Please wait

Abilene DC 1, LLC

Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

Abilene DC 1, LLC

Abilene DC 1, LLCFinancial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

Contents:

Independent Auditors’ Report…………………………………………………....…..…… 1

Statements of Net Assets………..……..……….....……..................................................... 3

Schedules of Investments……………..……………………………….......….………….. .4

Statements of Operations…………………………….…………..…….….…….………... 5

Statements of Changes in Net Assets…………………..…..…………………...……....... 6

Statements of Cash Flows………..………………………………………......................... .7

Notes to Financial Statements………………………………………..…………………... 8

Report of Independent Registered Public Accounting Firm

The Member Abilene DC 1, LLC:

Opinion

We have audited the financial statements of Abilene DC 1, LLC (the Company), which comprise the statements of net assets, including the schedules of investment, as of December 31, 2025 and 2024, and the related statements of operations, changes of changes in net assets, and cash flows for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) through December 31, 2024, and the related notes to the financial statements.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2025 and 2024, and the results of its operations, changes in net assets and its cash flows for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) through December 31, 2024 in accordance with U.S. generally accepted accounting principles.

Basis for Opinion

We conducted our audits in accordance with auditing standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of the Company, and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audits. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Responsibilities of Management for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with U.S. generally accepted accounting principles, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company's ability to continue as a going concern for one year after the date that the financial statements are available to be issued.

Auditors’ Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Misstatements are considered material if there is a substantial likelihood that, individually or in the aggregate, they would influence the judgment made by a reasonable user based on the financial statements.

In performing an audit in accordance with GAAS, we:

•Exercise professional judgment and maintain professional skepticism throughout the audit.

•Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements.

•Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control. Accordingly, no such opinion is expressed.

•Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the financial statements.

•Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company's ability to continue as a going concern for a reasonable period of time.

We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal control related matters that we identified during the audit.

KPMG LLP

Chicago, IL

March 12, 2026

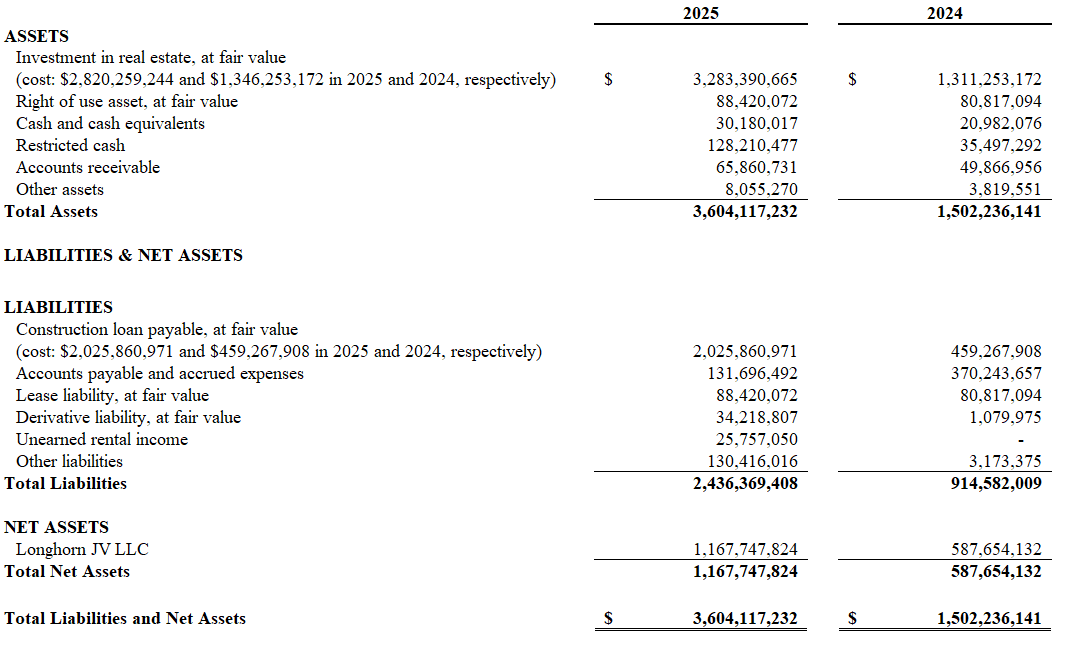

Abilene DC 1, LLC Statements of Net Assets

As of December 31, 2025 and 2024

The accompanying notes are an integral part of the financial statements.

3

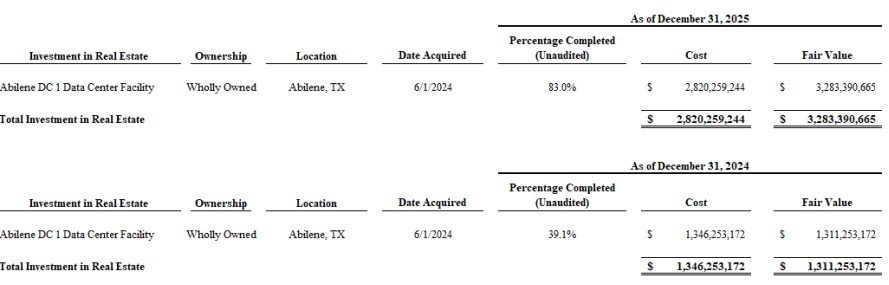

Abilene DC 1, LLC Schedules of Investments

As of December 31, 2025 and 2024

The accompanying notes are an integral part of the financial statements.

