Enlight Renewable Energy Ltd.

Monitoring and Rating Action Report | May 2026

This credit rating report is a translation of

a report that was written in Hebrew for a debt issued in Israel.

The binding version is the one in the original language.

Contacts:

Robert Avdalimov

Senior Analyst, Lead Rating Analyst

robert.a@midroog.co.il

Alon Cohen

Analyst, Secondary Rating Analyst

alon.c@midroog.co.il

Iris Sde Or, Vice President

Head of Projects and Infrastructure

iris.s@midroog.co.il

| MIDROOG |

Enlight Renewable Energy Ltd.

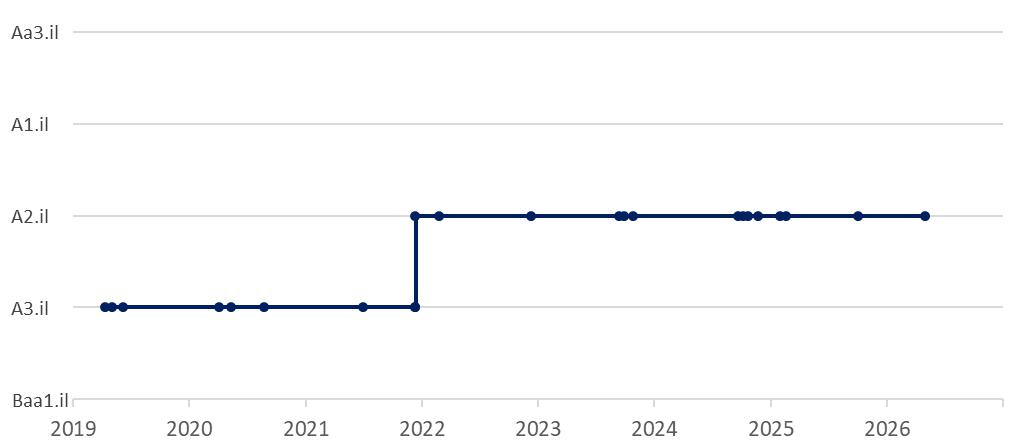

| Issuer Rating | A2.il | Outlook: Positive |

| Series Rating | A2.il | Outlook: Positive |

Midroog assigns an A2.il rating to debentures series 7, which is expected to be issued by Enlight Renewable Energy Ltd. (the "Company"), in an amount of up to 550 million par value, and changes the rating outlook from stable to positive. The proceeds from the issuance are expected to be used for refinancing existing debt and Company’s ongoing business operations. The rating also applies to the Company’s outstanding bonds (Series 3-4, 6-8).

Outstanding bonds rated by Midroog:

| Bond series | Security No. | Rating | Outlook | Final Maturity |

| ENLIGHT C3 | 7200249 | A2.il | Positive | 01.09.2028 |

| ENLIGHT B4 | 7200256 | A2.il | Positive | 01.09.2029 |

| ENLIGHT B6 | 7200173 | A2.il | Positive | 01.09.2026 |

| ENLIGHT B7 | 1218122 | A2.il | Positive | 01.09.2033 |

| ENLIGHT C8 | 1218130 | A2.il | Positive | 01.09.2033 |

Summary of Rating Rationale

The rating takes into account the following considerations, among others: (1) The Company operates in the sector of electricity generation from renewable energies, in Israel and around the world, which is assessed by Midroog at medium risk; (2) The Company's activity in the different countries is mostly conducted under tariff arrangements in a supportive regulatory environment and/or under long-term PPA1 agreements for the sale of electricity, mainly with giant corporations and local grid operators. In the framework of its electricity storage activity in the US, the Company provides local system operators with grid services, according to an income model based on availability payments that are not affected by demand. In our assessment, these characteristics contribute to stability of the Company's cash flow and strengthen cash flow certainty over the long term; (3) Lower entry barriers to the renewable energy power generation market than to the power generation market based on fossil fuel plants, which is characterized by high entry barriers due, among other things, to the need for significant capital investments coupled with technological and engineering complexity. At the same time, the Company has focused in recent years on the initiation and construction of high-capacity renewable energy projects, on a scale which, in our opinion, requires expertise, experience and execution capabilities not generally possessed by players in the market; (4) The growth trend characterizing the renewable energy sector in Israel and worldwide, supported by government decisions for setting renewable energy promotion targets; (5) A substantial increase in the installed capacity and geographical diversification of the income-generating projects. This trend is expected to persist in the coming years, with the entry into commercial operation of additional projects in the US, Europe and Israel; (6) Improvement in the Company's geographical diversification and revenue concentration, with further improvement expected as additional projects enter commercial operation; (7) The Company's strategy to create a broad and diversified geographical mix, which includes the sale of electricity in developed markets, alongside operations in developing countries with varying regulatory regimes; (8) The Company has a significant investment plan that includes the construction and development of several projects in the US, Europe and Israel. This plan has resulted in a substantial increase in Capex expenses in recent years, with these expenses2 amounting to $1.8 billion in 2025, compared to $0.9 billion in 2024, in a growth trend expected to persist in the coming years; (9) A project finance structure based on non-recourse debt of the subsidiaries. Accordingly, the Company's coverage ratios are relatively long and characterized by a high leverage ratio, as customary in the sector, as against assets with long-term cash flows that align with the project debt duration; (10) The revenue-generating ability of the Company is assessed to be good, given the stability, profitability and financial strength of the projects held by the Company, with EBITDA as of the end of 2025 totaling $284 million, compared to $247 million3 for the year-before period; (11) Exposure to interest rates, exchange rates and the credit risks of the various countries in which the Company operates. It should be noted that approximately 88% of the Company's existing debt (at project and Company level) is not exposed to interest-rate fluctuations; (12) The gross financial debt to capital resources (Cap) ratio stood at 71.1% at the end of 2025. The share offering held in the first quarter of 2026 bolstered the Company's financial strength; (13) The debt to EBITDA ratio stood at 18.0 in 2025, and should improve somewhat in 2026-2027, in view of substantial cash flows from new projects that are set to begin commercial operation. (14) Good financial flexibility and high liquidity reserves, which stood at $979 million as of March 31, 2026; (15) In our assessment, renewable energy power generation projects have low exposure to environmental and social risks, in light of supportive regulation and demand trends. We likewise rate the Company's exposure to governance risk as low.

Under Midroog's base case scenario, EBITDA is expected to be in the range of $400-450 million in 2026, and to increase significantly during 2027-2028, to a range of $550-600 million in 2027 and $750-800 million in 2028, following the entry into commercial operation of several projects, mainly in the US. The debt to EBITDA ratio is expected to stand at 16.0 in 2026, with this ratio projected to improve in 2027 to a range of 11.5-12.5. Meanwhile, the interest coverage ratio of EBIT to finance costs is expected to stand in the range of 1.4-2.0 in those years. Additionally, the gross financial debt to capital resources (Cap) ratio is expected to be in the range of 68%-72% in the years 2026-2028.

1 Power Purchase Agreements.

2 Including adjustment in respect of lease liability principal payment.

3 Excluding revenues from tax partners, other income and expenses, and income from the sale of assets.

2

| MIDROOG |

Additional Rating Considerations

(1) The Company’s undertaking to maintain liquidity reserves and/or available unused credit facilities in a minimum amount of approximately NIS 100 million, at the very least, in excess of bond repayment needs for the following 9 months; (2) Structural and cash flow subordination of the Company to senior and subordinated debts of the projects owned by it, moderated by high-quality projects with wide geographical diversification; (3) Ownership without a control core, allowing for an appropriate balance between debtholders and shareholders and significant capital raises, as necessary, with no dividend distribution expected in periods of significant investments.

Rating Outlook

The positive rating outlook is supported by the strengthening of the Company’s capital base and the expected commercial operation of material projects in the U.S. in the short-to-medium term, alongside the Company’s strong business position, high cash flow certainty, and financial flexibility.

Operation Lion's Roar, which began on February 26, 2026, has led to a series of repercussions and restrictions, including, among others, the partial or full closure of businesses, suspension of civilian flights, restrictions on gatherings at workplaces and educational institutions, as well as the call-up of reserves. These measures have resulted in a reduction in economic activity and other negative effects on the Israeli economy. In Midroog's assessment, this period is characterized by a high degree of uncertainty as to how the war will unfold and as to its economic ramifications. Accordingly, Midroog may update the base case scenario for the rating in light of future developments.

Factors that could lead to a rating upgrade

| · | Substantial improvement in leverage ratios, cash flow and coverage ratios, and demonstration of stability over time. |

| · | Significant improvement in the Company's overall capacity, revenues, and cash flow diversification. |

3

| MIDROOG |

Factors that could lead to a rating downgrade

| · | A change in the sector risk profile, including deterioration in the supportive regulatory environment. |

| · | Significant worsening of leverage ratios, financial strength and debt service coverage ratios. |

| · | Material deviations from the timetable and budget framework established for the development of the projects under construction. |

