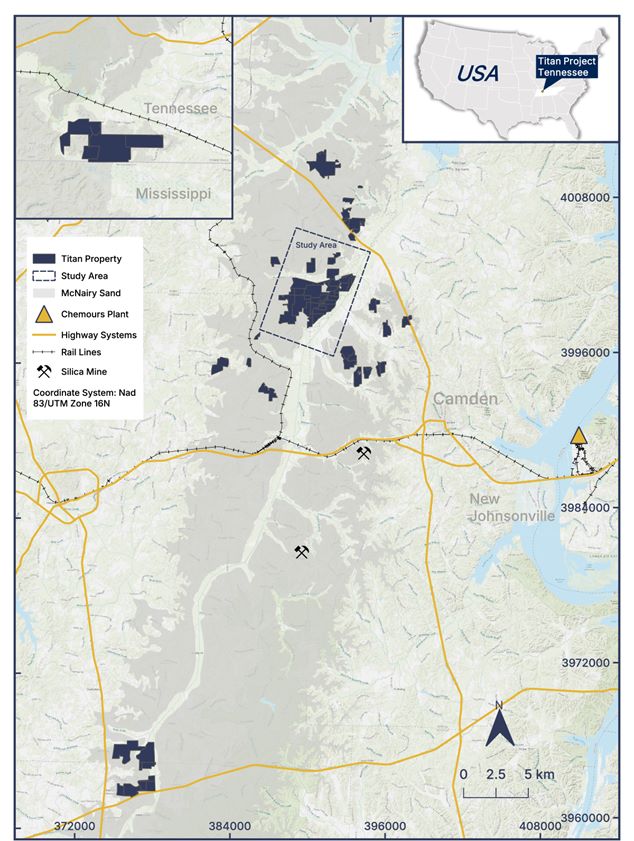

The Titan Project is located near Camden, Tennessee, U.S., approximately 128 kilometers (km) (80 miles) west of Nashville, Tennessee and approximately 11 km (7 miles) northwest of Camden, Tennessee.

The Study Area is centered at approximately 36.147349°N, -88.20974°W.

As at June 4, 2026, the Property consists of approximately 40.8 square kilometers (km2) (10,091 acres) of surface and

associated mineral rights in Tennessee, of which approximately 6.0 km2 (1,490 acres) are owned by IperionX, approximately 5.9 km2 (1,457 acres) are subject to long-term lease by IperionX, and approximately 28.9 km2 (7,144 acres) are subject to

exclusive option agreements with IperionX. These exclusive option agreements, upon exercise, allow IperionX access to the surface property and associated mineral rights.

As at June 4, 2026, the Study Area is comprised of approximately 13.4 km2 (3,317 acres) of surface and associated

mineral rights, of which approximately 4.9 km2 (1,212 acres) are owned by IperionX, approximately 4.6 km2 (1,147 acres) are subject to long-term lease by IperionX, and approximately 3.9 km2 (958 acres) are subject to exclusive option

agreements with IperionX.

For the optioned and leased land, IperionX will pay the landowner the greater of 1) US$75 per acre of the property per year, or 2) the production royalty, generally 5% of net revenues from products

mined and removed from the property. All properties owned by IperionX or its subsidiary will not incur a royalty.

25

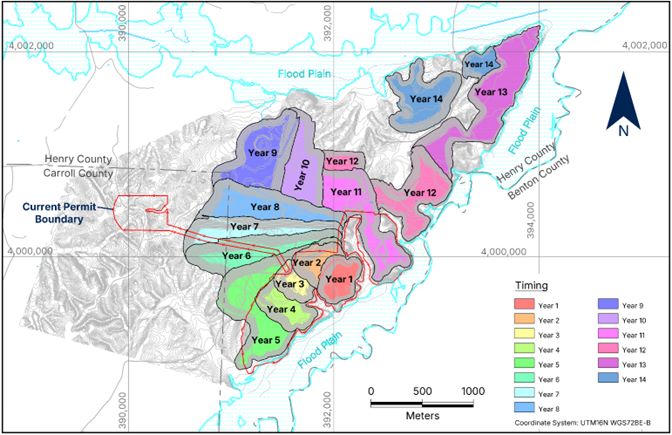

Figure 13: Titan property and study area.