4

Abilene DC 1, LLC

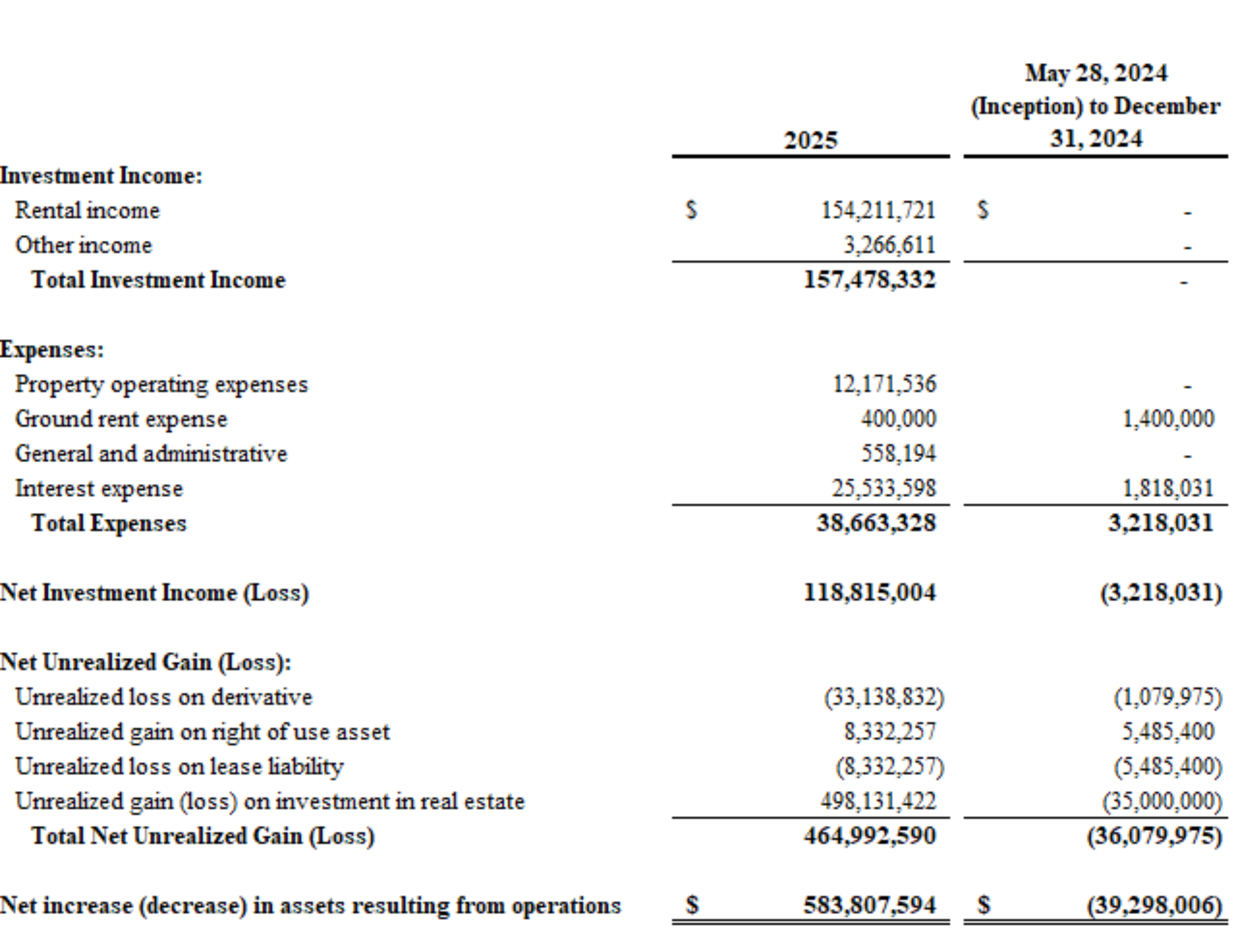

Abilene DC 1, LLCStatements of Operations

For the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

The accompanying notes are an integral part of the financial statements.

