Fourth Quarter and Full Year 2025 Results March 9, 2026

Important Disclosure This presentation is intended to provide general information

only and is not, and should not be considered, as an offer to purchase or sell the Company’s securities, or a proposal to receive such offers. In addition, this presentation is not an offer to the public of the Company’s securities. By

attending or viewing this presentation, each attendee (“Attendee”) agrees that he or she (i) has read this disclaimer, (ii) is bound by the restrictions set out herein, (iii) is permitted, in accordance with all applicable laws, to receive such

information, (iv) is solely responsible for his or her own assessment of the business and financial position of the Company and (v) will conduct his or her own analysis and be solely responsible for forming the Attendee's view of the potential

future performance of the Company’s business. This presentation includes projections, guidance, forecasts, estimates, assessments and other information pertaining to future events and/or matters, whose materialization is uncertain and is

beyond the Company’s control, and which constitute forward looking statements (within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Israeli

Securities Law, 5728-1968). Many of the forward-looking statements contained in this presentation can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “estimate”

and “potential,” among others. Forward-looking statements include, but are not limited to, expectations and evaluations relating to the Company’s business and financial targets and strategy, the integration of the Company’s technology in

various systems and industries, the advantages of the Company’s existing and future products, timetables regarding completion of the Company’s developments and the Company’s intentions in relation to various industries, the Company’s intentions

in relation to the creation of collaborations and engagements in licensing agreements, production and distribution in various countries, and other statements regarding our intent, belief or current expectations. Forward-looking statements are

based on our management’s beliefs and assumptions and on information currently available to our management. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the

forward-looking statements due to various factors, including, but not limited to: our expectations regarding general market conditions, including as a result of the COVID-19 pandemic and other global economic trends; changes in consumer tastes

and preferences; fluctuations in inflation, interest rates and exchange rates in the global economic environment; the availability of qualified personnel and the ability to retain such personnel; changes in commodity costs, labor, distribution

and other operating costs; our ability to implement our growth strategy; changes in government regulation and tax matters; other factors that may affect our financial condition, liquidity and results of operations; general economic, political,

demographic and business conditions in Israel, including the ongoing war in Israel that began on October 7, 2023 and global perspectives regarding that conflict; the success of operating initiatives, including advertising and promotional

efforts and new product and concept development by us and our competitors; factors relating to acquisitions made by the Company, including our ability to effectively and efficiently integrate acquired businesses into our existing business; and

other risk factors discussed under “Risk Factors” in our annual report on Form 20-F filed with the SEC on March 4 , 2025 (our “Annual Report"). The preceding list is not intended to be an exhaustive list of all of our forward-looking

statements. The forward-looking statements are based on our beliefs, assumptions and expectations of future performance, taking into account the information currently available to us. These statements are only estimates based upon our current

expectations and projections about future events. There are important factors that could cause our actual results, levels of activity, performance or achievements to differ materially from the results, levels of activity, performance or

achievements expressed or implied by the forward-looking statements. In particular, you should consider the risks provided under “Risk Factors” in our Annual Report. You should not rely upon forward-looking statements as predictions of future

events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that future results, levels of activity, performance and events and circumstances reflected in the forward-looking

statements will be achieved or will occur. Each forward-looking statement speaks only as of the date of the particular statement. Except as required by law, we undertake no obligation to update publicly any forward-looking statements provided

in this presentation for any reason, to conform these statements to actual results or to changes in our expectations. In addition, the presentation includes data published by various bodies, and data provided to the Company in the framework

of cooperation engagements, concerning the industry, competitive position and markets in which the Company operates, whose content was not independently verified by the Company, such that the Company is not responsible for the accuracy or

completeness of such date or whether the data is up-to-date, and Company takes no responsibility for any reliance on such data. Management estimates contained in this presentation are derived from publicly available information released by

independent industry analysts and other third-party sources, as well as data from the Company's internal research, and are based on assumptions made by the Company upon review of such data, and the Company's experience in, and knowledge of, the

industry and markets in which the Company operates. Although the Company believes these management estimates are reasonable, projections, assumptions and estimates of the future performance of the industry in which the Company operates and the

Company's future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described above. These and other factors could cause results to differ materially from those expressed in the estimates

made by independent parties and by the Company. Industry publications, research, surveys and studies generally state that the information they provide has been obtained from sources believed to be reliable, but that the accuracy and

completeness of such information is not guaranteed. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this

presentation. In addition to various operational metrics and financial measures in accordance with accounting principles generally accepted under International Financial Reporting Standards, or IFRS, this presentation contains Adjusted

EBITDA, Free Cash Flow and Adjusted OPEX, each a non-IFRS financial measure provided to help evaluate our past results and future prospects. Please refer to the appendix for of this presentation for a definition of Adjusted EBITDA, Free Cash

Flow and Adjusted OPEX as well as reconciliations of Adjusted EBITDA to net income (loss), Free Cash Flow to operating cash and Adjusted OPEX to OPEX. Due to the inherent difficulty in forecasting and quantifying the amounts of certain items

that are necessary for such reconciliation, the Company is not able, without unreasonable effort, to provide a reconciliation of forward-looking Adjusted EBITDA to IFRS net income (loss), in particular because items such as finance expenses and

issuance and acquisition costs used to calculate projected net income (loss) vary dramatically based on actual events. Therefore, the Company is not able to forecast on an IFRS basis with reasonable certainty all deductions needed in order to

provide an IFRS calculation of projected net income (loss) at this time. The amount of these deductions may be material and therefore could result in projected IFRS net income (loss) being materially less than projected Adjusted EBITDA

(non-IFRS). The Company and its licensors have proprietary rights to trademarks used in this presentation. Solely for convenience, trademarks and trade names referred to in this presentation may appear without the “®” or “TM” symbols, but

the lack of such references is not intended to indicate, in any way, that the Company will not assert, to the fullest extent possible under applicable law, its rights or the rights of the applicable licensor to these trademarks and trade names.

This presentation also contains trademarks, trade names and service marks of other companies, which are the property of their respective owners and are used here for reference purposes only. Such use of other parties’ trademarks, trade names or

service marks should not be construed to imply a relationship with, or an endorsement or sponsorship of the Company, by any other party. Forward-looking statements, risk factors, and non-GAAP financial measures referenced in this presentation

Today’s Presenters 3 Yair Nechmad CEO & Co-Founder Sagit

Manor CFO Aaron Greenberg CSO 3

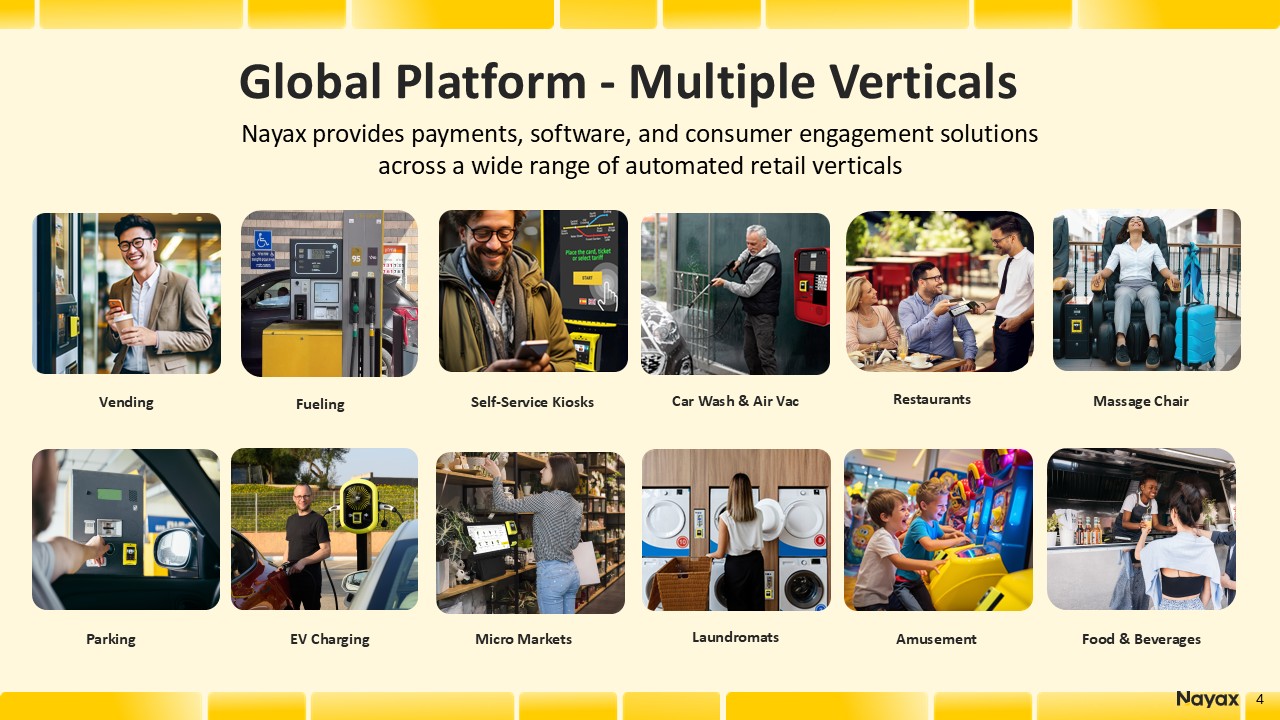

Nayax provides payments, software, and consumer engagement solutions across a wide

range of automated retail verticals Global Platform - Multiple Verticals Massage Chair Fueling Self-Service Kiosks Laundromats Car Wash & Air Vac Amusement Food & Beverages Restaurants Micro Markets EV Charging

Vending Parking 4 4

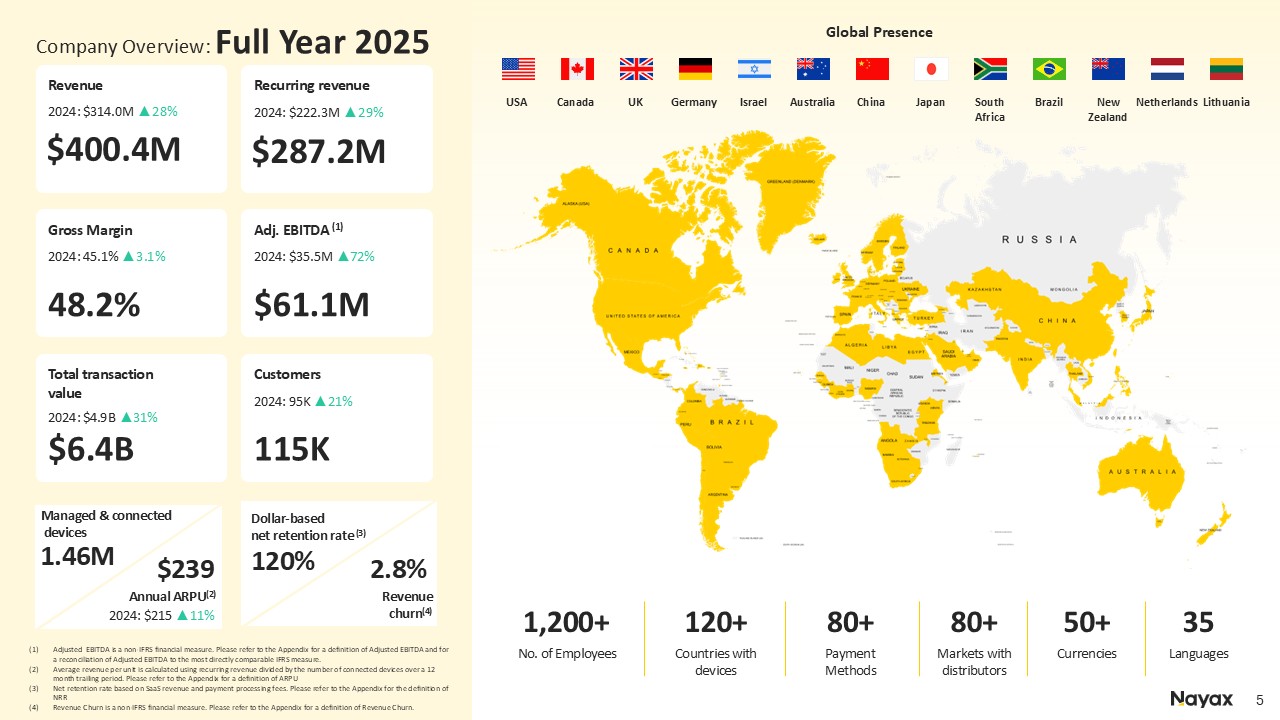

No. of Employees 1,200+ Countries with devices 120+ Payment

Methods 80+ Markets with distributors 80+ Currencies 50+ Languages 35 Company Overview: Full Year 2025 Revenue $400.4M 2024: $314.0M ▲28% Recurring revenue $287.2M 2024: $222.3M ▲29% Gross Margin 48.2% 2024: 45.1%

▲3.1% Adj. EBITDA (1) $61.1M 2024: $35.5M ▲72% Total transaction value $6.4B Customers 115K Revenue churn(4) 2.8% 2024: $4.9B ▲31% 2024: 95K ▲21% Dollar-basednet retention rate (3) 120% Adjusted EBITDA is a non-IFRS financial

measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. Average revenue per unit is calculated using recurring revenue divided by the

number of connected devices over a 12 month trailing period. Please refer to the Appendix for a definition of ARPU Net retention rate based on SaaS revenue and payment processing fees. Please refer to the Appendix for the definition of

NRR Revenue Churn is a non-IFRS financial measure. Please refer to the Appendix for a definition of Revenue Churn. 2024 Revenue $314.0M $315.2M (1) 2023: $235.5M ▲33% Global

Presence Canada USA UK Israel Germany Australia China Japan South Africa Brazil New Zealand Netherlands Lithuania Managed & connected devices 1.46M Annual ARPU(2) $239 2024: $215 ▲11%

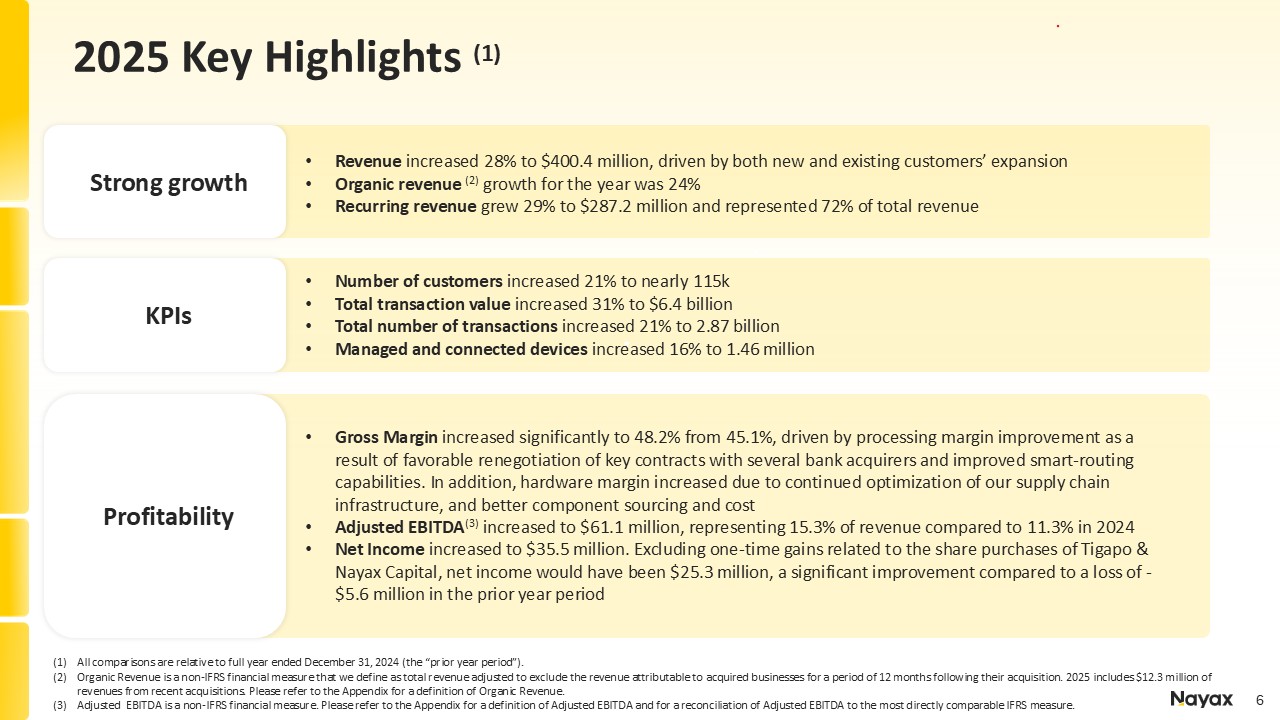

Strong growth Revenue increased 28% to $400.4 million, driven by both new and

existing customers’ expansion Organic revenue (2) growth for the year was 24% Recurring revenue grew 29% to $287.2 million and represented 72% of total revenue Number of customers increased 21% to nearly 115k Total transaction value

increased 31% to $6.4 billion Total number of transactions increased 21% to 2.87 billion Managed and connected devices increased 16% to 1.46 million KPIs Profitability Gross Margin increased significantly to 48.2% from 45.1%, driven by

processing margin improvement as a result of favorable renegotiation of key contracts with several bank acquirers and improved smart-routing capabilities. In addition, hardware margin increased due to continued optimization of our supply chain

infrastructure, and better component sourcing and cost Adjusted EBITDA(3) increased to $61.1 million, representing 15.3% of revenue compared to 11.3% in 2024 Net Income increased to $35.5 million. Excluding one-time gains related to the share

purchases of Tigapo & Nayax Capital, net income would have been $25.3 million, a significant improvement compared to a loss of -$5.6 million in the prior year period All comparisons are relative to full year ended December 31, 2024 (the