26

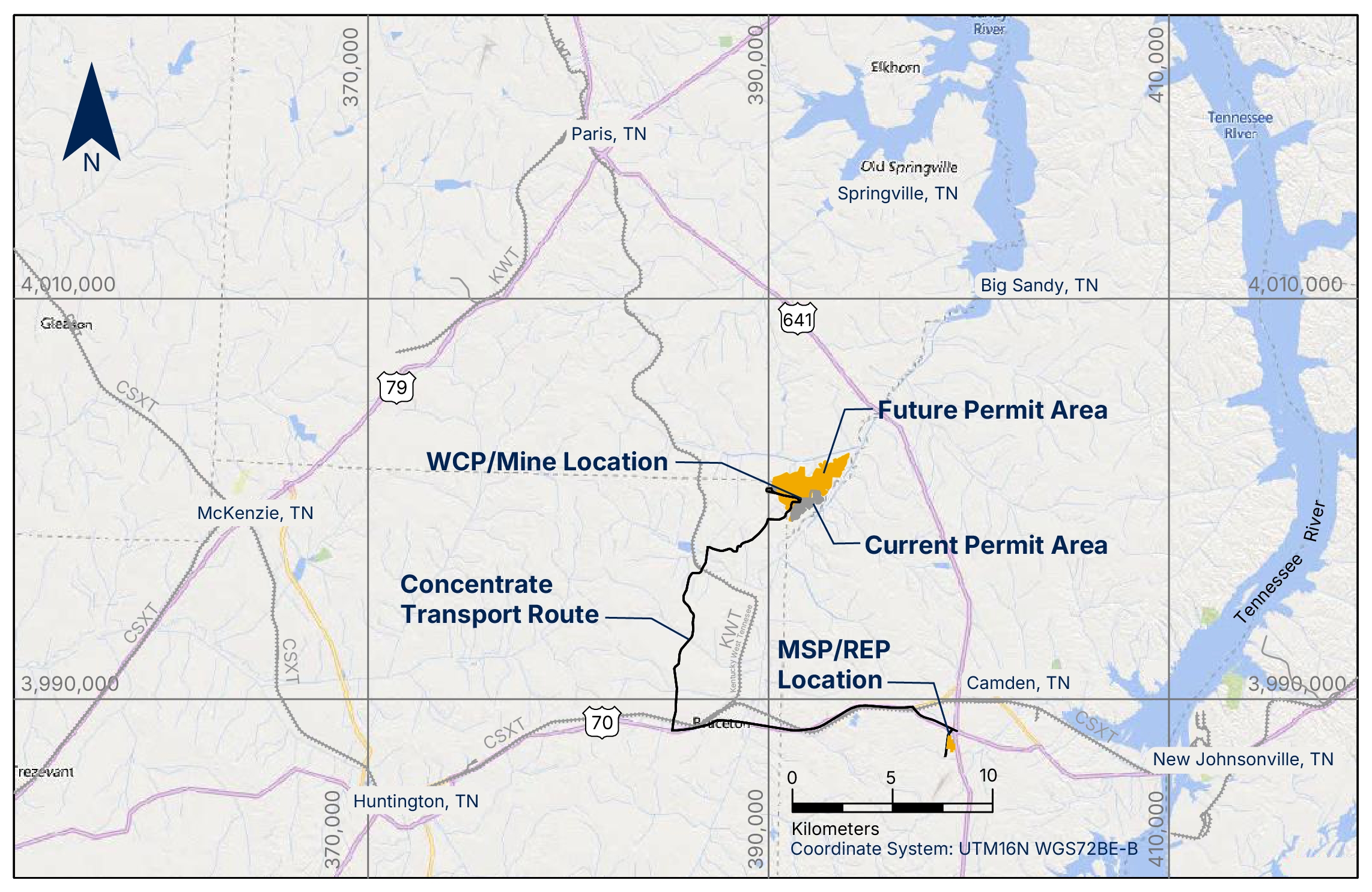

Infrastructure and Logistics

The Titan Project benefits from an established U.S. industrial location with access to road and rail infrastructure, along with proximity to potential domestic customers. General access to the

Study Area is via a well-developed network of primary and secondary roads, including mine and WCP access via paved and maintained state and county roads. The MSP and REP sites will be accessed primarily via U.S. Highway 70, and an operating

railyard exists approximately 7 miles from the MSP and REP site.