5

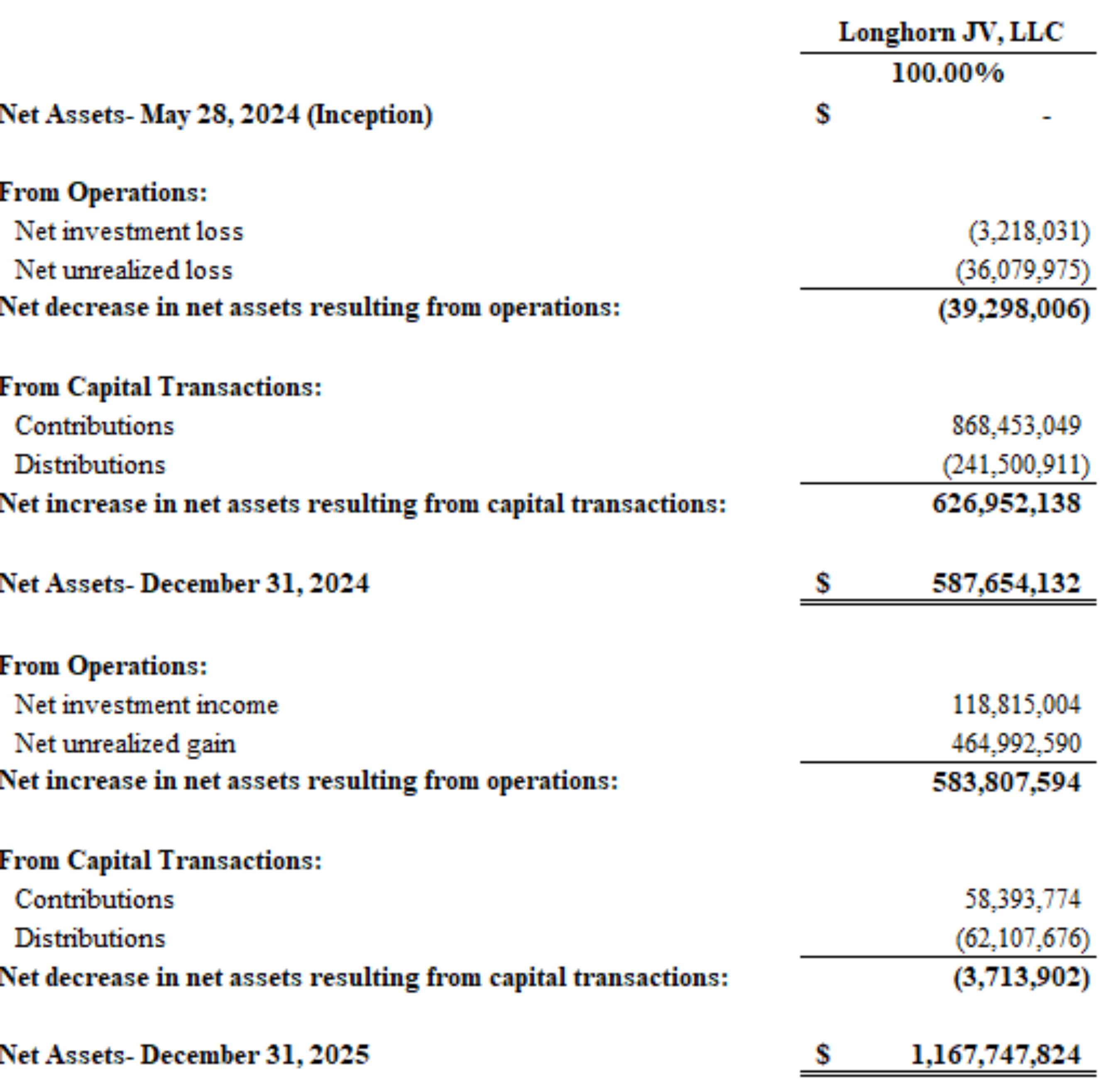

Abilene DC 1, LLC Statements of Changes in Net Assets

For the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

The accompanying notes are an integral part of the financial statements.

6

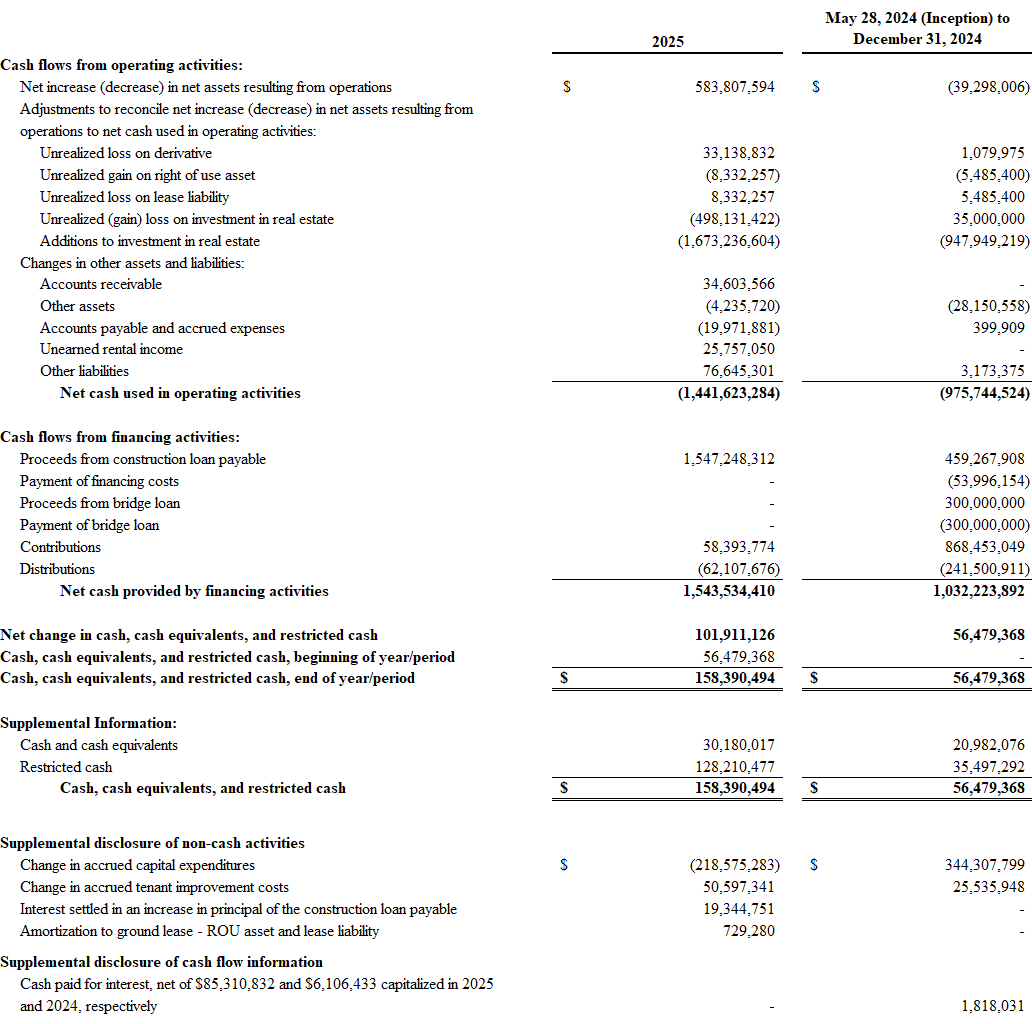

Abilene DC 1, LLC Statements of Cash Flows

For the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

The accompanying notes are an integral part of the financial statements.

