|

PROSPECTUS |

Filed Pursuant to Rule 424(b)(3) |

2,200,000 Class A Ordinary Shares

Linkers Industries Limited

This Resale Prospectus relates to the resale of 2,200,000 Class A Ordinary Shares in aggregate by the Selling Shareholders named in this prospectus. We will not receive any of the proceeds from the sale of Class A Ordinary Shares by the Selling Shareholders named in this prospectus.

Any shares sold by the Selling Shareholders covered by this prospectus will only occur after the commencement of trading of our Ordinary Shares on the Nasdaq Capital Market, and such sales will begin at prevailing market prices or at privately negotiated prices. No sales of the shares covered by this prospectus shall occur until after completion of our initial public offering. No shares covered by this prospectus will be sold through R.F. Lafferty & Co., Inc. or Revere Securities LLC in our initial public offering, nor will they receive any compensation from the sale of these shares. The distribution of securities offered hereby may be effected in one or more transactions that may take place in ordinary brokers’ transactions, privately negotiated transactions or through sales to one or more dealers for resale of such securities as principals. The Selling Shareholders will sell their shares at prevailing market prices or in privately negotiated prices. Usual and customary or specifically negotiated brokerage fees or commissions may be paid by the Selling Shareholders. The date of effectiveness of this registration statement is December 4, 2024.

The Class A Ordinary Shares registered for resale as part of this Resale Prospectus, once registered, will constitute a considerable percentage of our public float. The sales of a substantial number of registered shares could result in a significant decline in the public trading price of our Class A Ordinary Shares and could impair our ability to raise capital through the sale or issuance of additional Class A Ordinary Shares. We are unable to predict the effect that such sales may have on the prevailing market price of our Class A Ordinary Shares. Despite such a decline in the public trading price, certain Selling Shareholders may still experience a positive rate of return on the Class A Ordinary Shares due to the lower price that they purchased the Class A Ordinary Shares compared to other public investors and may be incentivized to sell their Class A Ordinary Shares when others are not. See “Risk Factors — Risks Related to our Corporate Structure — The future sales of Class A Ordinary Shares by existing shareholders, including the sales pursuant to the Resale Prospectus, may adversely affect the market price of our Class A Ordinary Share.”

Prior to this offering, there has been no public market for our Class A Ordinary Shares. The offering price of our Class A Ordinary Shares in this offering is US$4 per share. We have received the approval letter to have our Ordinary Shares listed on the Nasdaq Capital Market under the symbol “LNKS”. We will be a “controlled company” as defined under the Nasdaq Stock Market Rules because, immediately after the completion of this offering and the sale of our Class A Ordinary Shares by the Selling Shareholders pursuant to the Resale Prospectus, Mr. Man Tak Lau, our controlling shareholder (“Controlling Shareholder”) will own 5,829,500 Class A Ordinary Shares and 2,500,000 Class B Ordinary Shares, being 63.34% of our total issued and outstanding Ordinary Shares and representing 92.05% of the total voting power, assuming that the underwriters do not exercise their over-allotment option. As a result, our Controlling Shareholder will have the ability to control the outcome of certain matters submitted to shareholders for approval through his controlling ownership of the Company, such as the election of directors, amendments to our organizational documents and any merger, consolidation, sale of all or substantially all of our assets or other major corporate transactions. See “Risk Factors — Risks Related to our Class A Ordinary Shares — our Controlling Shareholder has significant voting power and may take actions that may not be in the best interests of our other shareholders” for further information. However, even if we are deemed as a “controlled company,” we do not intend to avail ourselves of the corporate governance exemptions afforded to a “controlled company” under the Nasdaq Stock Market Rules. See “Risk Factors — We are a “controlled company” within the meaning of the Nasdaq listing rules, and may follow certain exemptions from certain corporate governance requirements that could adversely affect our public shareholders.”

LIL is a holding company registered and incorporated in the British Virgin Islands (“BVI”), and is not a Malaysian operating company. As a holding company with no material operations, we conduct our operations in Malaysia through our operating subsidiary, TEM. This is an offering of the Class A Ordinary Shares of LIL, the holding company incorporated in the BVI, instead of shares of our operating subsidiary, TEM. You may never directly hold any equity interest in our operating subsidiary.

The date of this Resale Prospectus is December 4, 2024

PROSPECTUS SUMMARY

The following summary highlights information contained elsewhere in the Public Offering Prospectus and does not contain all of the information you should consider before investing in our Class A Ordinary Shares. You should read the entire prospectus carefully, including “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and the related notes thereto, in each case included in the Public Offering Prospectus. You should carefully consider, among other things, the matters discussed in the section of this prospectus titled “Business” before making an investment decision.

Overview

Through our operating subsidiary, we are a manufacturer and a supplier of wire/cable harnesses with our manufacturing operations in Malaysia and have more than 20 years’ experience in the wire/cable harnesses industry. Wire/cable harness refers to an assembly of wires/cables bound together with straps, cable ties and electrical tapes to transmit signals or electrical power. Our customers are generally global brand name manufacturers and original equipment manufacturers (“OEMs”) in the home appliances, industrial products and automotive industries that are mainly based in the Asia Pacific Region.