“prior year period”). Organic Revenue is a non-IFRS financial measure that we define as total revenue adjusted to exclude the revenue attributable to acquired businesses for a period of 12 months following their acquisition. 2025 includes

$12.3 million of revenues from recent acquisitions. Please refer to the Appendix for a definition of Organic Revenue. Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for

a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. 2025 Key Highlights (1)

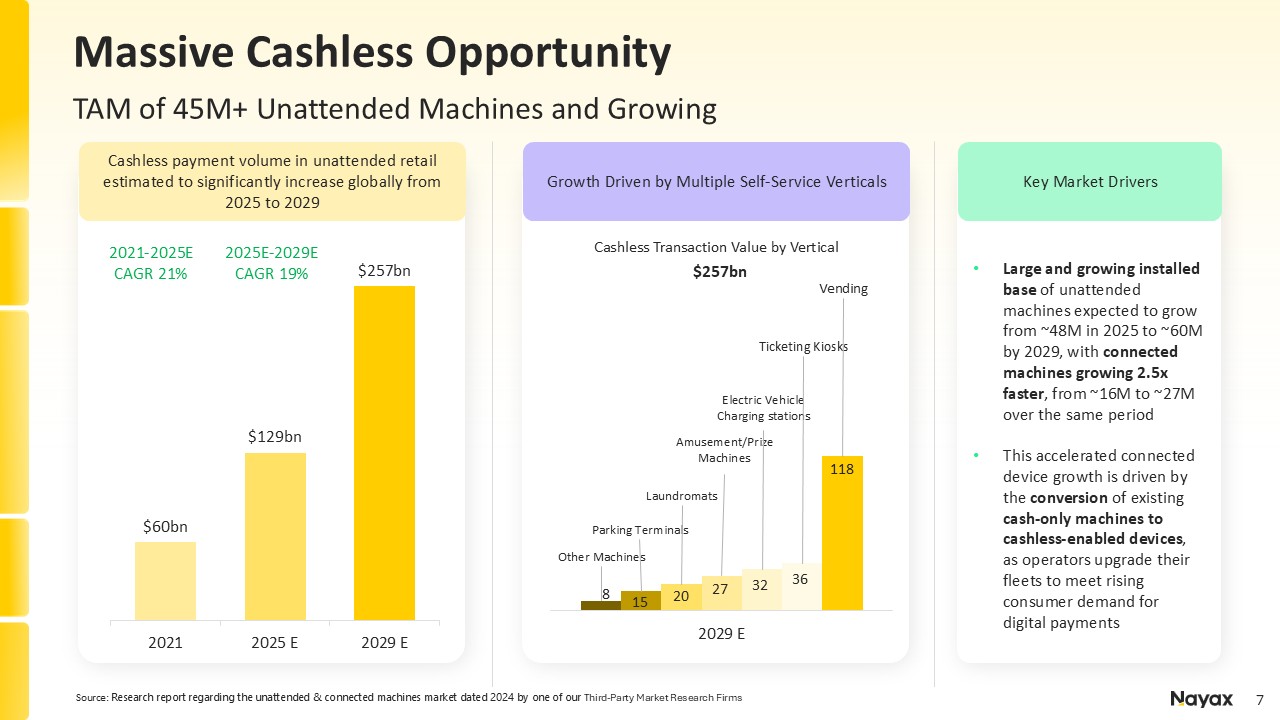

Key Market Drivers Growth Driven by Multiple Self-Service Verticals Source:

Research report regarding the unattended & connected machines market dated 2024 by one of our Third-Party Market Research Firms Cashless Transaction Value by Vertical Large and growing installed base of unattended machines expected to

grow from ~48M in 2025 to ~60M by 2029, with connected machines growing 2.5x faster, from ~16M to ~27M over the same period This accelerated connected device growth is driven by the conversion of existing cash-only machines to cashless-enabled

devices, as operators upgrade their fleets to meet rising consumer demand for digital payments Cashless payment volume in unattended retail estimated to significantly increase globally from 2025 to 2029 2021-2025E CAGR 21% 2025E-2029E CAGR

19% Massive Cashless Opportunity TAM of 45M+ Unattended Machines and Growing $257bn 8 15 20 27 32 36 118

Where Complexity Becomes a Competitive Advantage Gov. / Safety Payment

security Health Telecommunications Global Regulatory Infrastructure Barriers To Entry Integrations with unattended machines in multiple verticals Comprehensive, modular end-to-end solutions Proprietary Integrated POS

devices Multi-jurisdictional payments acceptance network Large installed customer base Addressing SME and Enterprise customers Multiple retailer needs for every merchant in one system Significant automation, AI, and data analytics

tools Global financial regulations and compliance requirements Connection to multiple financial Institutions and banks

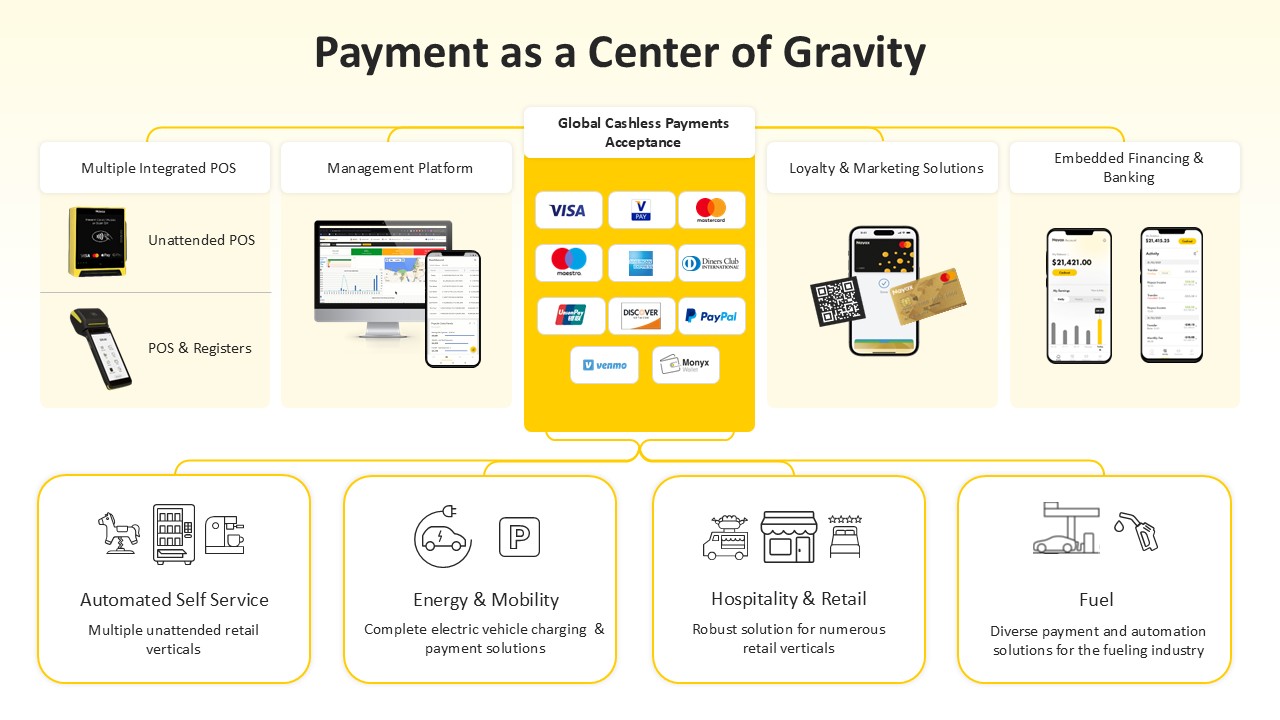

Payment as a Center of Gravity Global Cashless Payments Acceptance Multiple

Integrated POS Unattended POS POS & Registers Management Platform Loyalty & Marketing Solutions Embedded Financing & Banking Multiple unattended retail verticals Automated Self Service Hospitality & Retail Robust

solution for numerous retail verticals Complete electric vehicle charging & payment solutions Energy & Mobility Diverse payment and automation solutions for the fueling industry Fuel

Core Strategic Areas of Focus

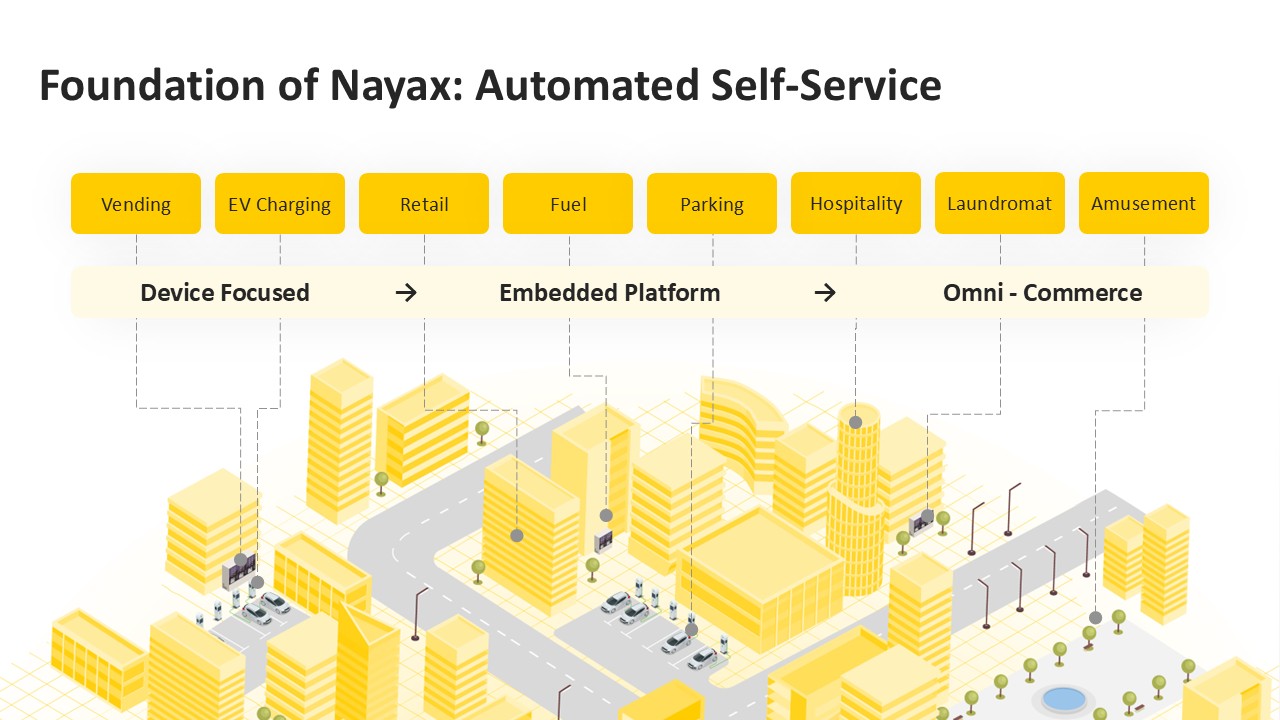

Foundation of Nayax: Automated Self-Service Vending EV

Charging Retail Fuel Hospitality Laundromat Parking Amusement Device Focused → Embedded Platform → Omni - Commerce

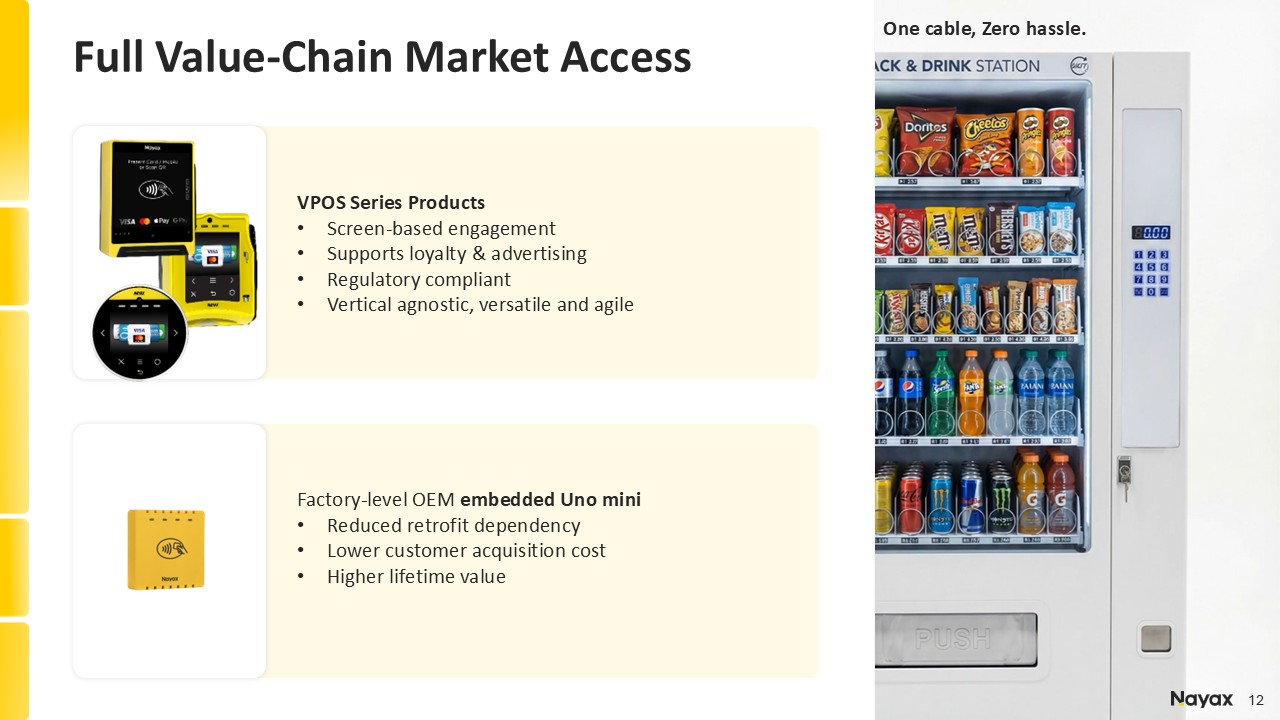

VPOS Series Products Screen-based engagement Supports loyalty &

advertising Regulatory compliant Vertical agnostic, versatile and agile Factory-level OEM embedded Uno mini Reduced retrofit dependency Lower customer acquisition cost Higher lifetime value Full Value-Chain Market Access One cable,