7

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

1.Organization and Nature of the Business

Abilene DC 1, LLC (the “Company”) is a single-member limited liability company organized under the laws of the state of Delaware and was formed on May 28, 2024. The Company’s liabilities are solely those of the Company and no member shall be personally obligated for any such liabilities. The Company was formed for the purpose of owning, developing, leasing, and operating a data center campus located in Abilene, Texas (the “Investment”), which is comprised of two buildings each containing four data halls, and a power station. On October 11, 2024, the Company executed a lease with a hyperscale tenant to occupy 100% of the Investment. During the year ended December 31, 2025, the buildings were substantially completed and delivered to the tenant. As of December 31, 2025, the power station remains under development.

The sole member of the Company is Longhorn JV, LLC (“Longhorn JV”), a Delaware limited liability company. Longhorn JV consolidates all activities and operations of the Company, and all authority to conduct the business of the Company is vested in Longhorn JV. At formation, the sole member of Longhorn JV was Crusoe Abilene, LLC (“Crusoe”), a Delaware limited liability company. On October 11, 2024, Crusoe sold 92.26% of its investment to BOREC Longhorn Member, LLC (“BOREC Longhorn”), a Delaware limited liability company. As of December 31, 2025 and 2024, the Company has total equity contributions of $926,846,823 and $868,453,049, respectively. As of December 31, 2025 and 2024, the Company has total equity distributions of $303,608,587 and 241,500,911, respectively.

2. Summary of Significant Accounting Policies

Basis of Presentation

The Company’s financial statements are presented on a fair value basis in conformity with accounting principles generally accepted in the United States of America (“GAAP”). Under Accounting Standards Codification (“ASC”) Topic 946, Financial Services – Investment Companies (“ASC 946”), the Company qualifies as an investment company.

Income and Expense Recognition

Rental income under leases that are deemed probable of collection is recognized as revenue on an accrual basis over the non-cancelable term of the related leases. For leases that are deemed not probable of collection, revenue is recorded as cash received from the tenant, with any tenant receivable balances charged as a direct write-off against rental revenue in the period of the change in the collectability determination. Our estimate of collectability includes, but is not limited to, factors such as the tenant’s payment history, financial condition, industry and geographic area. These estimates could differ materially from actual results.

Property operating expenses are recognized as incurred. The tenant is responsible for the payment of all property operating expenses during the lease term, including, but not limited to, property

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

taxes, repairs and maintenance, insurance and capital expenditures. Management records such expenses on a gross basis.

Investment in Real Estate

The investment in real estate is stated at fair value (see Note 3). The related adjustments, if any, are recorded and shown on the statements of operations as unrealized gain or loss on investment in real estate. As of December 31, 2024, given that the Investment was still undergoing significant development fair value was determined to be the cost of the Investment, including acquisition costs and any construction costs incurred subsequent to purchase less an unrealized loss of $35,000,000 associated with the lessee related cost (see Note 5). As of December 31, 2025, the fair value of the Investment was determined using the discounted cash flow method. In addition to construction costs, the Company capitalizes certain costs related to the development of real estate, including pre-construction costs, real estate taxes, and insurance. Additionally, interest costs related to development activities are capitalized. Capitalization of these costs begins when the activities and related expenditures commence and cease when the project is substantially complete and ready for its intended use. During the year ended December 31, 2025, the buildings were substantially completed and delivered to the tenant.

Cash and Cash Equivalents

The Company considers all highly liquid instruments purchased with an original maturity of three months or less to be cash equivalents. From time to time, amounts deposited in operating cash accounts may be in excess of the FDIC insurance level.

Restricted Cash

Restricted cash includes proceeds from the construction loan that are held in an imprest account and can be disbursed solely for the payment of development costs.

Tenant Construction Costs

Under the terms of the lease agreement, the Company pays certain tenant improvement costs and construction management fees on behalf of the tenant, which are fully reimbursable to the Company. Amounts expected to be collected from the tenant are recorded within accounts receivable, while amounts payable to third‑party vendors or contractors prior to reimbursement are recorded within other liabilities on the statements of net assets.

Construction Loan Payable

The construction loan payable is shown at fair value and is generally classified within Level 3 of the valuation hierarchy (see Note 3). The fair value of the construction loan payable reflects the

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

market value for similar obligations considering their maturities, credit quality, and market interest rates. Fair value adjustments, if any, are shown on the statements of operations as a component of net unrealized gain or loss on construction loan payable. During development, interest expense and loan acquisition costs are capitalized to the cost basis of real estate investments. As of December 31, 2025 and 2024, the Company capitalized a total of $146,738,356 and $61,427,524, respectively, of interest expense and loan acquisition costs into the investment in real estate balance on the statements of net assets.

Derivative Financial Instruments

In the normal course of business, derivative financial instruments are used to manage or hedge interest rate risk. The Company entered into three interest rate swap agreements on its construction loan payable to convert floating rate debt to a fixed rate basis. The derivative financial instruments are recognized as an asset or liability in the statements of net assets at fair value.

The change in the mark-to-market of the value of the derivative financial instruments is recorded to the statements of operations as an unrealized gain or loss on derivatives.

Risks and Uncertainties

In the normal course of business, the Company encounters economic risk, including interest rate risk, credit risk, and market risk. Interest rate risk is the result of movements in mortgage financing rates. Credit risk is the risk of default in the Company’s investments in real estate that results from an underlying tenant’s inability or unwillingness to make contractually required payments. Market risk reflects changes in the valuation of investments in real estate held by the Company.

Income Taxes

As a limited liability company, the Company is not directly subject to federal income taxes. The Company is subject to certain state income taxes which management believes to be insignificant. Therefore, no provision for federal and state income taxes has been provided in the financial statements of the Company. The member is responsible for reporting income or loss to the extent required by the federal and state income tax laws and regulations based upon its ownership of the Company’s income and expenses as reported for income tax purposes.