We work closely with customers in each stage of a product’s life cycle, including design, prototyping and production. Our business model enables us to offer customized wire harness for different applications and electrics designs. Our products are customized and made-to-order in accordance with the specific technical requirements of our customers.

Our Competitive Strengths

We believe the following competitive strengths differentiate our operating subsidiary from its competitors:

• Customer base in diversified industries and long-term business relationship with renowned global brand name manufacturers and OEMs;

• Extensive understanding of wire harness production process, up to date machinery and efficient management resulting in competitive pricing while maintaining quality;

• High standard and commitment to quality control;

• Strong customized production platform; and

• Experienced management team with extensive knowledge of the manufacturing industry where we operate.

Our Strategies

We aim to accomplish our business objective, further strengthen our market position and continue to be a competitive manufacturer and supplier of wire/cable harnesses by pursing the following key strategies:

• Upgrade and increase our production capacity;

• Strengthen our sales and marketing efforts to diversify our customer base;

• Enhance our capability level; and

• Acquisition of companies and/or formation of joint ventures.

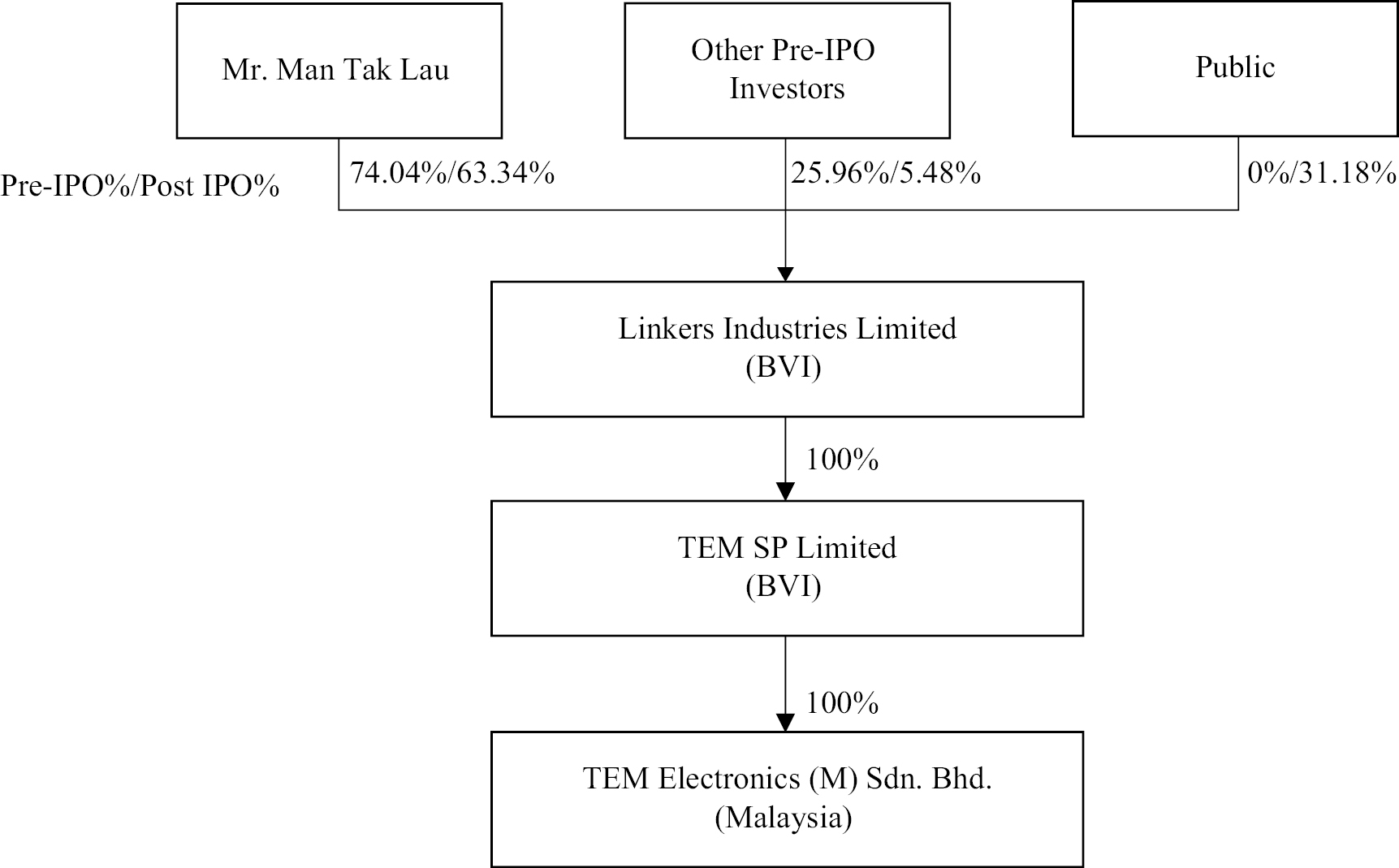

Corporate History and Structure

On October 31, 1995, TEM was established under the laws of Malaysia to engage in the business of manufacturing connectors, assemblies and wire/cable harness. TSPL was incorporated under the laws of the BVI on November 15, 2022 as an investment holding company. As part of the reorganization, on December 14, 2022, TSPL acquired the entire issued share capital of TEM.