Zero hassle. 12

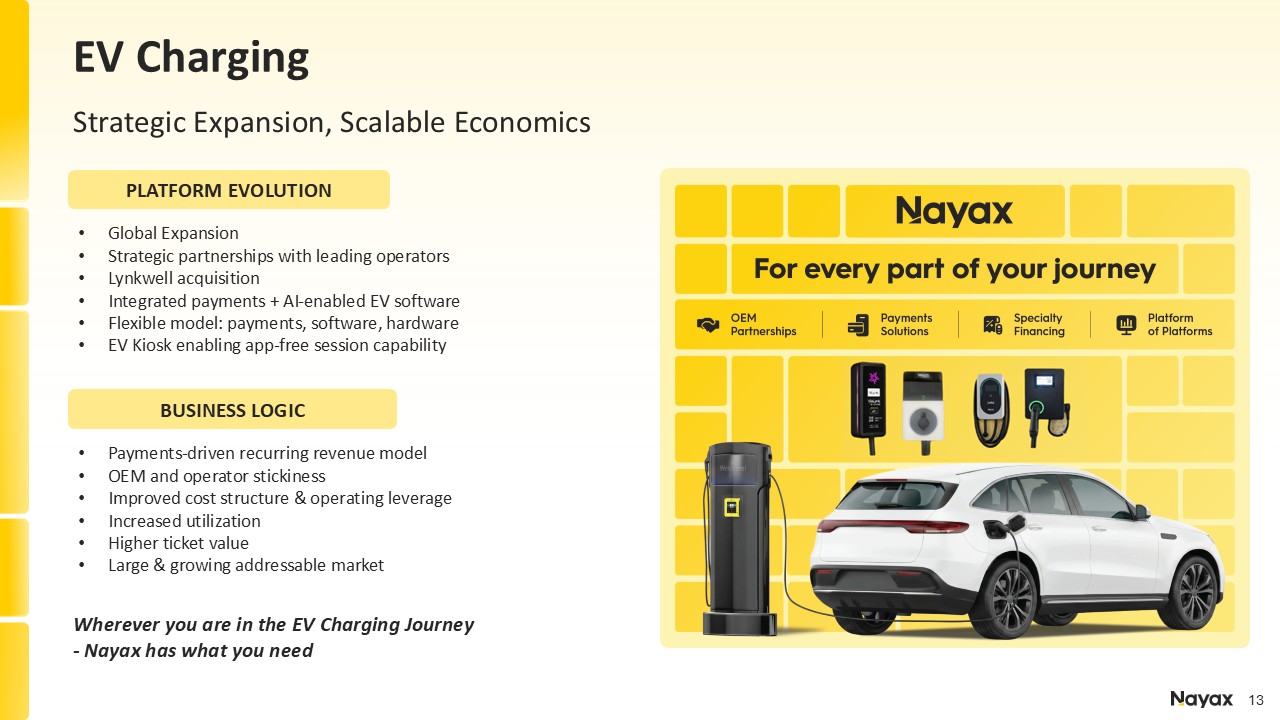

Wherever you are in the EV Charging Journey - Nayax has what you need Global

Expansion Strategic partnerships with leading operators Lynkwell acquisition Integrated payments + AI-enabled EV software Flexible model: payments, software, hardware EV Kiosk enabling app-free session capability PLATFORM

EVOLUTION BUSINESS LOGIC Payments-driven recurring revenue model OEM and operator stickiness Improved cost structure & operating leverage Increased utilization Higher ticket value Large & growing addressable market EV

Charging Strategic Expansion, Scalable Economics

Strategic M&As

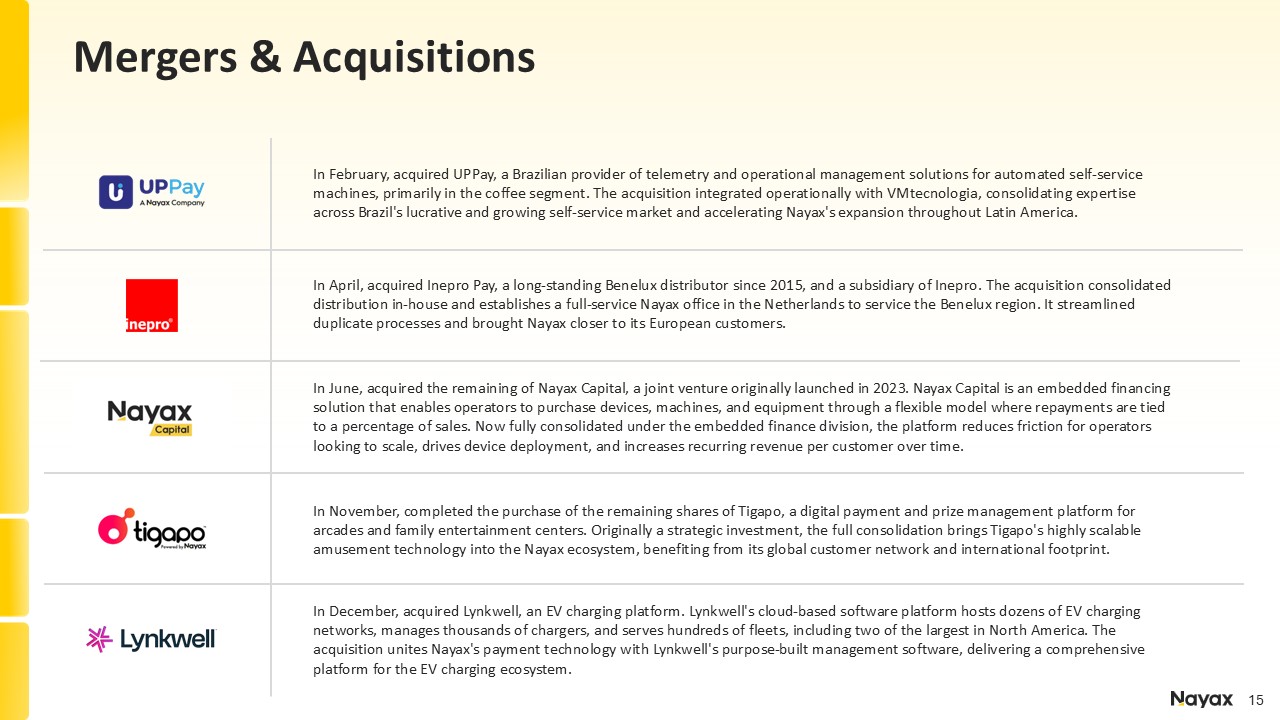

In February, acquired UPPay, a Brazilian provider of telemetry and operational

management solutions for automated self-service machines, primarily in the coffee segment. The acquisition integrated operationally with VMtecnologia, consolidating expertise across Brazil's lucrative and growing self-service market and

accelerating Nayax's expansion throughout Latin America. In April, acquired Inepro Pay, a long-standing Benelux distributor since 2015, and a subsidiary of Inepro. The acquisition consolidated distribution in-house and establishes a

full-service Nayax office in the Netherlands to service the Benelux region. It streamlined duplicate processes and brought Nayax closer to its European customers. In November, completed the purchase of the remaining shares of Tigapo, a digital

payment and prize management platform for arcades and family entertainment centers. Originally a strategic investment, the full consolidation brings Tigapo's highly scalable amusement technology into the Nayax ecosystem, benefiting from its

global customer network and international footprint. In June, acquired the remaining of Nayax Capital, a joint venture originally launched in 2023. Nayax Capital is an embedded financing solution that enables operators to purchase devices,

machines, and equipment through a flexible model where repayments are tied to a percentage of sales. Now fully consolidated under the embedded finance division, the platform reduces friction for operators looking to scale, drives device

deployment, and increases recurring revenue per customer over time. In December, acquired Lynkwell, an EV charging platform. Lynkwell's cloud-based software platform hosts dozens of EV charging networks, manages thousands of chargers, and

serves hundreds of fleets, including two of the largest in North America. The acquisition unites Nayax's payment technology with Lynkwell's purpose-built management software, delivering a comprehensive platform for the EV charging

ecosystem. Mergers & Acquisitions

What’s Next?

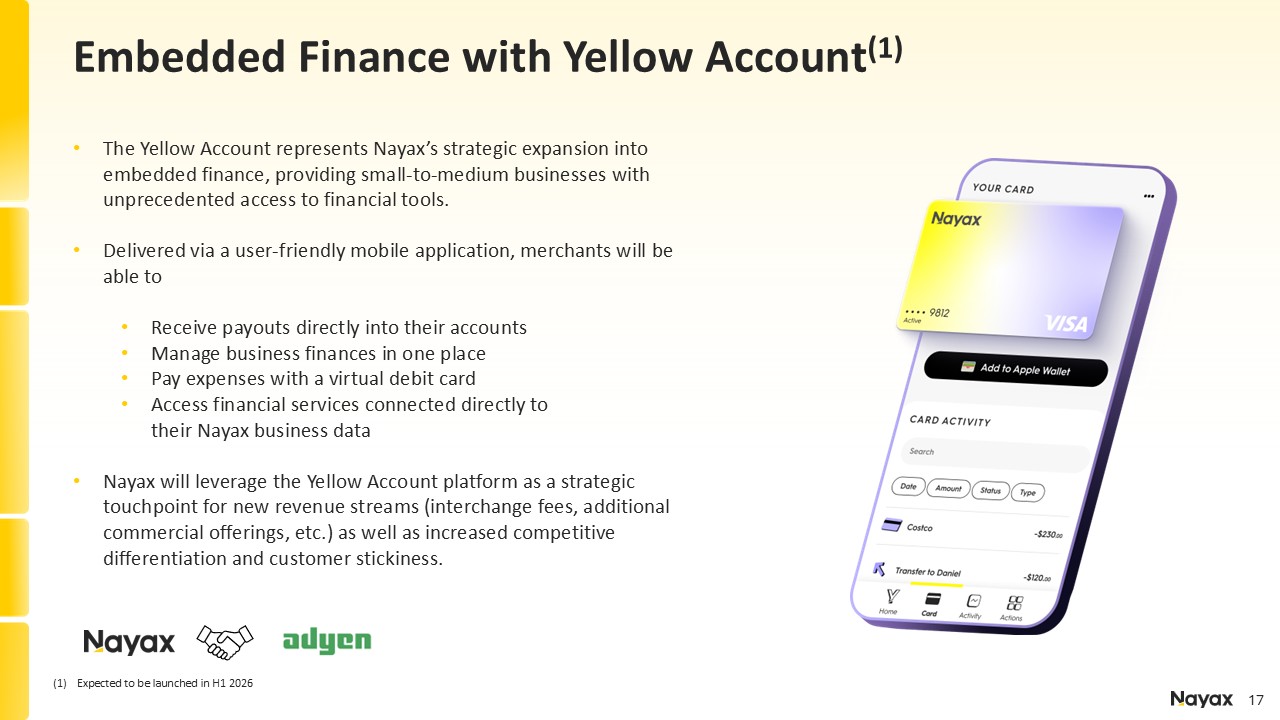

Embedded Finance with Yellow

Account(1) The Yellow Account represents Nayax’s strategic expansion into embedded finance, providing small-to-medium businesses with unprecedented access to financial tools. Delivered via a user-friendly mobile application, merchants

will be able to Receive payouts directly into their accounts Manage business finances in one place Pay expenses with a virtual debit card Access financial services connected directly to their Nayax business data Nayax will leverage the

Yellow Account platform as a strategic touchpoint for new revenue streams (interchange fees, additional commercial offerings, etc.) as well as increased competitive differentiation and customer stickiness. Expected to be launched in H1 2026

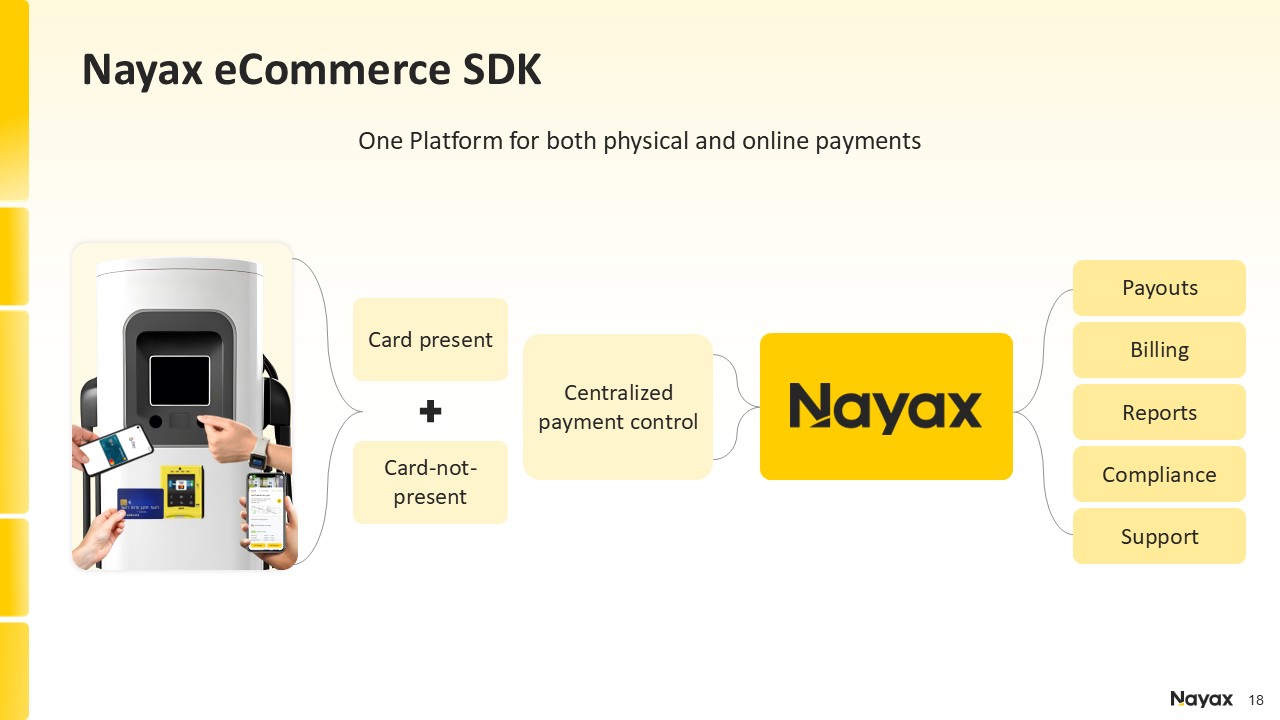

Nayax eCommerce SDK One Platform for both physical and online

payments Centralizedpayment control Payouts Billing Reports Compliance Support Card-not-present Card present