In accordance with authoritative guidance on how to account for uncertainty in income taxes in ASC Topic 740, Income Taxes, the Company has determined that no uncertain tax positions exist as of December 31, 2025 and 2024. If applicable, the Company will recognize interest and penalties related to underpayment of income taxes as income tax expense. As of December 31, 2025 and 2024, the Company had no amounts related to recognized income tax benefits and incurred no amount related to accrued interest and penalties.

The Company is not required to file any federal, state, or local tax returns in the jurisdictions in which it operates.

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

Management Estimates

The preparation of financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes as of and during the reporting period. Actual results could differ from these estimates.

The real estate and capital markets are cyclical in nature. Property and investment values are affected by, among other things, the availability of capital, occupancy rates, rental rates, interest rates, and inflation rates. As a result, estimating the fair value of investments in real estate involves subjective assumptions and estimates.

Leases – Lessee Accounting

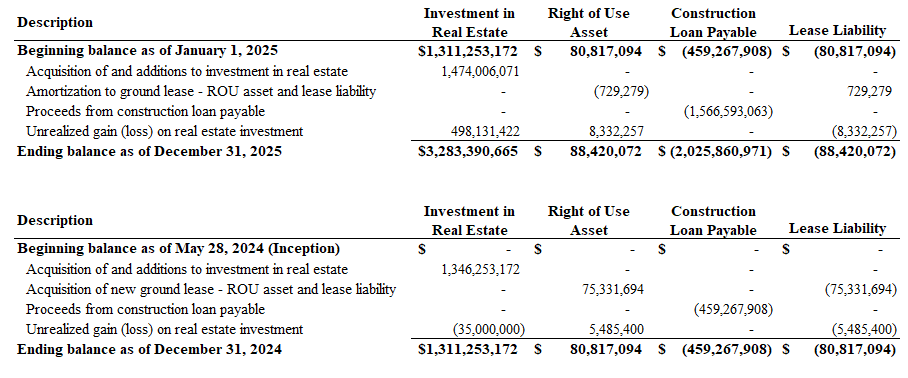

The Company's lease where it is the lessee consists of a ground lease which is classified as a finance lease. The Company has recorded a right of use asset and related lease liability for the rights and obligations associated with this financing lease. In 2024, the Company recognized a lease liability and corresponding right of use asset of $75,331,694 for the ground lease arrangement in which the Company is the lessee. As of December 31, 2025 and 2024, the balance of the lease liability and right of use asset was $88,420,072 and $80,817,094, respectively. The lease liability and right of use asset are shown as separate line items on the statements of net assets.

The Company values the lease liability and right of use asset on a quarterly basis and the amount of unrealized gain (loss) between the lease liability and right of use asset offset to have no material impact on net assets. As of December 31, 2025 and 2024, the Company recorded an unrealized loss of $8,332,257 and $5,485,400, respectively, on the lease liability, and an unrealized gain of $8,332,257 and $5,485,400, respectively, on the right of use asset.

3. Fair Value Measurements

Fair value is based upon ASC Topic 820, Fair Value Measurement “ASC 820”. ASC 820 defines fair value as an exit price in the principal market (or, lacking a principal market, the most advantageous market) in which the reporting entity would enter a transaction.

In determining fair value, the Company uses various valuation approaches. The standard establishes a fair value measurement framework, provides a single definition of fair value, and requires expanded disclosure summarizing fair value measurements. ASC 820 emphasizes that fair value is a market-based measurement, not an entity-specific measurement. Therefore, a fair value measurement should be determined based on the assumptions that market participants would use in pricing an asset or liability.

The standard establishes a hierarchy for inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable input be used when available. Observable inputs are inputs that the market participants would use in pricing the asset or liability developed based on market data obtained from sources

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

independent of the company. Unobservable inputs are inputs that reflect the Company’s assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. The hierarchy is measured in three levels based on the reliability of inputs:

Level 1 – Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities.

Level 2 – Quoted prices for similar assets or liabilities or inputs that are observable, either directly or indirectly, for substantially the full term through corroboration with observable market data. Level 2 includes investments valued at quoted prices adjusted for legal or contractual restrictions.

Level 3 – Pricing inputs are unobservable for the asset or liability, that is, inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability.

The fair value hierarchy is intended to increase consistency and comparability among fair value measures but also plays a critical role in disclosure where it serves to provide users with a construct for considering the relative reliability of various fair value measurements.

In instances where the determination of the fair value measurement is based on inputs from different levels of the fair value hierarchy, the level in the fair value hierarchy within which the entire fair value measurement falls is based on the lowest level of input that is significant to the fair value measurement in its entirety. For the year ended December 31, 2025, there were no transfers between the valuation hierarchy Levels 1, 2, and 3.

Investment in Real Estate

The investment in real estate is shown in the accompanying financial statements at fair value. Fair value is initially based upon the initial purchase price paid by the Company. Fair value is subsequently determined based on appraisals prepared by independent real estate appraisers or internal valuations prepared using valuation approaches described below. Investment values are determined monthly by internal valuations. External appraisals are prepared for the property two years after its acquisition, and annually thereafter, in each case, at the expense of the Company.

External appraisals and internal valuations of investments in real estate usually consider the use of three approaches to value when developing a market value opinion for real property. These are the sales comparison approach, cost approach, and income capitalization approach.

The sales comparison approach is an applicable valuation method for real property because:

a.There is often a market for comparable properties, and sufficient sales data is available for analysis.

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

b.This approach directly considers the prices of alternative properties having similar utility.

The cost approach is an applicable valuation method for real property when the following conditions exist:

a.The property represents new or nearly new construction, which reduces the subjectivity of estimating accrued depreciation.

b.There is an active land market, making estimates of underlying land value reasonably reliable.

The income capitalization approach is an applicable valuation method for real property because:

a.The probable buyer of the property would base a purchase price decision primarily on the income-generating potential of the property and an anticipated rate of return.

b.Sufficient market data regarding income, expenses, capitalization rates, and discount rates, which are significant inputs for analysis, is available through many resources.