The Study site can be accessed via Highway 641 north 41.0 km (25.5 miles) from Interstate 40 near the town of Camden, Tennessee, Reynoldsburg Road for 1.6 km (1.0 miles), Pleasant Hill Road for

1.6 km (1.0 miles) and the Little Benton Road, a gravel road, for 4.8 km (3.0 miles). Little Benton Road goes through the Study Area.

The existing infrastructure includes power and gas, with 161-kV transmission lines near the Project area. IperionX intends to implement 100% renewable power sourcing options for the Titan Project.

Water supply can either be sourced from nearby surface water bodies or from shallow groundwater sources.

West Tennessee is home to a large and diversified workforce, with personnel assumed to live in surrounding communities, and no accommodation camp is expected to be required. There are a number of

local active sand mining, gravel mining and timber operations in the area, which are expected to be sources of experienced labor for IperionX’s operations.

Figure 14: Titan Project mine and process plant locations.

The property location for the wet concentrator plant and mining area associated with the Titan Project is split between Benton and Carroll Counties in Tennessee, with the proposed wet concentrator

plant to reside in Carroll County. The proposed rare earth plant and mineral separation plant will reside in Benton County outside the municipal limits of Camden, Tennessee. Distance between the wet concentrator plant and mineral separation

plant is approximately 29 km (18 miles) using county, state, and U.S. routes. CSX Transportation operates a rail yard approximately 11 km (7 miles) from the mineral separation plant site. The movement of heavy mineral concentrate from the wet

concentrator plant to the mineral separation plant/rare earth plant will be conducted by road trucking. Transportation of ROM and tailings materials between the mine pits and the wet concentrator plant will be conducted by conveyor belts.

27

The Titan Project infrastructure concept reflects a staged, modular development approach designed to reduce execution risk, with development of the wet concentrator plant and the mineral

separation plant occurring in Phase 1 and expanded in Phase 2. Development of the rare earth plant will be carried out in Phase 1.

Government Support and Strategic Importance

Titan is strategically positioned at the intersection of U.S. critical minerals policy, defense industrial base resilience, advanced manufacturing and domestic titanium supply chain development.

The Project has the potential to provide a domestic source of critical minerals (as defined by the U.S. government) including titanium feedstocks, zircon and HREC, into supply chains that are currently exposed to high levels of foreign

concentration and geopolitical risk.

The Titan Project DFS was funded by the U.S. Department of War (“DoW”), via the Industrial Base Analysis and Sustainment program (“IBAS”), as part of a broader $47.1 million funding contract to

accelerate the development of a mineral to metal supply chain in the U.S., leveraging both IperionX’s Titan Project as well as its titanium technology portfolio. DFS funding of approximately $5.0 million was awarded and obligated under the IBAS

program in February 2025.

The Titan Project’s strategic value is underpinned by the following themes:

| ■ |

Critical minerals supply security: Titan would produce minerals used in titanium dioxide, titanium metal, ceramics, foundry, advanced manufacturing, permanent magnets,

defense systems and energy-transition technologies.

|

| ■ |

Domestic production: The Project is located in Tennessee, enabling domestic production of critical mineral concentrates and reducing exposure to long global supply

chains.

|

| ■ |

Titanium supply chain integration: IperionX’s broader titanium strategy provides a potential downstream pathway for titanium feedstocks, supporting a more integrated

U.S. titanium ecosystem.

|

| ■ |

Rare earth resilience: HREC production provides exposure to rare earth elements, including heavy rare earths, that are important to magnet, defense and high-performance

technology supply chains.

|

| ■ |

Heavy rare earth enriched product: Titan’s HREC product lines are enriched in heavy rare earth oxides, most notably Dy, Tb, and Y, which are especially at risk for

foreign import reliance in the U.S.

|

| ■ |

Industrial policy alignment: The Project is aligned with U.S. policy themes focused on critical minerals, defense production, re-shoring, domestic manufacturing and

supply chain resilience.

|

The Study Area location in western Tennessee represents the eastern flank of the Mississippi Embayment, a large, southward-plunging syncline within the Gulf Coastal Plain.