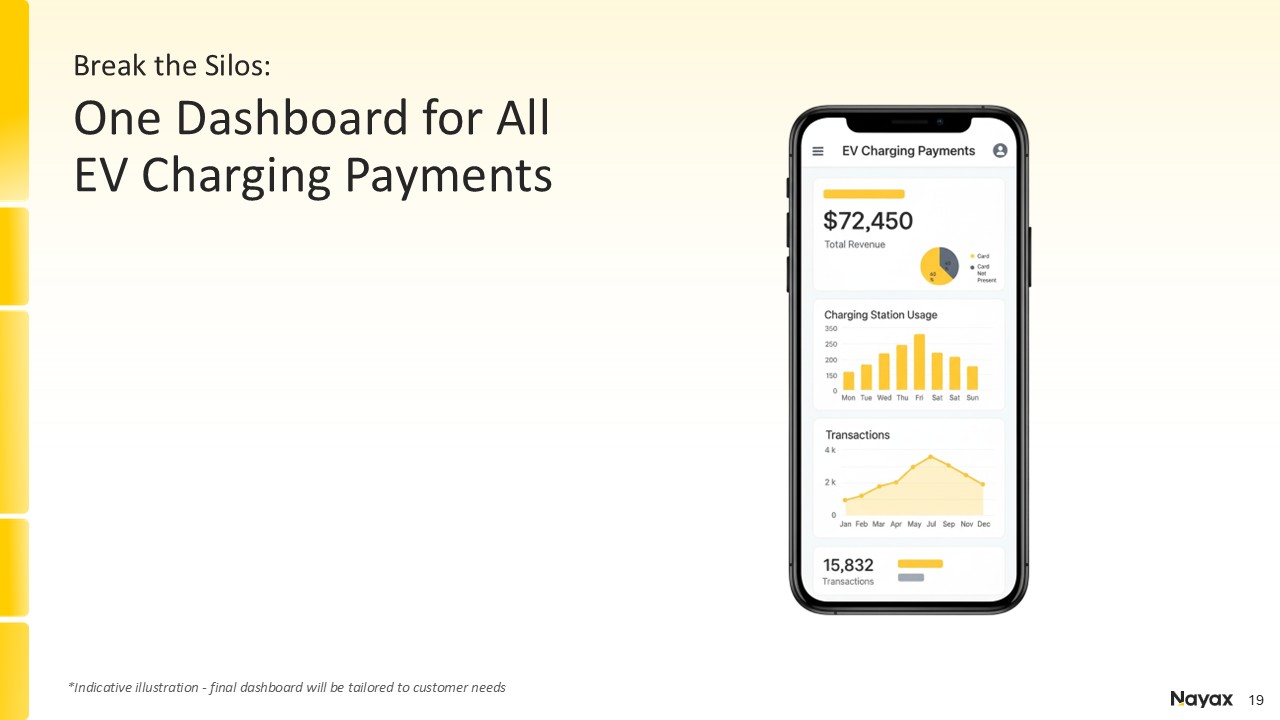

One Dashboard for All EV Charging Payments Break the Silos: *Indicative

illustration - final dashboard will be tailored to customer needs

Financial Performance & Outlook

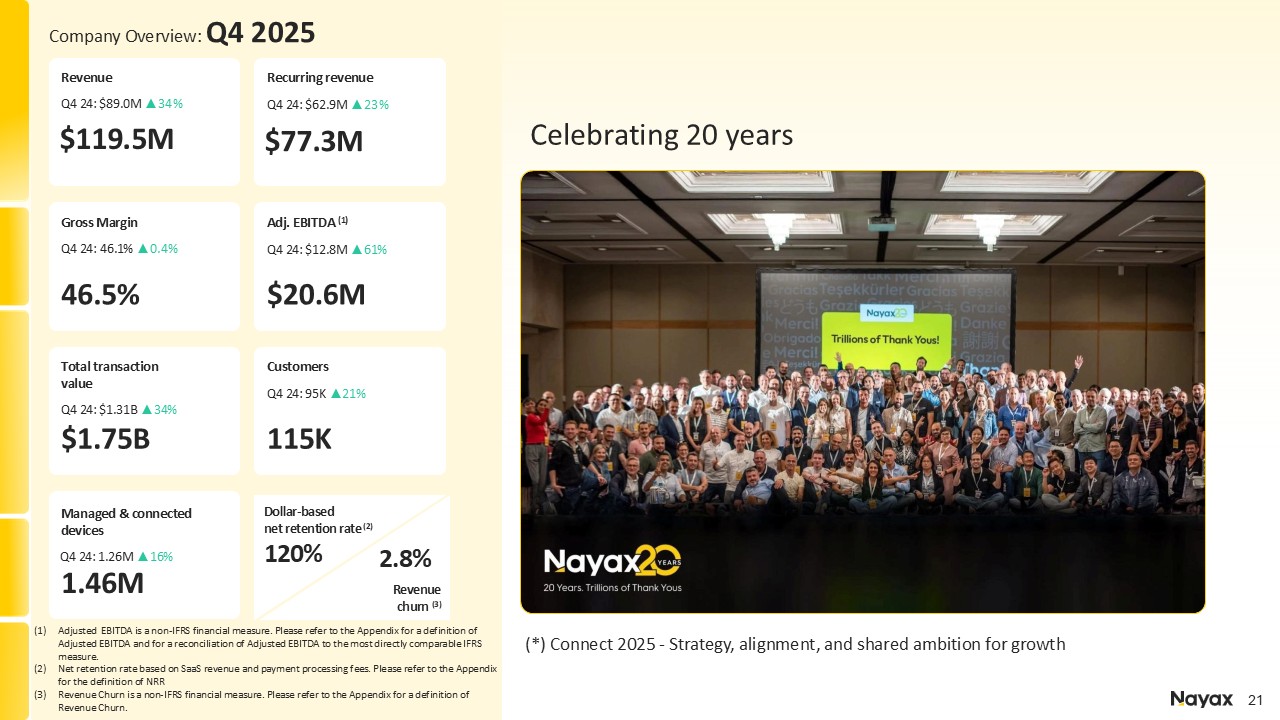

Company Overview: Q4 2025 2025 Revenue $400.4M $314.0M (1) 2024: $314.0M

▲28% 2025 Revenue $400.4M 2024: $314.0M ▲28% . Company Overview: Q4 2025 Revenue $119.5M Q4 24: $89.0M ▲34% Recurring revenue $77.3M Q4 24: $62.9M ▲23% Gross Margin 46.5% Q4 24: 46.1% ▲0.4% Adj. EBITDA (1) $20.6M Q4 24:

$12.8M ▲61% Total transaction value $1.75B Customers 115K Managed & connected devices 1.46M Revenue churn (3) 2.8% Q4 24: $1.31B ▲34% Q4 24: 95K ▲21% Dollar-basednet retention rate (2) 120% Q4 24: 1.26M ▲16% Adjusted

EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. Net retention rate based on SaaS revenue and

payment processing fees. Please refer to the Appendix for the definition of NRR Revenue Churn is a non-IFRS financial measure. Please refer to the Appendix for a definition of Revenue Churn. Celebrating 20 years (*) Connect 2025 - Strategy,

alignment, and shared ambiti

on for growth

Company Overview: Q4 2025 2025 Revenue $400.4M $314.0M (1) 2024:

$314.0M ▲28% 2025 Revenue $400.4M 2024: $314.0M ▲28% . Company Overview: Q4 2025 Revenue $119.5M Q4 24: $89.0M ▲34% Recurring revenue $77.3M Q4 24: $62.9M ▲23% Gross Margin 46.5% Q4 24: 46.1% ▲0.4% Adj. EBITDA

(1) $20.6M Q4 24: $12.8M ▲61% Total transaction value $1.75B Customers 115K Managed & connected devices 1.46M Revenue churn (3) 2.8% Q4 24: $1.31B ▲34% Q4 24: 95K ▲21% Dollar-basednet retention rate (2) 120% Q4 24:

1.26M ▲16% Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. Net retention

rate based on SaaS revenue and payment processing fees. Please refer to the Appendix for the definition of NRR Revenue Churn is a non-IFRS financial measure. Please refer to the Appendix for a definition of Revenue Churn. Celebrating

20 years (*) Connect 2025 - Strategy, alignment, and shared ambition for growth

Company Overview: Q4 2025 2025 Revenue $400.4M $314.0M (1) 2024: $314.0M

▲28% 2025 Revenue $400.4M 2024: $314.0M ▲28% . Company Overview: Q4 2025 Revenue $119.5M Q4 24: $89.0M ▲34% Recurring revenue $77.3M Q4 24: $62.9M ▲23% Gross Margin 46.5% Q4 24: 46.1% ▲0.4% Adj. EBITDA (1) $20.6M Q4 24:

$12.8M ▲61% Total transaction value $1.75B Customers 115K Managed & connected devices 1.46M Revenue churn (3) 2.8% Q4 24: $1.31B ▲34% Q4 24: 95K ▲21% Dollar-basednet retention rate (2) 120% Q4 24: 1.26M ▲16% Adjusted

EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. Net retention rate based on SaaS revenue and

payment processing fees. Please refer to the Appendix for the definition of NRR Revenue Churn is a non-IFRS financial measure. Please refer to the Appendix for a definition of Revenue Churn. Celebrating 20 years (*) Connect 2025 -

Strategy, alignment, and shared ambition for growth

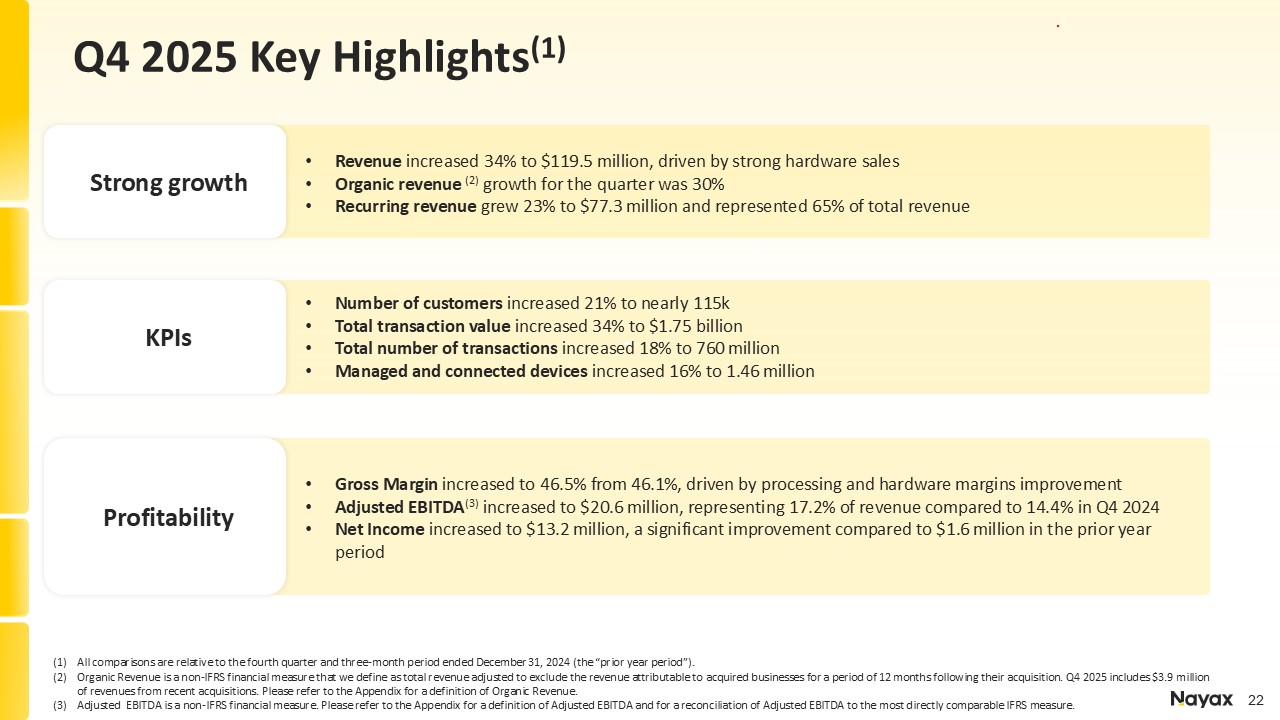

Strong growth Revenue increased 34% to $119.5 million, driven by strong hardware

sales Organic revenue (2) growth for the quarter was 30% Recurring revenue grew 23% to $77.3 million and represented 65% of total revenue Number of customers increased 21% to nearly 115k Total transaction value increased 34% to $1.75

billion Total number of transactions increased 18% to 760 million Managed and connected devices increased 16% to 1.46 million KPIs Profitability Gross Margin increased to 46.5% from 46.1%, driven by processing and hardware margins

improvement Adjusted EBITDA(3) increased to $20.6 million, representing 17.2% of revenue compared to 14.4% in Q4 2024 Net Income increased to $13.2 million, a significant improvement compared to $1.6 million in the prior year period All

comparisons are relative to the fourth quarter and three-month period ended December 31, 2024 (the “prior year period”). Organic Revenue is a non-IFRS financial measure that we define as total revenue adjusted to exclude the revenue

attributable to acquired businesses for a period of 12 months following their acquisition. Q4 2025 includes $3.9 million of revenues from recent acquisitions. Please refer to the Appendix for a definition of Organic Revenue. Adjusted EBITDA

is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. Q4 2025 Key Highlights(1)

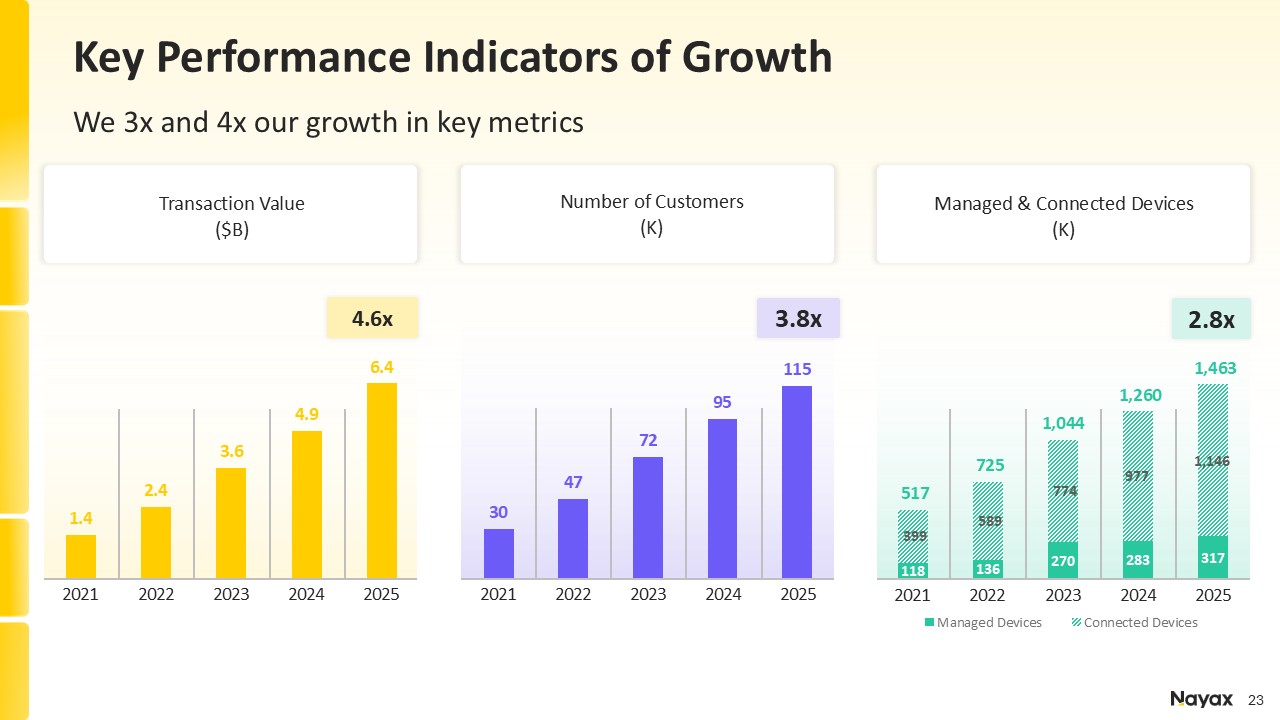

Transaction Value ($B) 2021 2022 2023 2024 4.6x 3.8x 2.8x Number of

Customers (K) Managed & Connected Devices (K) 2025 2021 2022 2023 2024 2025 2021 2022 2023 2024 2025 Key Performance Indicators of Growth We 3x and 4x our growth in key metrics