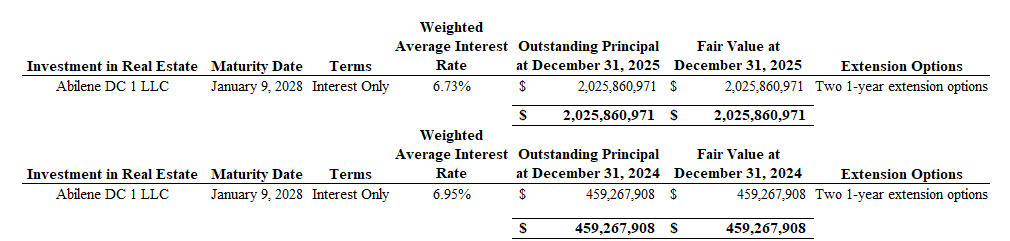

Construction Loan Payable

As of December 31, 2025, the Company’s construction loan payable was held at cost, which approximates fair value.

Right of Use Asset and Lease Liability

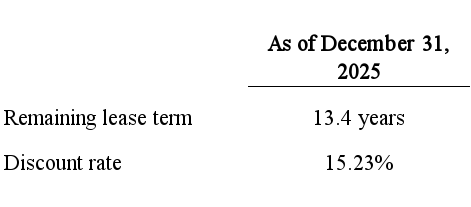

The lease liability and corresponding right of use asset are recorded at fair value. The fair value of the lease liability is determined by discounting the future contractual cash flows to the present value using a discount rate that is implicit in the lease. The discount rate is determined by giving consideration to one or more of the following criteria as appropriate: (i) rates for similar property types, quality, and maturity, and (ii) the fair value of the underlying collateral.

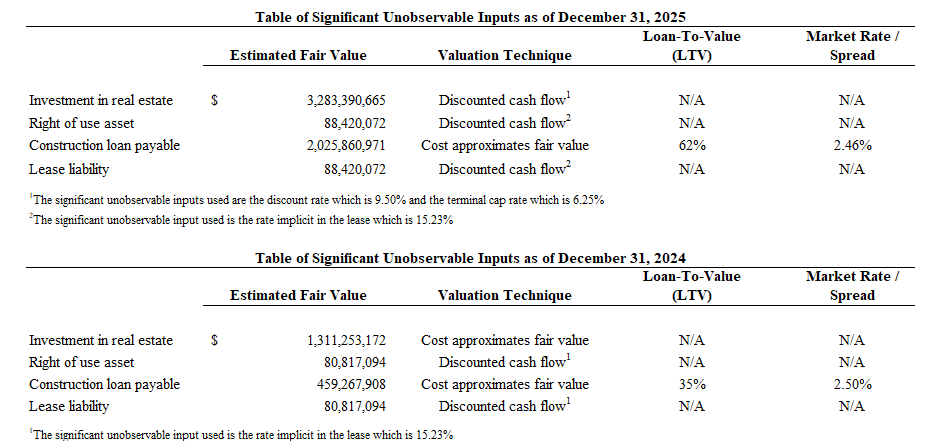

The following table presents the quantitative information about significant unobservable inputs related to the Level 3 fair value measurements used as of December 31, 2025 and 2024:

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

Derivative Financial Instrument

The Company uses Level 2 inputs on the fair value hierarchy to calculate the fair value of its derivative financial instrument. The Company uses widely accepted valuation techniques, including discounted cash flow analysis on the expected cash flows of its derivative financial instrument. This analysis reflects contractual terms of the derivative financial instrument, including the period to maturity, and uses observable market-based inputs, including interest rate curves and implied volatilities. The fair value of the interest rate swap is determined using market standard methodology of netting the discounted future fixed cash receipts (or payments). The variable cash payments (or receipts) are based on an expectation of future interest rates (forward curves) derived from observable market interest rate curves.

As of December 31, 2024, the Company entered into one floating-to-fixed interest rate swap on the SOFR-based floating portion of its construction loan payable with a strike rate of 3.980%. On February 27, 2025, the agreement was amended to extend the maturity date to January 9, 2028. The notional amount of the swap equaled $2,261,773,483 and $459,603,884 as of December 31, 2025 and 2024, respectively. The notional amount of the swap will accrete according to the notional schedule agreed upon per the terms of the swap agreement, with the final notional amount being $2,498,000,000 as of April 9, 2026. On March 9, 2025, the Company entered into two floating-to-fixed interest rate swaps on the SOFR-based floating portion of its construction loan payable with a strike rate of 3.980%. The notional amount of the swaps equaled $220,963,600 as of December 31, 2025, and will mature on January 9, 2028.

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

The notional amount of the swaps will accrete according to the notional schedule agreed upon per the terms of the swap agreement, with the final notional amount being $222,322,000 as of April 9, 2026.

All other assets and liabilities are carried at cost, which approximates fair value, since these are the amounts which are expected to be realized upon liquidation. Although the Company’s valuation processes described above are designed to estimate fair value, uncertainties in the appraisal/valuation process may cause the recorded value of reported assets and liabilities of the Company to differ significantly from that which would have been obtained if they were actually offered for sale in the marketplace.