The McNairy Formation represents a pro-grading deltaic environment during a regressive marine sequence. This deposition model is supported by the coarsening upward sequence grading from the glauconitic clay-rich Coon Creek Formation to the

finer grained lower member of the McNairy Formation to the coarser grained upper member of the McNairy Formation.

The main mineralized zone at the Study Area is hosted stratigraphically in the lower member of the McNairy Formation, which dips gently to the west in the Study Area. The upper zone is also

mineralized in some areas. Mineralization in the lower member had been traced for over 6.0 km along strike.

The base of mineralization range is relatively level from 81 meters (m) to 112 m (266 feet (ft) to 367 ft) above current sea level. Mineralization varies from 5 m to 67 m (16 ft to 220 ft) thick

and averages 28 m (92 ft) in thickness. Mineralization primarily occurs in two zones within the McNairy Formation. The main mineralized zones are interrupted by low-grade sand. The primary minerals associated with the mineralized horizons

are altered ilmenite, zircon, rutile, staurolite, kyanite, monazite and xenotime. The Gangue minerals are predominantly quartz and clays. Though extensive basement faulting is present in the region, it does not appear to impact the

stratigraphy at the scale of this Project.

28

Drilling on the Study Area comprises 156 drill holes. This includes 16 reverse circulation holes (total drilled length of 837 m or 2,746 ft) and 140 roto-sonic drill holes (total drilled length

of 5,644 m or 18,517 ft). Across all Titan properties, including those outside of the Study, IperionX has drilled 313 holes (total drilled length of 11,382 m or 37,343 feet). All exploration drilling was completed by IperionX.

The area covered by the drilling is roughly 6.6 km (4.1 miles) (north-south) by 3.7 km (2.3 miles) (east-west); the area that hosts the Mineral Resource estimate is further broken up into several

areas based on land holdings (land agreements). These range from 1.58 hectare (ha) (3.9 acres) for the smallest area to 161 Ha (397 acres) for the largest area. Drill hole spacing is generally 150 x 300 m (492 x 984 ft). Some areas have

difficult access and drill spacing in those areas is wider spaced, approximately up to 300 x 600 m (984 x 1,969 ft).

There are an additional 11 roto-sonic drill holes completed as part of a hydrogeological study by HDR Engineering, Inc. These holes were drilled on IperionX’s behalf. In 2025, an additional 62

holes were drilled by S&ME, Inc. for geotechnical evaluations.

Geoprobe drill core samples, typically 3 m (9.8 ft) in length, were collected directly from the plastic sample sleeves at the drill site. Some interpretation was involved as the material could

expand or compact as it was recovered from the core barrel into the plastic sleeve. Samples were collected at regular 1.5-m (4.9 ft) intervals unless geological contacts were encountered. Sample length ranged from 0.3 m (1.0 ft) to 4.5 m

(14.8 ft).

The unconsolidated sonic cores were sampled by splitting the core in half lengthwise using a machete, then recovering an even split with a trowel along the entire length of the sample interval.

The sample volume weights were about 2 kilograms (kg) (4.4 pounds (lbs)) and were appropriate for the analytical method(s) being used. Samples were collected directly to pre-labeled/pre-tagged sample bags; the remaining sample was further

split into a replicate/archival sample. What sample remained after these steps was used to backfill the drill hole.

Drill samples were sent to the SGS facility in Lakefield, ON, Canada and Bureau Veritas in Perth, Australia. SGS is a qualified third-party laboratory that is independent of IperionX. SGS

Lakefield is accredited as an ISO 17025 facility for selected analytical techniques. Samples were subjected to standard mineral sand industry assay procedures of size fraction analysis, heavy-liquid separation, and chemical analysis.

Accuracy monitoring was addressed by submission of in-house heavy mineral sands standards developed specifically for the Project. There is no commercially available standard reference material

for heavy mineral sands. It is a common practice within heavy mineral sands exploration and operations to generate standards that represent a matrix match to the target material being analyzed.