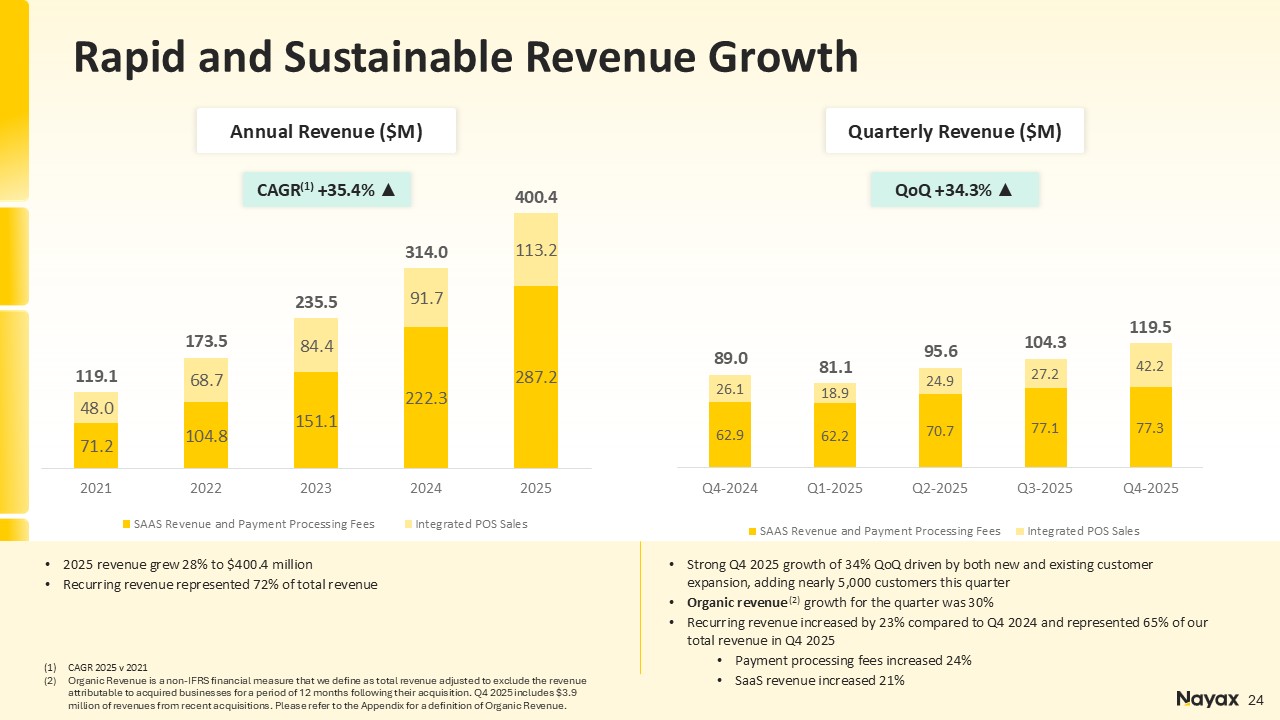

2025 revenue grew 28% to $400.4 million Recurring revenue represented 72% of

total revenue CAGR 2025 v 2021 Organic Revenue is a non-IFRS financial measure that we define as total revenue adjusted to exclude the revenue attributable to acquired businesses for a period of 12 months following their acquisition. Q4 2025

includes $3.9 million of revenues from recent acquisitions. Please refer to the Appendix for a definition of Organic Revenue. CAGR(1) +35.4% ▲ 24 Annual Revenue ($M) Quarterly Revenue ($M) QoQ +34.3% ▲ Strong Q4 2025 growth of 34% QoQ

driven by both new and existing customer expansion, adding nearly 5,000 customers this quarter Organic revenue (2) growth for the quarter was 30% Recurring revenue increased by 23% compared to Q4 2024 and represented 65% of our total revenue

in Q4 2025 Payment processing fees increased 24% SaaS revenue increased 21% Rapid and Sustainable Revenue Growth

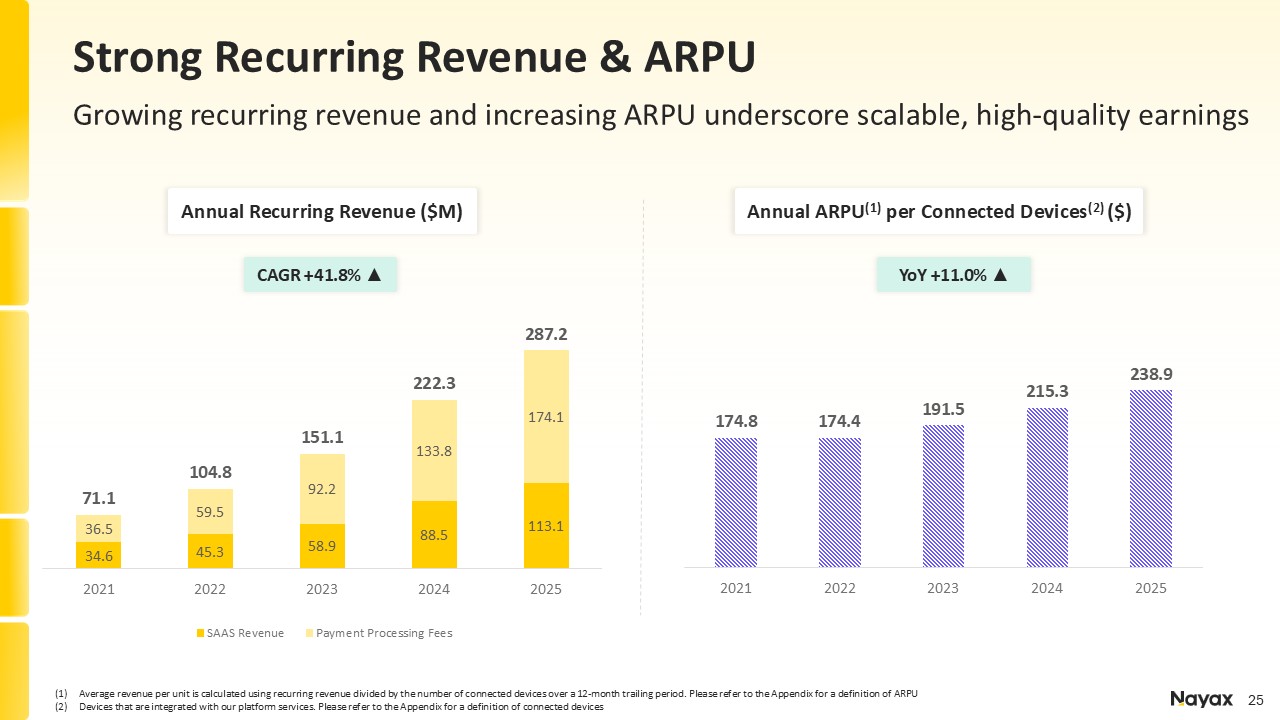

Average revenue per unit is calculated using recurring revenue divided by the

number of connected devices over a 12-month trailing period. Please refer to the Appendix for a definition of ARPU Devices that are integrated with our platform services. Please refer to the Appendix for a definition of connected devices CAGR

+41.8% ▲ Annual Recurring Revenue ($M) Annual ARPU(1) per Connected Devices(2) ($) YoY +11.0% ▲ Strong Recurring Revenue & ARPU Growing recurring revenue and increasing ARPU underscore scalable, high-quality earnings

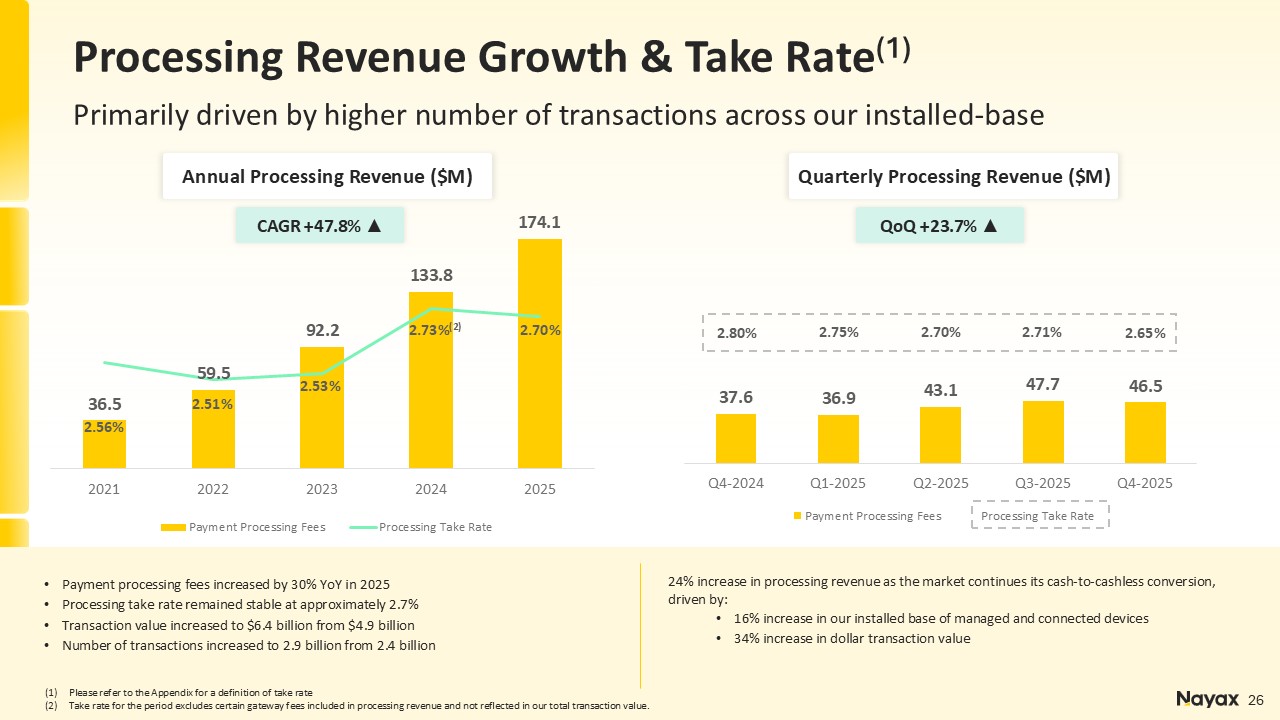

CAGR +47.8% ▲ 26 Annual Processing Revenue ($M) Quarterly Processing Revenue

($M) QoQ +23.7% ▲ Please refer to the Appendix for a definition of take rate Take rate for the period excludes certain gateway fees included in processing revenue and not reflected in our total transaction value. Payment processing fees

increased by 30% YoY in 2025 Processing take rate remained stable at approximately 2.7% Transaction value increased to $6.4 billion from $4.9 billion Number of transactions increased to 2.9 billion from 2.4 billion 24% increase in

processing revenue as the market continues its cash-to-cashless conversion, driven by: 16% increase in our installed base of managed and connected devices 34% increase in dollar transaction value Processing Revenue Growth & Take

Rate(1) Primarily driven by higher number of transactions across our installed-base

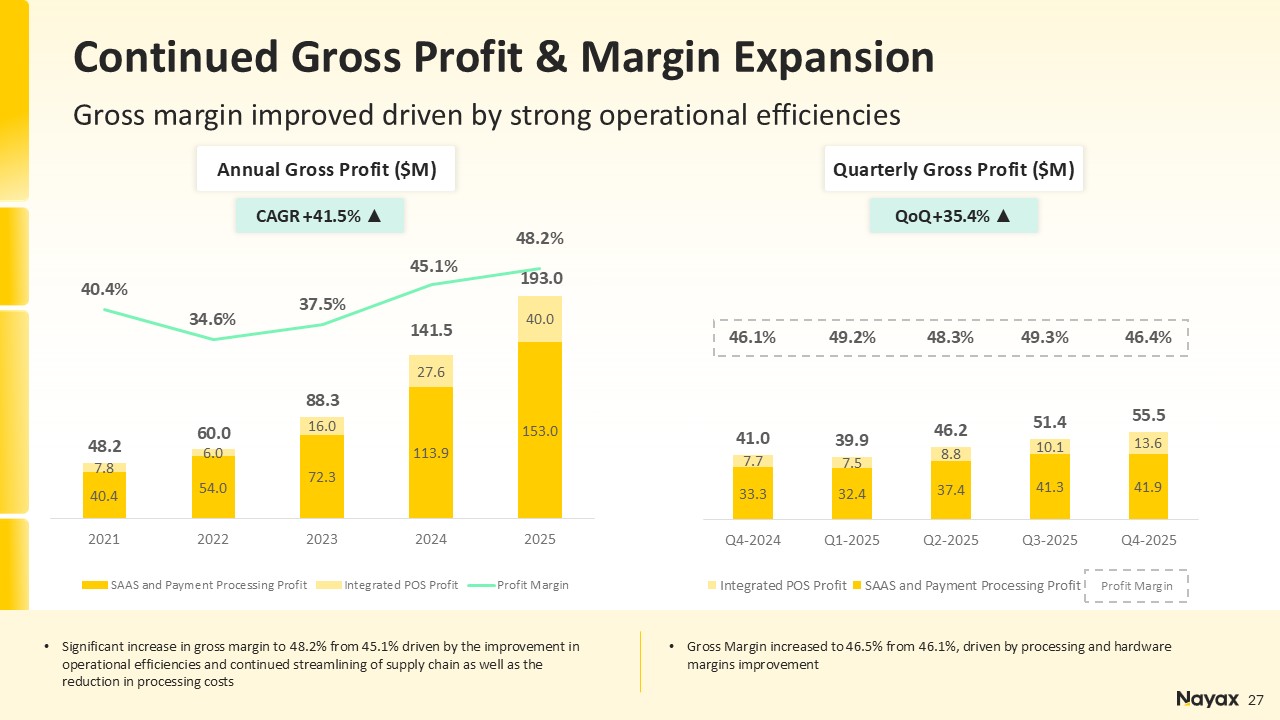

CAGR +41.5% ▲ 27 Annual Gross Profit ($M) Quarterly Gross Profit ($M) QoQ

+35.4% ▲ Significant increase in gross margin to 48.2% from 45.1% driven by the improvement in operational efficiencies and continued streamlining of supply chain as well as the reduction in processing costs Gross Margin increased to 46.5%

from 46.1%, driven by processing and hardware margins improvement Continued Gross Profit & Margin Expansion Gross margin improved driven by strong operational efficiencies Profit Margin

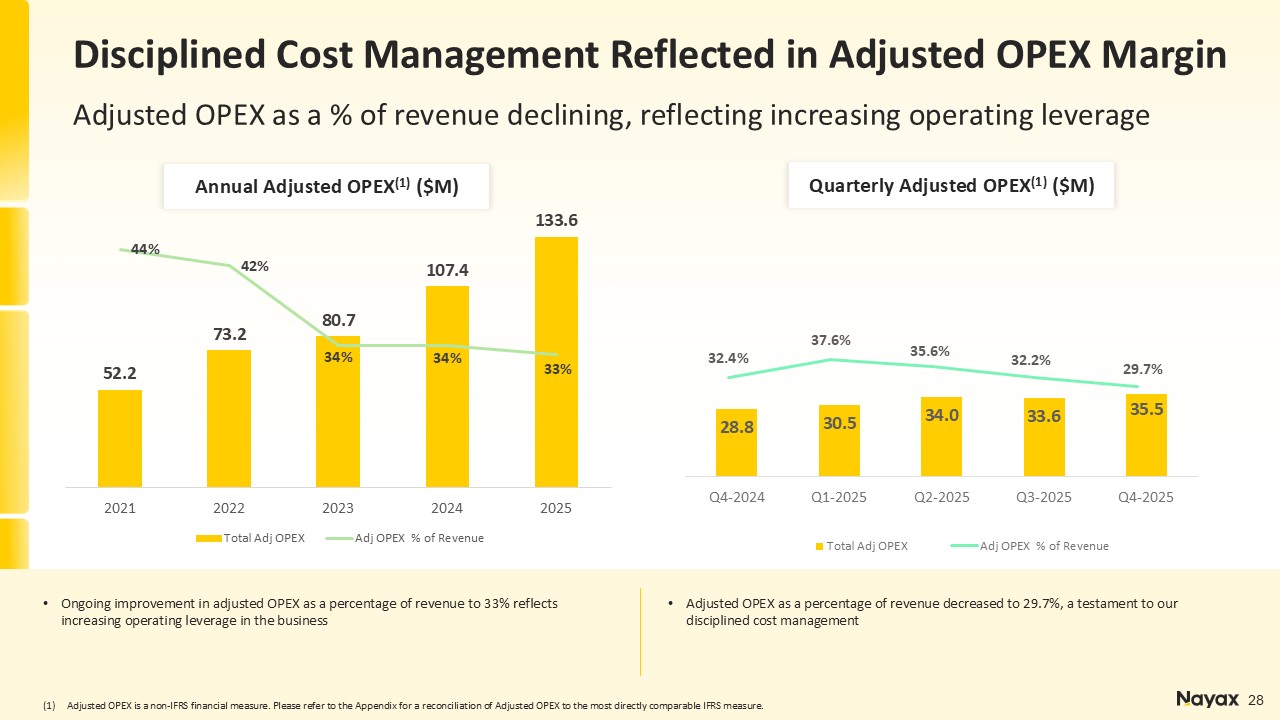

28 Annual Adjusted OPEX(1) ($M) Quarterly Adjusted OPEX(1) ($M) Ongoing

improvement in adjusted OPEX as a percentage of revenue to 33% reflects increasing operating leverage in the business Adjusted OPEX as a percentage of revenue decreased to 29.7%, a testament to our disciplined cost management Adjusted OPEX