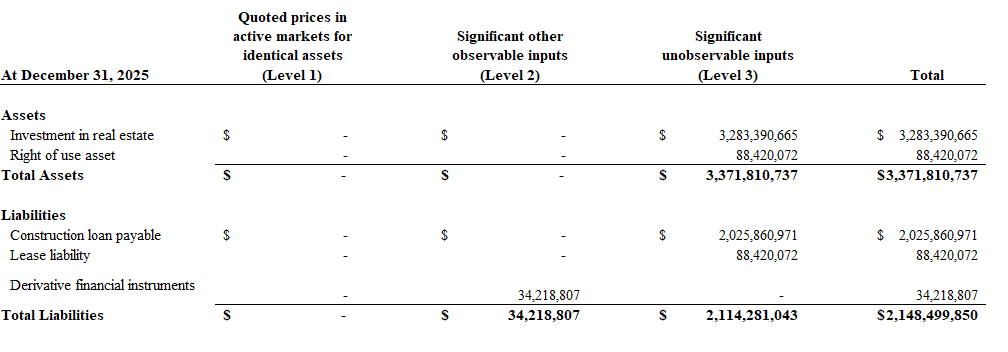

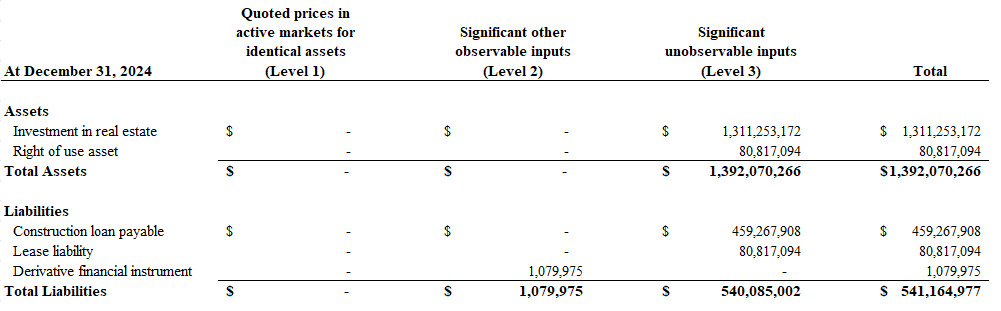

The following are the classes of assets and liabilities measured at fair value on a recurring basis for the year ended December 31, 2025 and 2024, using unadjusted quoted prices in active markets for identical assets (Level 1); significant other observable inputs (Level 2); and significant unobservable inputs (Level 3):

The following table summarizes the changes in investment in real estate, right of use asset, construction loan payable, and lease liability, measured at fair value on a recurring basis using Level 3 inputs for the year ended December 31, 2025 and 2024:

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

4. Construction Loan Payable

On December 16, 2024, the Company entered into a construction loan related to the investment in real estate. Based on the executed loan agreement, the Company can borrow up to $2,288,000,000. The construction loan is interest only and bears interest at one of the following rates based on the type of loan and rate established at the time of each draw: (a) the Term SOFR Rate plus the spread of 2.5%, (b) an Alternate Rate based on the Alternate Rate Index determined by the lender, or (c) the Prime Rate based on the index established by the lender.

The construction loan payable is subject to compliance with financial and construction covenants, and management believes the Company was in compliance with such covenants as of December 31, 2025 and 2024. The construction loan payable as of December 31, 2025 and 2024, consisted of the following property-level obligation:

As of December 31, 2025 and 2024, aggregate contractual maturities of debt are due in 2028.

5. Leasing

Lessee

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

The Company leases land owned by Lancium (an unrelated third party) which commenced on May 31, 2024. The Company determines whether an arrangement is a lease at inception by establishing if the contract conveys the right to control the use of identified property, plant, or equipment for a period of time in exchange for consideration.

The lease covers an initial term of 20 years with the option to extend this initial term for up to five additional periods of 15 years each. The lease grants the Company an option to purchase the land on or at any time following May 31, 2039, for the purchase price of $1. As the Company is reasonably certain to exercise this purchase option, the lease term was determined to be 15 years.

Per the terms of the ground lease agreement, monthly rent shall initially be $200,000 during the construction period. Upon completion of the first data hall within the Investment, monthly rent shall be based on the total megawatts of all data halls energized and commissioned at the time, with the minimum amount to be paid each month remaining at $200,000. The ground rent expense shall be passed through to the tenant under the terms of the property Lease Agreement where the Company is the lessor. The total ground lease rent expense recorded by the Company during the year ended December 31, 2025, was $400,000, which is included in rent expense on the accompanying statements of operations.

On October 11, 2024, the Company executed the second amendment to the ground lease and easement agreement with Lancium. In this amendment, the Company agreed to make a one-time payment of $35,000,000 associated with the land covered by the ground lease and upon which the Investment is being constructed. While the Investment is leased to a tenant, the tenant will be responsible for making monthly payments for power directly to Lancium. Per the terms of the amendment, if the tenant were to vacate the space, the up-front reservation payment would cover any fees that would be charged to the Company to continue having power provided to the site rather than the Company assuming the monthly payments.

Lease term and discount rate information is summarized as follows:

Lessor

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

The Company is a lessor of development real estate property. The Investment is 100% leased to a single tenant. The leased area includes two buildings which are each comprised of four data halls. On March 18, 2025 and July 1, 2025, rent commenced for building 1 and building 2, respectively.

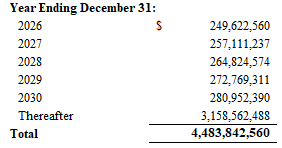

The lease term is 15 years from the rent commencement date. Based on the terms of the lease agreement, monthly rent includes base rent and additional rent. Base rent for the first lease year is $2,475,000 per data hall and $297,000 for the network core of each building. Base rent for each successive lease year shall increase by 3% on each one-year anniversary of the rent commencement date. Additional rent includes an estimate of operating costs for common area of the investment, real estate taxes, insurance premiums and monthly rent under the ground lease agreement. For the year ended December 31, 2025, the additional rent recognized on the statement of operations as rental income and property operating expenses is $12,046,759.