Assayed samples of THM% in the Lower McNairy Formation were used to derive variograms. Variogram features exhibit the spatial continuity of the sample spacing. The variogram sill factor along

with the known drill hole spacing were used to support the Mineral Resource confidence classification ranges of the deposit.

A block model was created to encompass the Study Area extent and estimate the mineral sands deposit resources. The model was oriented with a bearing of 30 degrees east of north, an orientation

near the apparent depositional trend of the mineral sands. Block cell dimensions of the model are 25 m*25 m*1.524 m (X*Y*Z). For block model development, the digital topographic surface established the overlying bounding surface. Blocks

above the topography were coded as air and excluded from any resource or volume estimates. Gap spaces that exist between the base of the overburden and the top of the Upper McNairy Formation were assigned to waste material (and were therefore

handled with the overburden).

Two testwork programs were conducted for the mineral resource area, one in 2021 and the second in 2023. All testwork was completed on behalf of IperionX.

Assays were conducted by SGS Lakefield, and Bureau Veritas in Perth, Australia, using X-ray fluorescence (XRF), laser ablation/inductively-coupled plasma mass spectrometry (ICP–MS) and

quantitative evaluation of materials by scanning electron microscopy (QEMSCAN) analytical methods. The final products, ilmenite, rutile, zircon, rare earth mineral concentrate, were produced from the 2023 testwork. Ilmenite graded 64.9% TiO2,

and the rutile graded 91.2% TiO2. The zircon graded 66.8% ZrO2. The rare earth mineral concentrate had a total rare earth oxide grade of 59.1%. The product grades generally align with 2021 scoping testwork results and were considered to be

saleable products.

29

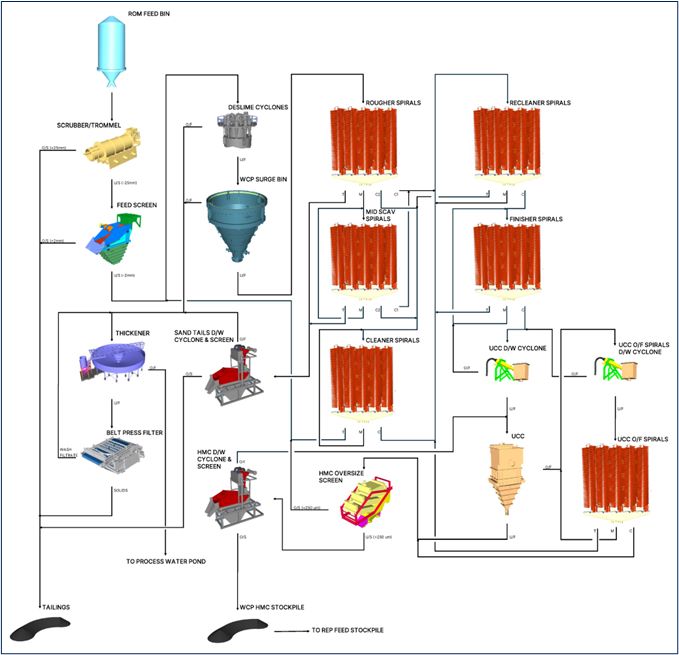

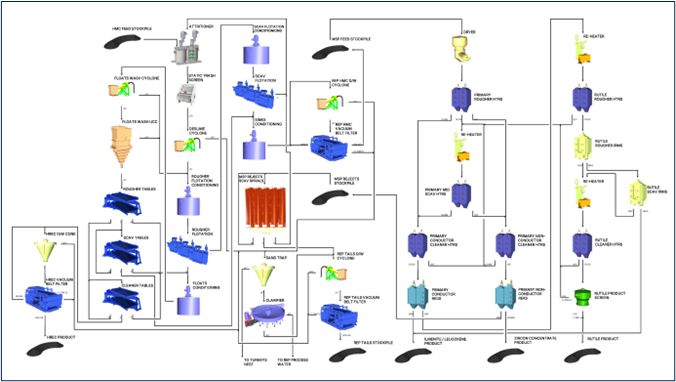

The testwork showed that high-quality ilmenite, rutile, zircon products could be achieved using conventional separation equipment through a typical wet concentrator plant, and fine and coarse

mineral separation plant flowsheet. A rare earth mineral concentrate product was created at a high monazite recovery using a wet rare earth mineral concentrate circuit.