is a non-IFRS financial measure. Please refer to the Appendix for a reconciliation of Adjusted OPEX to the most directly comparable IFRS measure. Disciplined Cost Management Reflected in Adjusted OPEX Margin Adjusted OPEX as a % of revenue

declining, reflecting increasing operating leverage

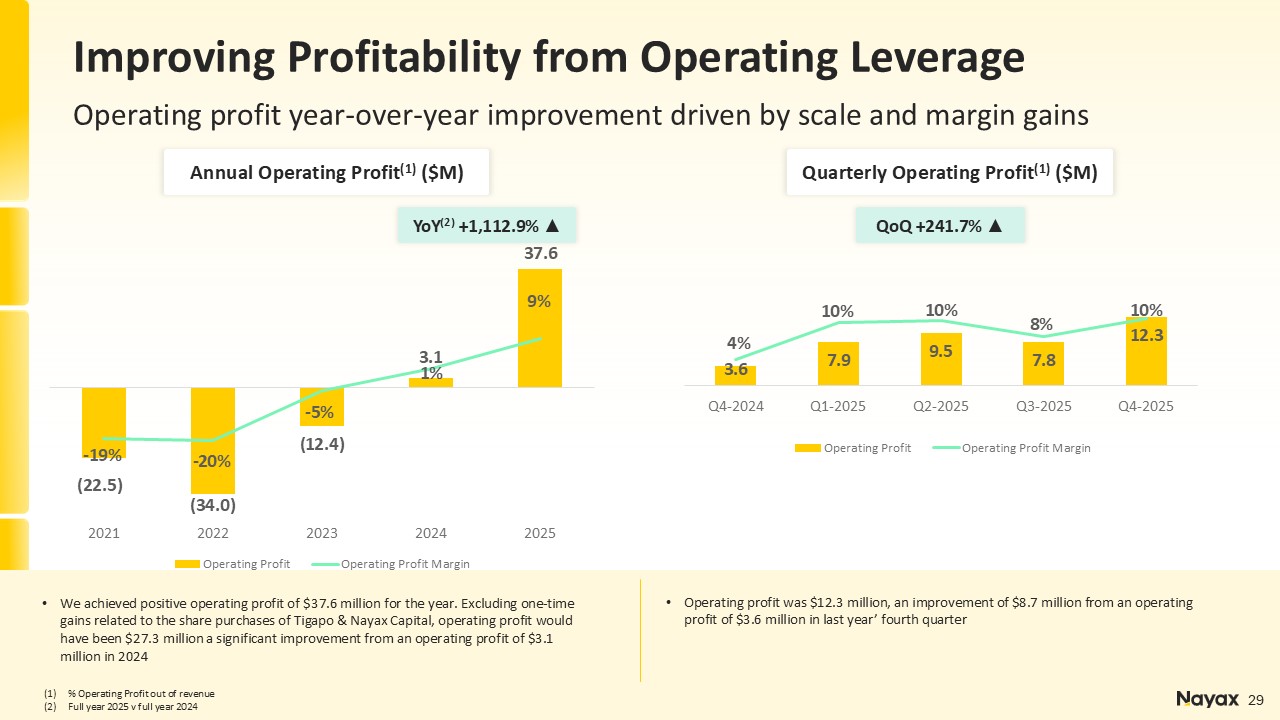

YoY(2) +1,112.9% ▲ 29 Annual Operating Profit(1) ($M) Quarterly Operating

Profit(1) ($M) QoQ +241.7% ▲ % Operating Profit out of revenue Full year 2025 v full year 2024 We achieved positive operating profit of $37.6 million for the year. Excluding one-time gains related to the share purchases of Tigapo &

Nayax Capital, operating profit would have been $27.3 million a significant improvement from an operating profit of $3.1 million in 2024 Operating profit was $12.3 million, an improvement of $8.7 million from an operating profit of $3.6

million in last year’ fourth quarter Improving Profitability from Operating Leverage Operating profit year-over-year improvement driven by scale and margin gains

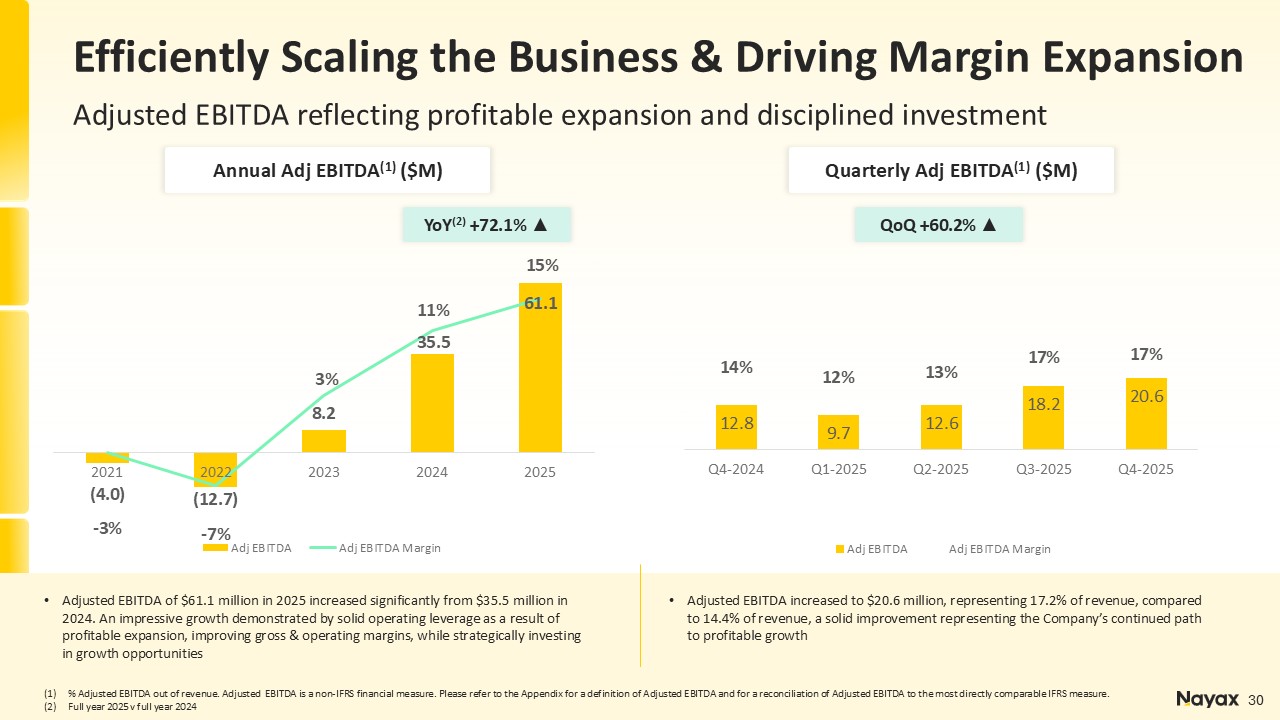

YoY(2) +72.1% ▲ 30 Annual Adj EBITDA(1) ($M) Quarterly Adj EBITDA(1) ($M) QoQ

+60.2% ▲ % Adjusted EBITDA out of revenue. Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS

measure. Full year 2025 v full year 2024 Adjusted EBITDA of $61.1 million in 2025 increased significantly from $35.5 million in 2024. An impressive growth demonstrated by solid operating leverage as a result of profitable expansion,

improving gross & operating margins, while strategically investing in growth opportunities Adjusted EBITDA increased to $20.6 million, representing 17.2% of revenue, compared to 14.4% of revenue, a solid improvement representing the

Company’s continued path to profitable growth Efficiently Scaling the Business & Driving Margin Expansion Adjusted EBITDA reflecting profitable expansion and disciplined investment

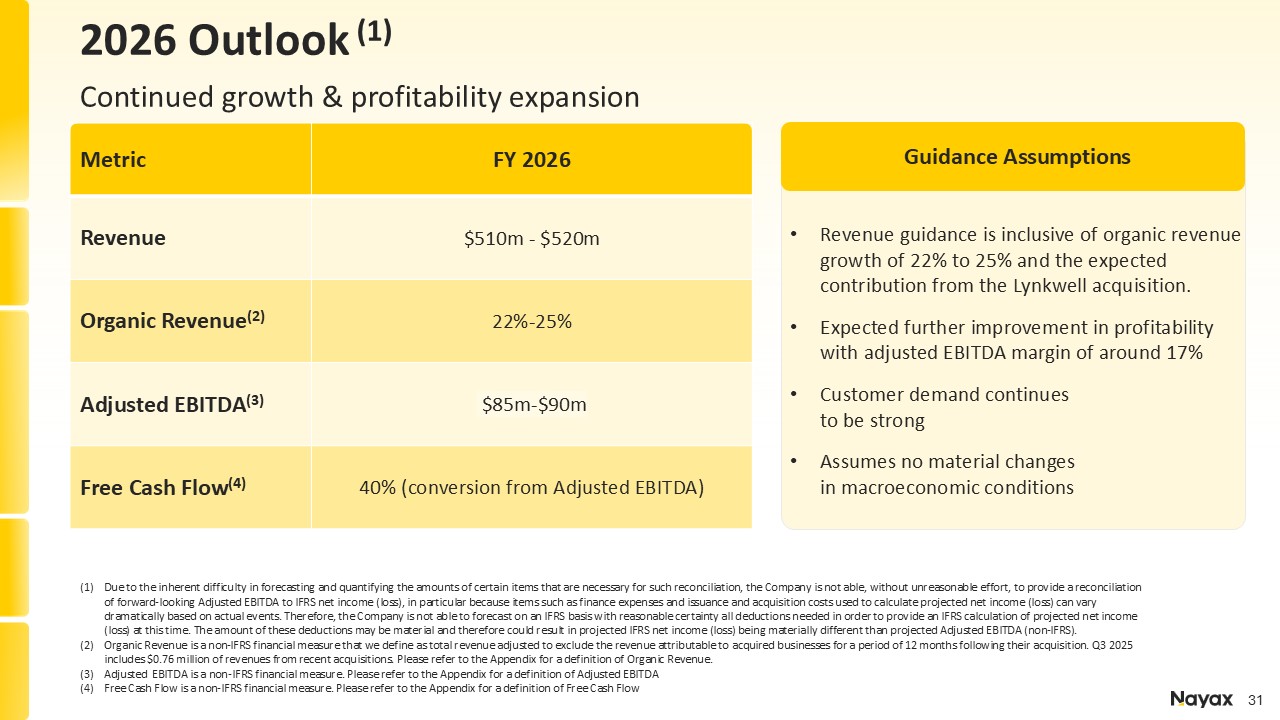

Metric FY 2026 Revenue $510m - $520m Organic Revenue(2) 22%-25% Adjusted

EBITDA(3) $85m-$90m Free Cash Flow(4) 40% (conversion from Adjusted EBITDA) Due to the inherent difficulty in forecasting and quantifying the amounts of certain items that are necessary for such reconciliation, the Company is not able,

without unreasonable effort, to provide a reconciliation of forward-looking Adjusted EBITDA to IFRS net income (loss), in particular because items such as finance expenses and issuance and acquisition costs used to calculate projected net

income (loss) can vary dramatically based on actual events. Therefore, the Company is not able to forecast on an IFRS basis with reasonable certainty all deductions needed in order to provide an IFRS calculation of projected net income (loss)

at this time. The amount of these deductions may be material and therefore could result in projected IFRS net income (loss) being materially different than projected Adjusted EBITDA (non-IFRS). Organic Revenue is a non-IFRS financial measure

that we define as total revenue adjusted to exclude the revenue attributable to acquired businesses for a period of 12 months following their acquisition. Q3 2025 includes $0.76 million of revenues from recent acquisitions. Please refer to the

Appendix for a definition of Organic Revenue. Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA Free Cash Flow is a non-IFRS financial measure. Please refer to the Appendix for

a definition of Free Cash Flow 2026 Outlook (1) Continued growth & profitability expansion Guidance Assumptions Revenue guidance is inclusive of organic revenue growth of 22% to 25% and the expected contribution from the Lynkwell

acquisition. Expected further improvement in profitability with adjusted EBITDA margin of around 17% Customer demand continues to be strong Assumes no material changes in macroeconomic conditions

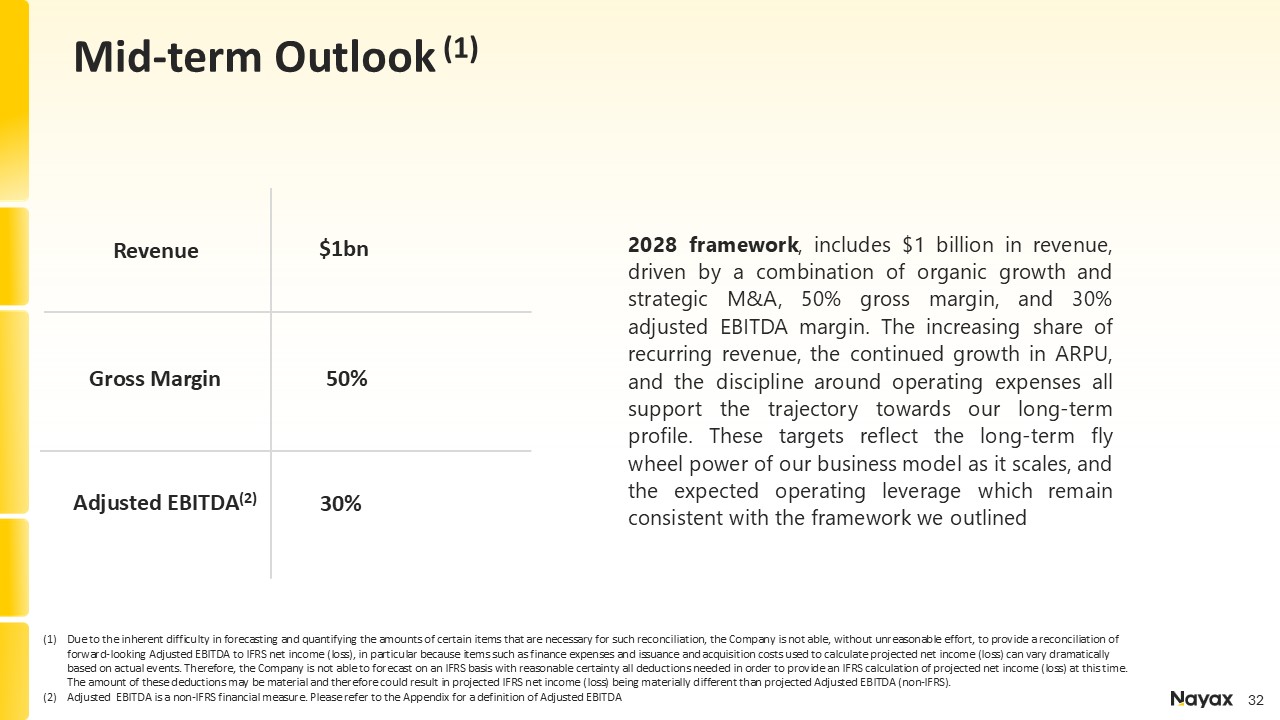

Mid-term Outlook (1) Revenue $1bn Gross Margin 50% Adjusted

EBITDA(2) 30% 2028 framework, includes $1 billion in revenue, driven by a combination of organic growth and strategic M&A, 50% gross margin, and 30% adjusted EBITDA margin. The increasing share of recurring revenue, the continued growth