As of December 31, 2025 the future minimum rent payment is summarized as follows:

6. Related-Party Transactions

The Company is wholly owned by Longhorn JV LLC. Crusoe Abilene LLC and BOREC Longhorn Member LLC hold a 7.7% and 92.3% interest, respectively, in Longhorn JV. In connection with owning and developing the Investment through the Company, affiliates of Crusoe Abilene are paid a development fee.

An affiliate of Crusoe Abilene shall receive a development fee equal to $13,000,000 which shall be paid in thirteen equal monthly installments of $900,000 between October 11, 2024 (Effective Date of the Development Management Agreement) and the anticipated date of substantial completion of the development, and the final balance of $1,300,000 upon completion of development. Development fees incurred and paid were $6,617,000 and $9,000,000, respectively, for the year ended December 31, 2025, and $5,083,000 and $2,700,000, respectively, for the period from May 28, 2024 (Inception) to December 31, 2024. As of December 31, 2025 and 2024, $0 and $2,383,000, respectively, in fees remained accrued and are recorded in accounts payable and accrued expense on the statements of net assets. Development fees incurred are capitalized and recorded as investment in real estate on the statements of net assets.

7. Commitments and Contingencies

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

In the normal course of business, from time to time, the Company may be involved in legal actions relating to the ownership and operations of investments in real estate. In management’s opinion, the liabilities, if any, that may ultimately result from such legal actions are not expected to have a material effect on the Company’s financial position, results of operations or liquidity.

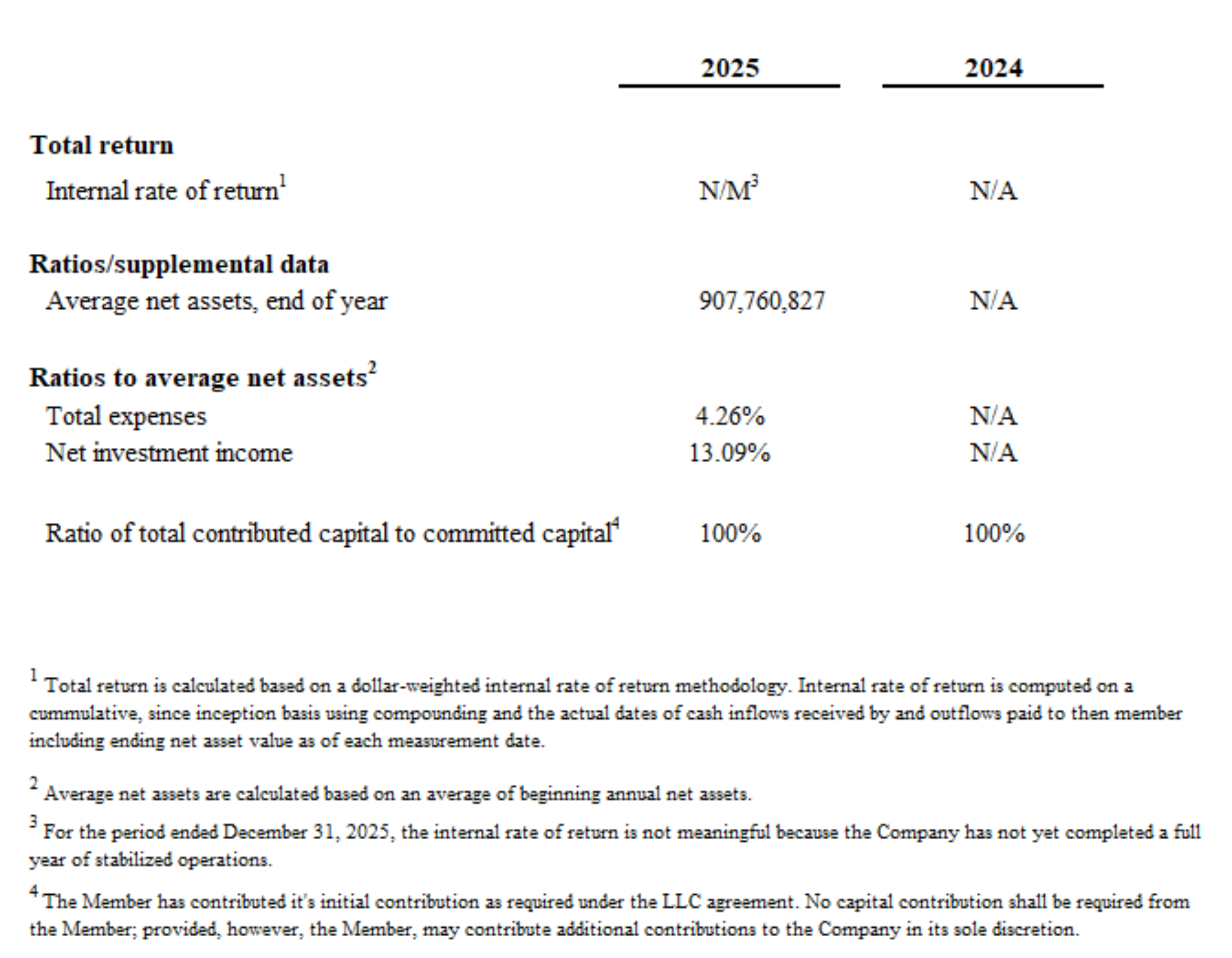

8. Financial Highlights

The financial highlights for the Company as of and for the year ending December 31, 2025, and as of December 31, 2024 and for the period from May 28, 2024 (Inception) to December 31, 2024 are as follows:

Abilene DC 1, LLC Notes to Financial Statements

As of December 31, 2025 and 2024, for the year ended December 31, 2025 and for the period from May 28, 2024 (Inception) to December 31, 2024

9. Subsequent Events

The Company has evaluated activity through March 12, 2026, the date the financial statements were available to be issued and has concluded that no additional subsequent events have occurred that would require recognition or additional disclosure.