Enlight Renewable Energy Ltd. – Key Financial Indicators ($ in millions)

| 31.03.2026 | 31.03.2025 | 31.12.2025 | 31.12.2024 | 31.12.2023 | |

| Cash, cash equivalents and deposits | 979 | 450 | 528 | 387 | 409 |

| Equity | 2,437 | 1,591 | 1,995 | 1,441 | 1,436 |

| Gross financial debt4 | 5,512 | 3,420 | 5,100 | 3,093 | 2,721 |

| Total assets | 9,314 | 5,884 | 8,630 | 5,547 | 4,634 |

| Gross financial debt/cap | 68.6% | 63.3% | 71.1% | 67.6% | 64.9% |

| Adjusted EBITDA5 | 89 | 69 | 284 | 247 | 179 |

| Capex6 | 612 | 260 | 1,821 | 905 | 736 |

Rating Scorecard[1]

| As of 31.12.2025 | Midroog Forecast | ||||||

| Category | Parameters | Measurement | Score | Measurement | Score | ||

Operating environment |

Cash flow certainty | --- | A.il | --- | A.il | ||

| Entry barriers | --- | A.il | --- | A.il | |||

| Regulatory framework | --- | A.il-Aa.il | --- | A.il-Aa.il | |||

Business profile |

Total assets | $8,630M | Aaa.il | $11,000-12,000M | Aaa.il | ||

Quality of geographical diversification |

--- | Aa.il | --- | Aa.il | |||

| Quality and diversification of products and operating segments |

--- | A.il-Aa.il | --- | A.il-Aa.il | |||

| Capex/PPE | 27% | A.il | 13%-22% | A.il | |||

| Financial profile |

Debt/EBITDA | 18.0 | Ba.il | 11.5-16.0 | Baa.il | ||

| EBIT/Net finance costs | 1.1 | Baa.il | 1.4-2.0 | Baa.il | |||

| Debt/cap | 71.1% | Baa.il | 68%-72% | Baa.il | |||

| Financial policy | -- | A.il | -- | A.il | |||

| Implied score | A2.il | ||||||

| Final score | A2.il | ||||||

[1] The metrics shown in the table are after adjustments by Midroog and are not necessarily identical to those presented by the Company. The Midroog forecast includes Midroog's assessments with respect to the issuer according to its base case scenario, and not the issuer's assessments.

4 Including lease liabilities, liabilities measured through profit and loss, loans from non-controlling interests, and other long-term liabilities, excluding liabilities related to tax equity agreements, deferred revenus from tax equity partners, and debt service reverse funds.

5 Excluding other expenses and income, revenues from tax equity partners, and adjustments related to concession arrangements. EBITDA is calculated in accordance with Midroog’s financial adjustments.

6 Including adjustment in respect of lease liability principal payment.

4

| MIDROOG |

Rating History

Related Reports

Enlight Renewable Energy Ltd. – Related Reports

Rating Power Producers – Methodology Report, January 2023

Financial Statement Adjustments and Presentation of Main Financial Measures in Corporate Rating – Methodology Report, December 2024

Structural Considerations in Rating Debt Instruments in Corporate Finance – Methodology Report, September 2019

Guidelines for Reviewing Environmental, Social and Governance Risks in Credit Ratings – Methodology Report, February 2022

Midroog Rating Scales and Definitions

The reports are published on the Midroog website at www.midroog.co.il

General Information

Date of rating report:

Date of last revision of the rating:

Date of first publication of the rating:

Rating commissioned by:

Rating paid for by: |

October 16, 2025

Enlight Renewable Energy Ltd.

Enlight Renewable Energy Ltd. |

INFORMATION FROM THE ISSUER

Midroog relies in its ratings inter alia on information received from competent personnel at the issuer.

5

| MIDROOG |

Long-Term Rating Scale

| Aaa.il | Issuers or issues rated Aaa.il are those that, in Midroog judgment, have highest creditworthiness relative to other local issuers. |

| Aa.il | Issuers or issues rated Aa.il are those that, in Midroog judgment, have very strong creditworthiness relative to other local issuers. |

| A.il | Issuers or issues rated A.il are those that, in Midroog judgment, have relatively high creditworthiness relative to other local issuers. |

| Baa.il | Issuers or issues rated Baa.il are those that, in Midroog judgment, have relatively moderate credit risk relative to other local issuers, and could involve certain speculative characteristics. |

| Ba.il | Issuers or issues rated Ba.il are those that, in Midroog judgment, have relatively weak creditworthiness relative to other local issuers, and involve speculative characteristics. |

| B.il | Issuers or issues rated B.il are those that, in Midroog judgment, have relatively very weak creditworthiness relative to other local issuers, and involve significant speculative characteristics. |

| Caa.il | Issuers or issues rated Caa.il are those that, in Midroog judgment, have extremely weak creditworthiness relative to other local issuers, and involve very significant speculative characteristics. |

| Ca.il | Issuers or issues rated Ca.il are those that, in Midroog judgment, have extremely weak creditworthiness and very near default, with some prospect of recovery of principal and interest. |

| C.il | Issuers or issues rated C are those that, in Midroog judgment, have the weakest creditworthiness and are usually in a situation of default, with little prospect of recovery of principal and interest. |

Note: Midroog appends numeric modifiers 1, 2, and 3 to each rating category from Aa.il to Caa.il. The modifier '1' indicates that the obligation ranks in the higher end of its rating category, which is denoted by letters. The modifier '2' indicates that it ranks in the middle of its rating category and the modifier '3' indicates that the obligation ranks in the lower end of that category, denoted by letters.