in ARPU, and the discipline around operating expenses all support the trajectory towards our long-term profile. These targets reflect the long-term fly wheel power of our business model as it scales, and the expected operating leverage which

remain consistent with the framework we outlined Due to the inherent difficulty in forecasting and quantifying the amounts of certain items that are necessary for such reconciliation, the Company is not able, without unreasonable effort, to

provide a reconciliation of forward-looking Adjusted EBITDA to IFRS net income (loss), in particular because items such as finance expenses and issuance and acquisition costs used to calculate projected net income (loss) can vary dramatically

based on actual events. Therefore, the Company is not able to forecast on an IFRS basis with reasonable certainty all deductions needed in order to provide an IFRS calculation of projected net income (loss) at this time. The amount of these

deductions may be material and therefore could result in projected IFRS net income (loss) being materially different than projected Adjusted EBITDA (non-IFRS). Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for

a definition of Adjusted EBITDA

Appendix 33

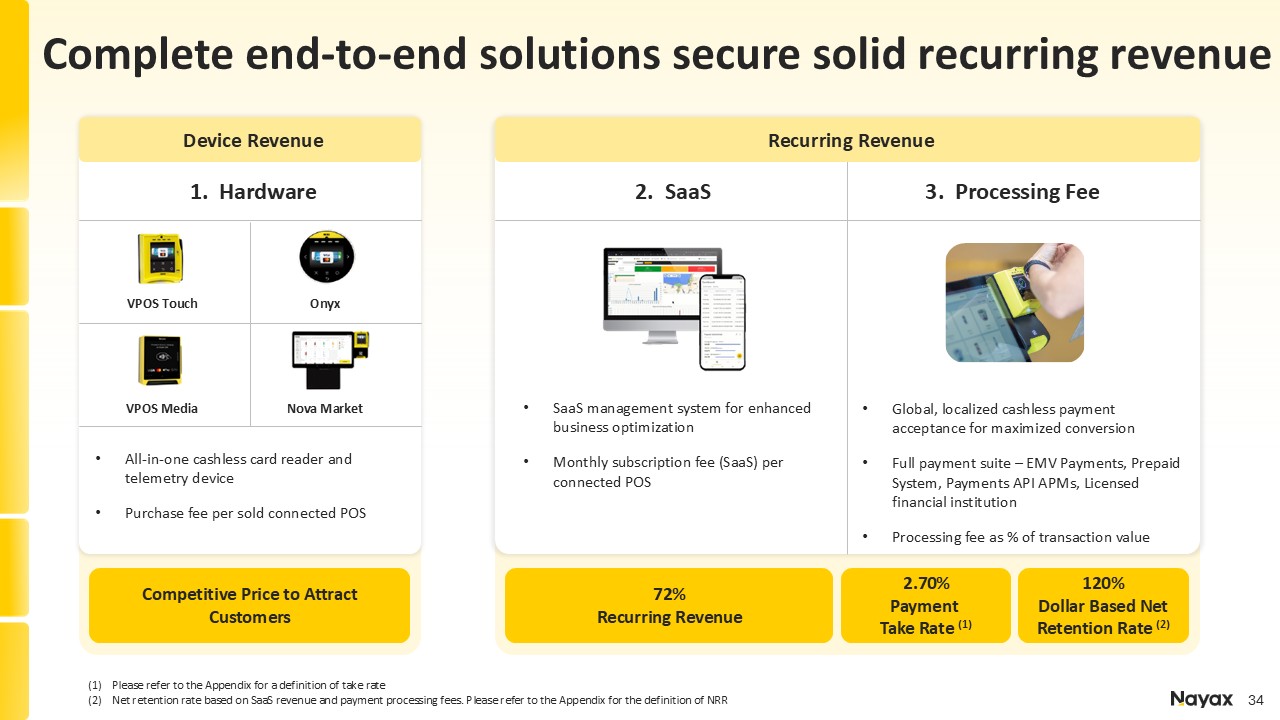

Device Revenue VPOS Touch All-in-one cashless card reader and telemetry

device Purchase fee per sold connected POS Onyx VPOS Media Nova Market Competitive Price to Attract Customers 1. Hardware 2. SaaS 3. Processing Fee 72% Recurring Revenue 2.70% Payment Take Rate (1) 120% Dollar Based Net

Retention Rate (2) SaaS management system for enhanced business optimization Monthly subscription fee (SaaS) per connected POS Global, localized cashless payment acceptance for maximized conversion Full payment suite – EMV Payments,

Prepaid System, Payments API APMs, Licensed financial institution Processing fee as % of transaction value Please refer to the Appendix for a definition of take rate Net retention rate based on SaaS revenue and payment processing fees.

Please refer to the Appendix for the definition of NRR Recurring Revenue Complete end-to-end solutions secure solid recurring revenue

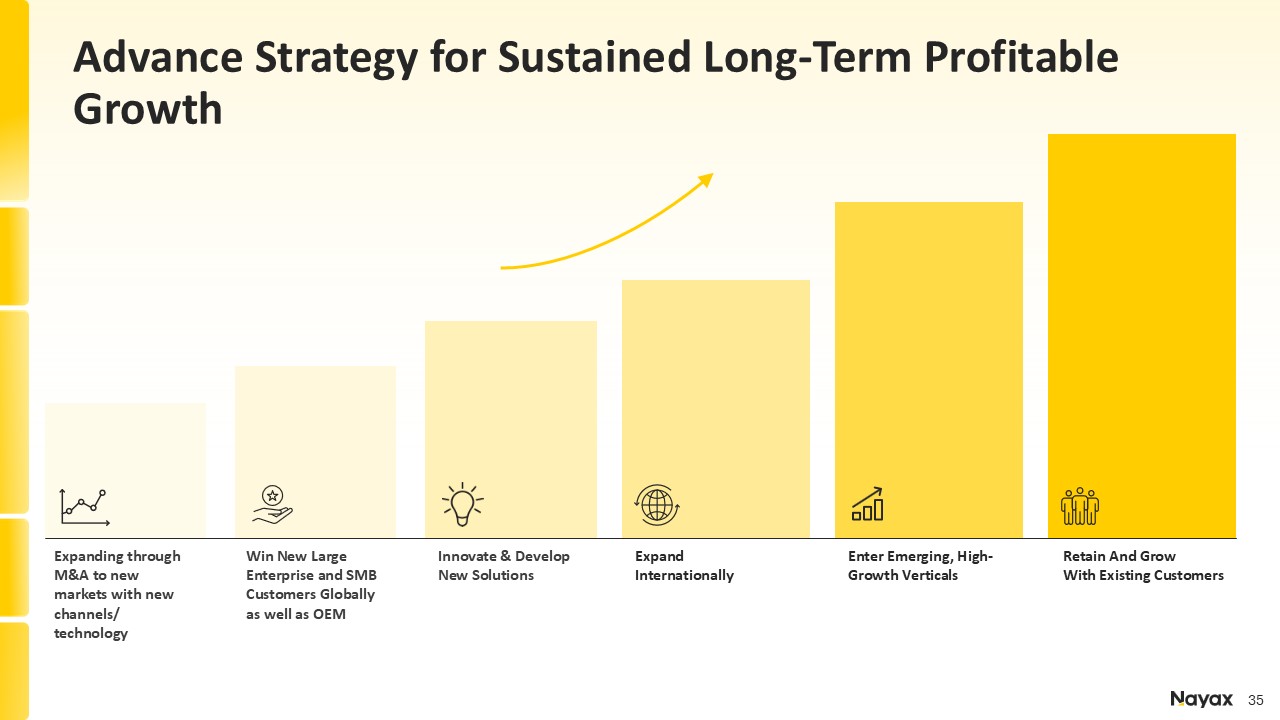

Expand Internationally Enter Emerging, High-Growth Verticals Retain And Grow

With Existing Customers Innovate & Develop New Solutions Win New Large Enterprise and SMB Customers Globally as well as OEM Expanding through M&A to new markets with new channels/ technology Advance Strategy for Sustained

Long-Term Profitable Growth

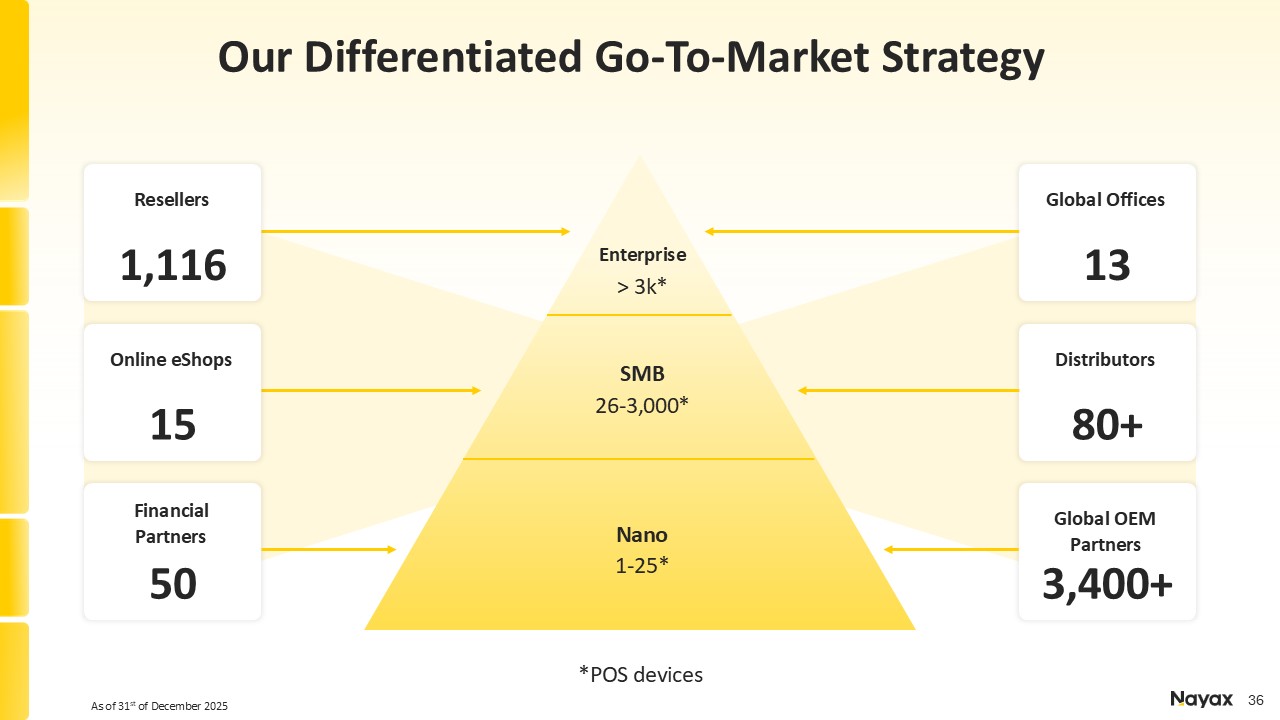

Global Offices 13 *POS devices Distributors 80+ Global OEM

Partners 3,400+ Resellers 1,116 Online eShops 15 Financial Partners 50 Nano 1-25* SMB 26-3,000* Enterprise > 3k* As of 31st of December 2025 Our Differentiated Go-To-Market Strategy

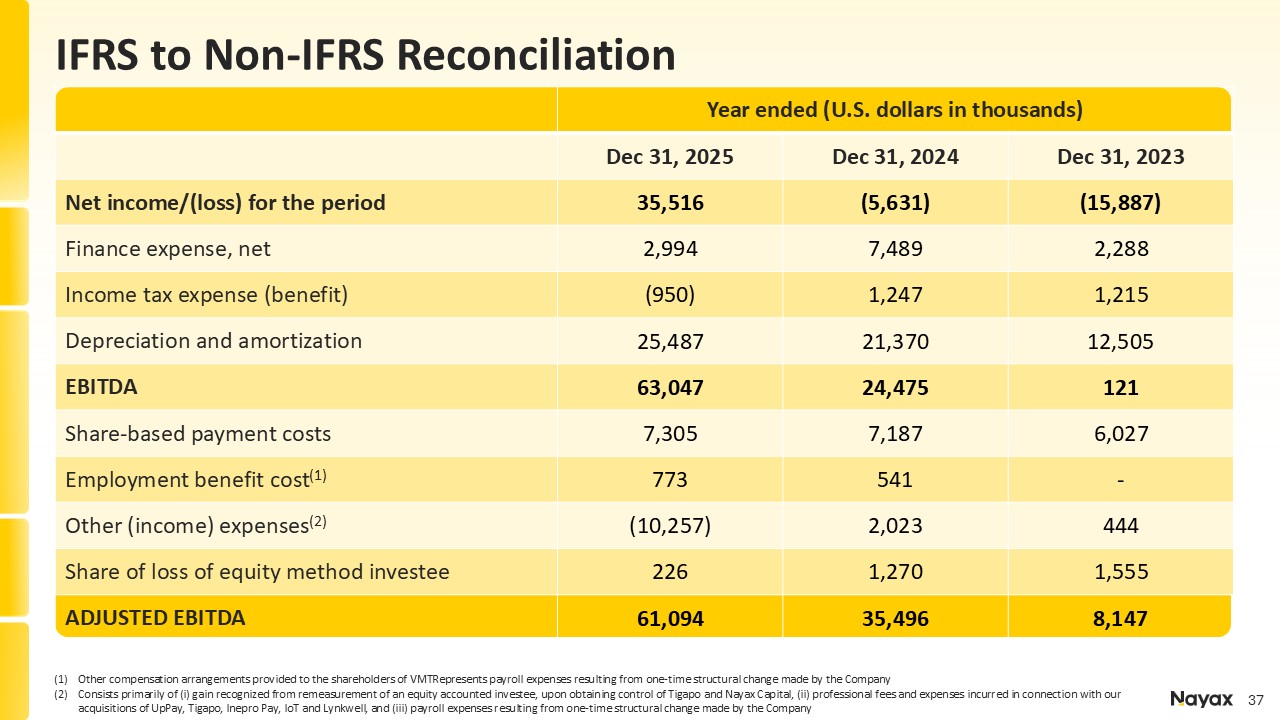

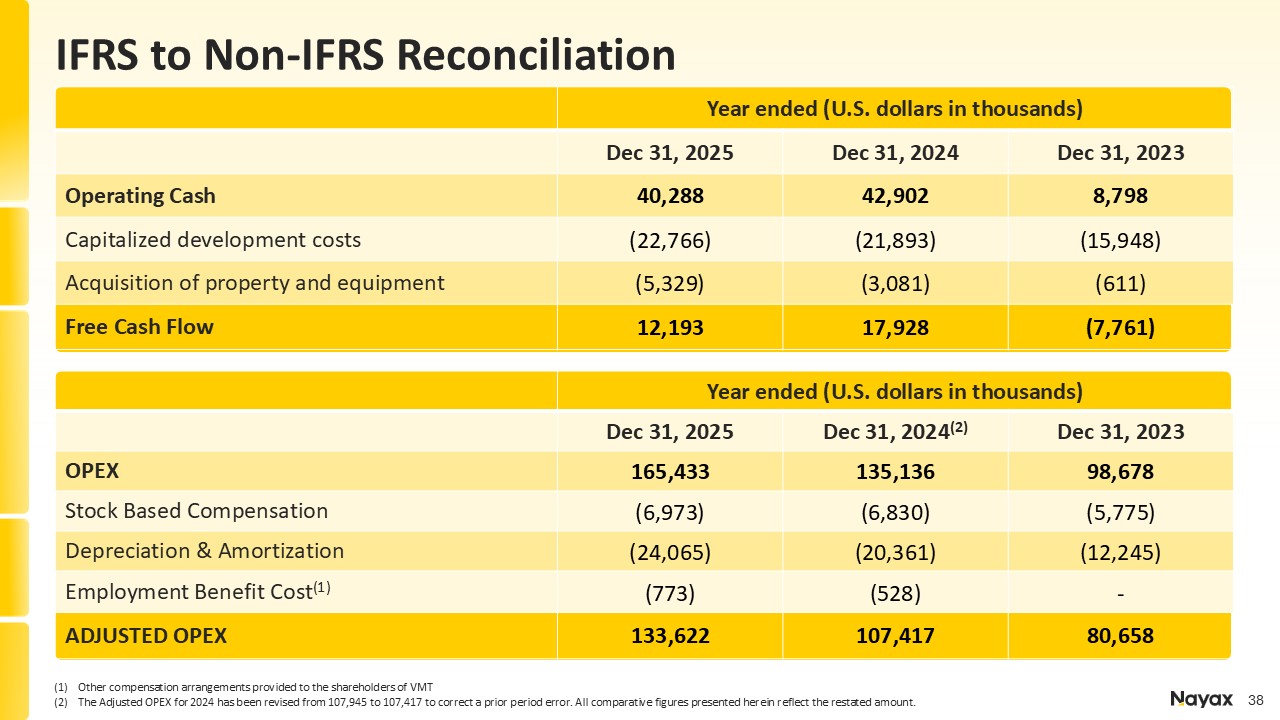

IFRS to Non-IFRS Reconciliation Other compensation arrangements provided to the

shareholders of VMTRepresents payroll expenses resulting from one-time structural change made by the Company Consists primarily of (i) gain recognized from remeasurement of an equity accounted investee, upon obtaining control of Tigapo and