Circuit simulation models were generated for the wet concentration plant, rare earth mineral plant and mineral separation plant flowsheets to evaluate recycle streams and resultant mass flows.

The expected future performance of the processing plant was based on metallurgical testwork results and benchmarked against other deposits that have similar characteristics to the Titan deposit. The simulated recoveries for in-size samples

(+45- micron material) from ROM to products are: rare earth mineral recovery of 82.6%; ilmenite recovery of 79.7%; rutile recovery of 66.9%; zircon recovery of 77.6%.

The resource classification was determined based on drill hole density reflecting the geological confidence; firstly, from hole locations with QEMSCAN analysis and secondly from all drill holes

with total heavy minerals and the geostatistical variogram model. To prevent stand-alone classification pods, radial arcs from points of measurement were required to intersect with an adjacent arc of the same classification. Therefore,

isolated, stand-alone drill holes with QEMSCAN samples were not assigned Measured classification and similarly, stand-alone drill holes with total heavy minerals were not assigned an Indicated classification.

A bottom cut-off grade of 0.4% THM was used in the constraining pit shell, on the basis that the incremental cost of selectively extracting this material, hauling it to a long-term stockpile, and

subsequently reclaiming and re-placing the material into a mine void for progressive rehabilitation would be higher than the net cost (operating cost less revenue) of the central case method. The central case method is the processing of this

material, extracting the contained valuable critical minerals for sale and immediately returning the remaining material, mostly silica sand, back to the deposit void. An additional pit optimization was completed to generate the finalized mine

plan pit shell used in the conversion of Mineral Resources to Ore Reserves.

The Titan Project hosts a Mineral Resource of approximately 445.7 million tons at 2.1% total heavy mineral (“THM”), containing approximately 9.16 million tons of THM with an assemblage of zircon,

rutile, ilmenite and rare earth elements. Mineral Resources are reported using the Mineral Resource definitions set out in the 2012 JORC Code on a 100% basis. The reference point for the estimate is in situ, and the Mineral Resource is

inclusive of Ore Reserves.

30

|

Mineral Resource Estimate

|

In situ tons

|

THM

|

THM

|

THM Assemblage

|

||||

|

Zircon

|

Rutile

|

Ilmenite

|

REE

|

|||||

|

(%)

|

(t)

|

(%)

|

(%)

|

(%)

|

(%)

|

|||

|

Inclusive of Reserve

|

||||||||

|

Measured (M)

|

120,434,000

|

2.5

|

3,060,000

|

11.1

|

9.5

|

40.9

|

1.5

|

|

|

Indicated (I)

|

28,388,000

|

2.9

|

828,000

|

11.8

|

9.2

|

52.0

|

1.5

|

|

|

Total M+I

|

148,823,000

|

2.6

|

3,887,000

|

11.2

|

9.4

|

43.2

|

1.5

|

|

|

Inferred (Inf)

|

-

|

-

|

-

|

-

|

-

|

-

|

-

|

|

|

Total M+I+Inf

|

148,823,000

|

2.6

|

3,887,000

|

11.2

|

9.4

|

43.2

|

1.5

|

|

|

Exclusive of Reserve

|

||||||||

|

Measured (M)

|

96,851,000

|

1.5

|

1,489,000

|

10.4

|

9.2

|

40.1

|

1.2

|

|

|

Indicated (I)

|

102,190,000

|

2.0

|

2,013,000

|

9.8

|

10.2

|

38.9

|

1.5

|

|

|

Total M+I

|

199,041,000

|

1.8

|

3,502,000

|

10.0

|

9.8

|

39.4

|

1.4

|

|

|

Inferred (Inf)

|

97,832,000

|

1.8

|

1,774,000

|

9.3

|

9.6

|

38.0

|

1.2

|

|

|

Total M+I+Inf

|

296,872,000

|

1.8

|

5,276,000

|

9.8

|

9.7

|

39.0

|

1.3

|

|