6

| MIDROOG |

Copyright © All rights reserved to Midroog Ltd. (hereinafter: “Midroog”).

CREDIT RATINGS ISSUED BY MIDROOG ARE MIDROOG’S SUBJECTIVE OPINIONS ABOUT THE RELATIVE FUTURE CREDITWORTHINESSOF ENTITIES, CREDIT OBLIGATIONS, DEBTS AND/OR DEBT-LIKE FINANCIAL INSTRUMENTS, WHICH APPLY ON THE DATE OF THEIR PUBLICATION OR OTHER MEANS OF PROVISION, AND AS LONG AS MIDROOG HAS NOT CHANGED THE RATING OR WITHDRAWN IT AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED OR OTHERWISE MADE AVAILABLE BY MIDROOG (COLLECTVELY, “MATERIALS”) MAY INCLUDE SUCH OPINIONS. MIDROOG DEFINES CREDITWORTHINESS AS THE ISSUER’S ABILITY TO MEET ITS CONTRACTUAL OBLIGATIONS AND LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT . MIDROOG'S CREDIT RATINGS DO NOT ADDRESS ANY OTHER FACTOR, INCLUDING BUT NOT LIMITED TO RISKS RELATING TO LIQUIDITY, MARKET VALUE, CHANGE IN INTEREST RATES, PRICE VOLATILITY, OR ANY OTHER NON-CREDITWORTHINESS ELEMENT. CREDIT RATINGS, NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MIDROOG’S MATERIALS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MIDROOG’S MATERIALS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDITWORTHINESS, AS WELL AS RELATED OPINIONS OR COMMENTARY. MIDROOG’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND MATERIALS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MIDROOG’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND MATERIALS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MIDROOG’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND MATERIALS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MIDROOG ISSUES ITS CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES OR OTHERWISE PROVIDES ITS MATERIALS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE. EVERY INVESTOR SHOULD OBTAIN PROFESSIONAL ADVICE IN RESPECT TO THEIR INVESTMENTS, TO THE APPLICABLE LAW, AND/OR TO ANY OTHER PROFESSIONAL ISSUE.

MIDROOG’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND MATERIALS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS, AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MIDROOG’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR MATERIALS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW AND BY INTELLECTUAL PROPERTY LAW. NONE OF SUCH INFORMATION MAY BE COPIED, OR OTHERWISE SCANNED, AMENDED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED, DUPLICATED, DISPLAYED, TRANSLATED, RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON, WITHOUT ADVANCE WRITTEN CONSENT FROM MIDROOG.

Midroog makes use of rating scales to issue its opinions, according to definitions detailed in the scale itself. The choice of a symbol to reflect Midroog’s opinion with respect to creditworthiness reflects solely a relative assessment of such creditworthiness. Midroog’s credit ratings are not issued on a global scale – they are opinions of the creditworthiness of issuers and their financial obligations relative to that of other issuers and financial obligations within Israel.

MIDROOG CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND MATERIALS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY RATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MIDROOG IN ANY FORM OR MANNER WHATSOEVER.

All the information contained in Midroog Ratings, Assessments, other opinions and Materials (hereinafter: "the Information") is obtained by Midroog from sources believed by it to be accurate and credible. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. Midroog is not responsible for the accuracy of the Information. Midroog exercises reasonable means so that the information it uses in assigning a credit rating is of sufficient quality and that it originates from sources Midroog considers to be credible, including information received from independent third parties, if and when appropriate. However, Midroog is not an auditor and cannot in every instance independently verify or validate information received in the credit rating process or in preparing its Materials.

The provisions of any Midroog Materials other than one expressly stated as a methodology do not constitute part of any Midroog methodology.

To the extent permitted by law, Midroog and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if Midroog or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by Midroog.

To the extent permitted by law, Midroog and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, Midroog or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

Midroog maintains policies and procedures in respect to the independence of the rating and the rating processes.

A rating, assessment or opinion issued by Midroog may change as a result of changes in the information on which it was based and/or as a result of new information and/or for any other reason. When applicable, updates and/or changes in ratings are presented on Midroog’s website at www.midroog.co.il.

7