Nayax Capital, (ii) professional fees and expenses incurred in connection with our acquisitions of UpPay, Tigapo, Inepro Pay, IoT and Lynkwell, and (iii) payroll expenses resulting from one-time structural change made by the Company Year ended

(U.S. dollars in thousands) Dec 31, 2025 Dec 31, 2024 Dec 31, 2023 Net income/(loss) for the period 35,516 (5,631) (15,887) Finance expense, net 2,994 7,489 2,288 Income tax expense (benefit) (950) 1,247 1,215 Depreciation and

amortization 25,487 21,370 12,505 EBITDA 63,047 24,475 121 Share-based payment costs 7,305 7,187 6,027 Employment benefit cost(1) 773 541 - Other (income) expenses(2) (10,257) 2,023 444 Share of loss of equity method

investee 226 1,270 1,555 ADJUSTED EBITDA 61,094 35,496 8,147

Year ended (U.S. dollars in thousands) Dec 31, 2025 Dec 31, 2024(2) Dec 31,

2023 OPEX 165,433 135,136 98,678 Stock Based Compensation (6,973) (6,830) (5,775) Depreciation & Amortization (24,065) (20,361) (12,245) Employment Benefit Cost(1) (773) (528) - ADJUSTED OPEX 133,622 107,417 80,658 IFRS

to Non-IFRS Reconciliation Year ended (U.S. dollars in thousands) Dec 31, 2025 Dec 31, 2024 Dec 31, 2023 Operating Cash 40,288 42,902 8,798 Capitalized development costs (22,766) (21,893) (15,948) Acquisition of property and

equipment (5,329) (3,081) (611) Free Cash Flow 12,193 17,928 (7,761) Other compensation arrangements provided to the shareholders of VMT The Adjusted OPEX for 2024 has been revised from 107,945 to 107,417 to correct a prior period

error. All comparative figures presented herein reflect the restated amount.

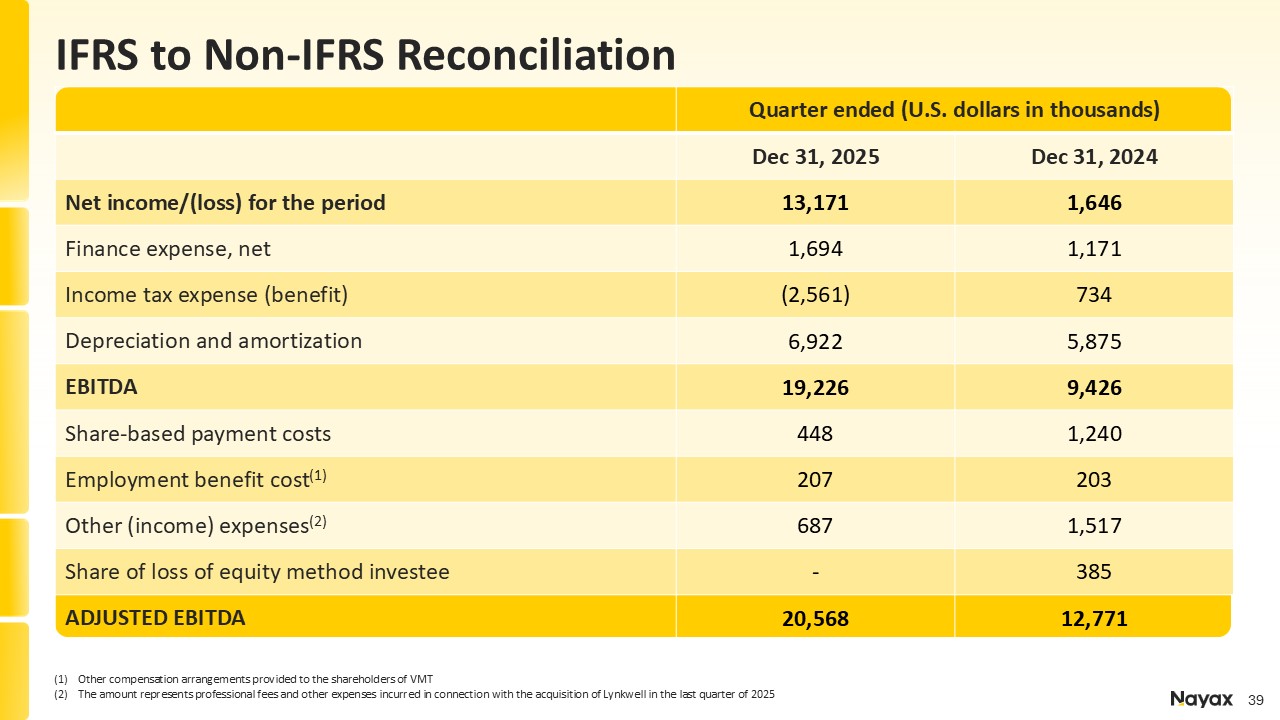

IFRS to Non-IFRS Reconciliation Other compensation arrangements provided to the

shareholders of VMT The amount represents professional fees and other expenses incurred in connection with the acquisition of Lynkwell in the last quarter of 2025 Quarter ended (U.S. dollars in thousands) Dec 31, 2025 Dec 31, 2024 Net

income/(loss) for the period 13,171 1,646 Finance expense, net 1,694 1,171 Income tax expense (benefit) (2,561) 734 Depreciation and amortization 6,922 5,875 EBITDA 19,226 9,426 Share-based payment costs 448 1,240 Employment

benefit cost(1) 207 203 Other (income) expenses(2) 687 1,517 Share of loss of equity method investee - 385 ADJUSTED EBITDA 20,568 12,771

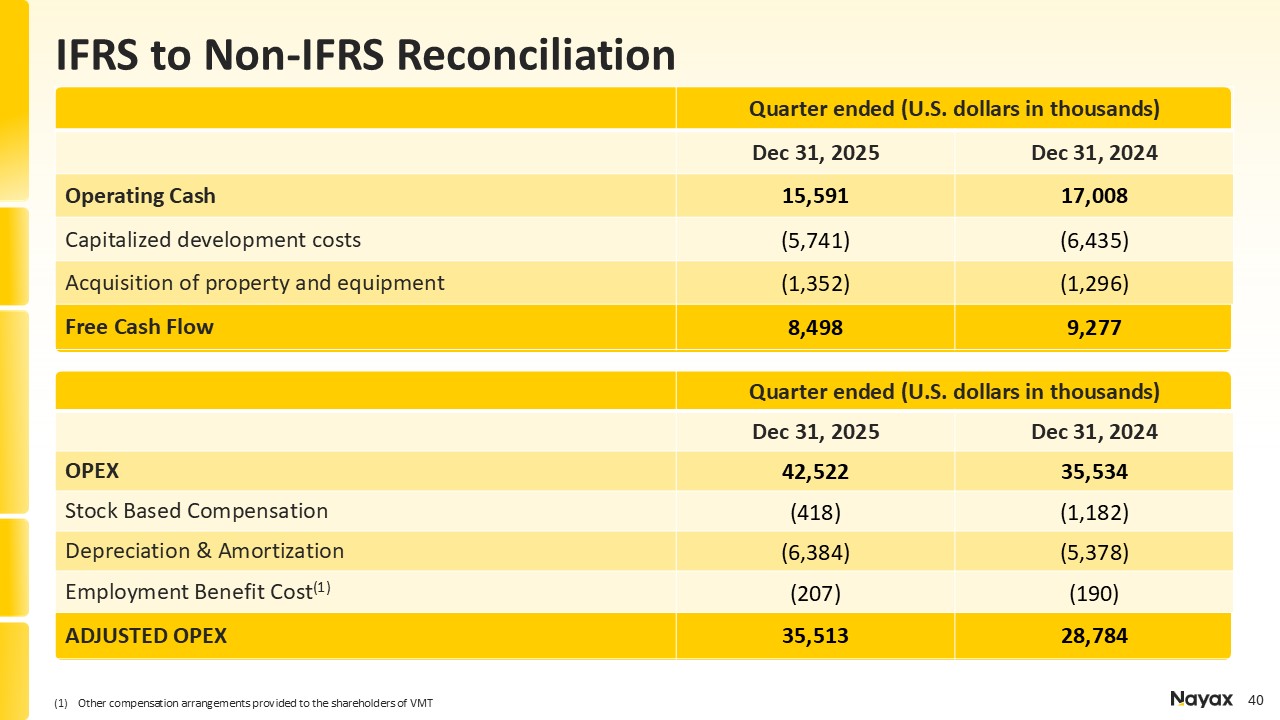

Quarter ended (U.S. dollars in thousands) Dec 31, 2025 Dec 31,

2024 OPEX 42,522 35,534 Stock Based Compensation (418) (1,182) Depreciation & Amortization (6,384) (5,378) Employment Benefit Cost(1) (207) (190) ADJUSTED OPEX 35,513 28,784 IFRS to Non-IFRS Reconciliation Quarter ended

(U.S. dollars in thousands) Dec 31, 2025 Dec 31, 2024 Operating Cash 15,591 17,008 Capitalized development costs (5,741) (6,435) Acquisition of property and equipment (1,352) (1,296) Free Cash Flow 8,498 9,277 Other compensation

arrangements provided to the shareholders of VMT

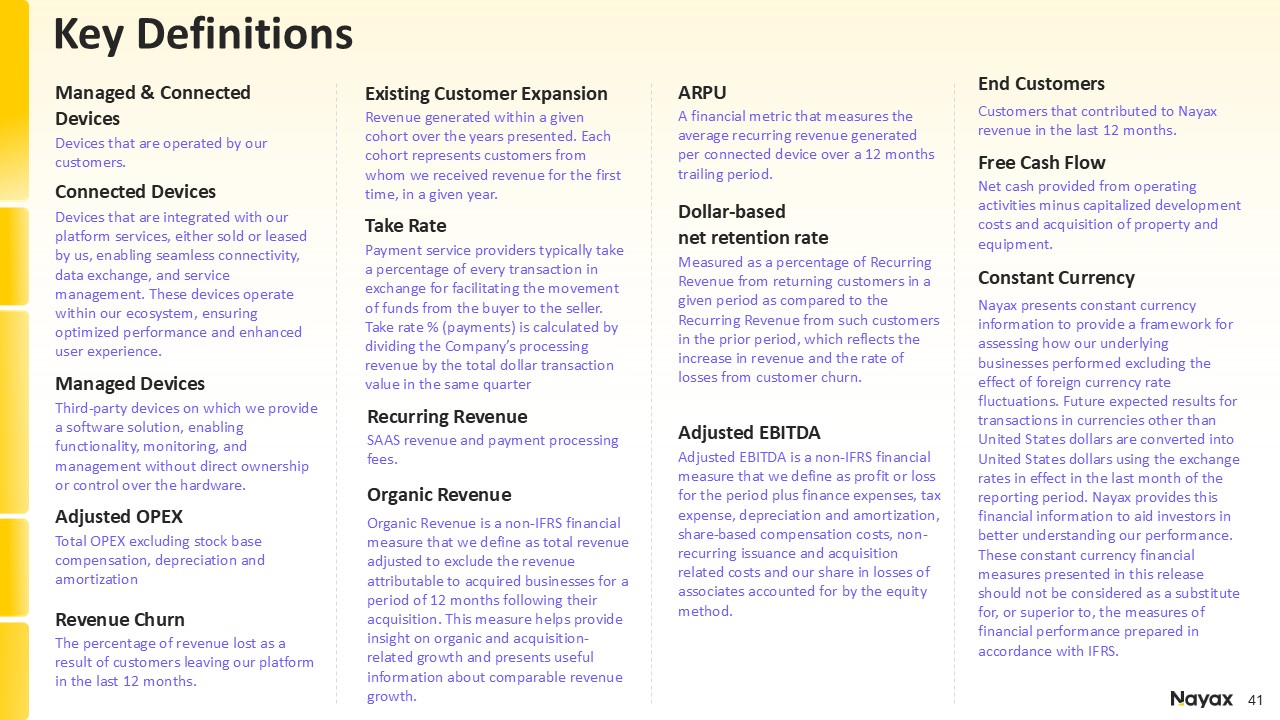

Key Definitions Measured as a percentage of Recurring Revenue from returning

customers in a given period as compared to the Recurring Revenue from such customers in the prior period, which reflects the increase in revenue and the rate of losses from customer churn. Dollar-based net retention rate Nayax presents

constant currency information to provide a framework for assessing how our underlying businesses performed excluding the effect of foreign currency rate fluctuations. Future expected results for transactions in currencies other than United

States dollars are converted into United States dollars using the exchange rates in effect in the last month of the reporting period. Nayax provides this financial information to aid investors in better understanding our performance. These

constant currency financial measures presented in this release should not be considered as a substitute for, or superior to, the measures of financial performance prepared in accordance with IFRS. Constant Currency Adjusted EBITDA is a

non-IFRS financial measure that we define as profit or loss for the period plus finance expenses, tax expense, depreciation and amortization, share-based compensation costs, non-recurring issuance and acquisition related costs and our share in

losses of associates accounted for by the equity method. Adjusted EBITDA Devices that are integrated with our platform services, either sold or leased by us, enabling seamless connectivity, data exchange, and service management. These devices

operate within our ecosystem, ensuring optimized performance and enhanced user experience. Connected Devices Devices that are operated by our customers. Managed & Connected Devices Customers that contributed to Nayax revenue in the

last 12 months. End Customers SAAS revenue and payment processing fees. Recurring Revenue The percentage of revenue lost as a result of customers leaving our platform in the last 12 months. Revenue Churn Revenue generated within a given

cohort over the years presented. Each cohort represents customers from whom we received revenue for the first time, in a given year. Existing Customer Expansion Net cash provided from operating activities minus capitalized development costs

and acquisition of property and equipment. Free Cash Flow Third-party devices on which we provide a software solution, enabling functionality, monitoring, and management without direct ownership or control over the hardware. Managed

Devices Total OPEX excluding stock base compensation, depreciation and amortization Adjusted OPEX Payment service providers typically take a percentage of every transaction in exchange for facilitating the movement of funds from the buyer

to the seller. Take rate % (payments) is calculated by dividing the Company’s processing revenue by the total dollar transaction value in the same quarter Take Rate A financial metric that measures the average recurring revenue generated per

connected device over a 12 months trailing period. ARPU Organic Revenue is a non-IFRS financial measure that we define as total revenue adjusted to exclude the revenue attributable to acquired businesses for a period of 12 months following

their acquisition. This measure helps provide insight on organic and acquisition-related growth and presents useful information about comparable revenue growth. Organic Revenue

Aaron Greenberg Chief Strategy Officer ir@nayax.com IR Contact Thank

You! ir.nayax.com Website