Alt-1

On December 8, 2022, LIL was incorporated under the laws of the BVI as a holding company. As part of the reorganization, on December 21, 2022, LIL acquired the entire issued share capital of TSPL, following which TSPL was wholly-owned by LIL, and TEM was indirectly wholly-owned by LIL.

We are offering 2,200,000 Class A Ordinary Shares, representing 16.73% of the Ordinary Shares following the completion of this offering, assuming the underwriters do not exercise their over-allotment option. The chart below illustrates our corporate structure and identify our subsidiaries as of the date of this prospectus/upon completion of this offering:

We will be a “controlled company” as defined under the Nasdaq Stock Market Rules because, immediately after the completion of this offering and the sale of our Class A Ordinary Shares by the Selling Shareholders pursuant to the Resale Prospectus, our Controlling Shareholder, will own 63.34% of our total issued and outstanding Ordinary Shares, representing 92.05% of the total voting power, assuming that the underwriters do not exercise their over-allotment option, and may have the ability to determine matters requiring approval by shareholders.

Investors are purchasing securities of our holding company, LIL, instead of securities of our operating subsidiary, through which our operations are conducted.

Transfers of Cash to and from Our Subsidiaries

As part of our cash management policies and procedures, our management monitors the cash position of our subsidiaries regularly and prepares budgets on a monthly basis to ensure it has the necessary funds to fulfil its obligations for the foreseeable future and to ensure adequate liquidity. In the event that there is a need for cash or a potential liquidity issue, it will be reported to our chief financial officer and subject to approval by our board of directors.

Cash is transferred through our organization in the following manner: (i) funds are transferred to TEM, our operating subsidiary in Malaysia, from LIL as needed through our BVI subsidiary in the form of capital contributions or shareholder loans, as the case may be; and (ii) dividends or other distributions may be paid by TEM to LIL through our BVI subsidiary.

Under BVI Act, a BVI company can provide funding to its direct subsidiary (i) by making shareholder’s loan, (ii) by way of further subscription for shares or (iii) by way of capital contribution without subscribing for further shares. For LIL to transfer cash to its subsidiaries, LIL is permitted under the laws of the BVI to provide funding to its direct subsidiary, TSPL, in the three aforementioned ways subject to certain restrictions laid down in the BVI Act (as

Alt-2

amended) and the memorandum and articles of association of LIL. Similarly, TSPL is permitted under the laws of the BVI to provide funding to our operating subsidiary, TEM, in the three aforementioned ways subject to certain restrictions laid down in the BVI Act (as amended) and the memorandum and articles of association of TSPL.

TEM’s ability to transfer funds to us in the form of dividends or other distributions is not materially restricted by regulatory provisions in accordance with laws and regulations in Malaysia. TEM is free to remit divestment proceeds, profits, dividends, or any income arising from any investment in Malaysia, as long as the payment is made in foreign currency, instead of Malaysian Ringgit, and in accordance with the Foreign Exchange Notices issued by the Bank Negara Malaysia (the Central Bank of Malaysia) (“BNM”).

Under the BVI Act (as amended), subject to the memorandum and articles of association, a BVI company may make a dividend distribution to its shareholders to the extent that immediately after the distribution, the value of the company’s assets exceeds its liabilities and that such company is able to pay its debts as they fall due.

Other than the above, we did not adopt or maintain any cash management policies and procedures dictating the amount of such funding or how funds are transferred and our subsidiaries have not experienced any difficulties or limitations on their ability to transfer cash between each other, to distribute earnings from our subsidiaries to LIL and to settle amounts owed under any applicable agreements as of the date of this prospectus.

During the years ended June 30, 2024 and 2023, LIL did not declare or pay any dividends or distributions and there was no transfer of assets among LIL and its subsidiaries.

We do not expect to pay dividends on our Shares in the foreseeable future. We currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our operating subsidiary’s business. Any future determination related to our dividend policy will be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and other factors the board of directors deems relevant, and subject to the restrictions contained in any future financing instruments.

Enforcement of Civil Liabilities

We are incorporated under the laws of the BVI with limited liability. Substantially all of our assets are located outside the United States. In addition, all of our directors and executive officers are nationals or residents in Malaysia or Hong Kong and substantially all of their assets are located outside the United States. As a result, it may be difficult for you to effect service of process within the United States upon us or these persons, or to enforce judgments obtained in U.S. courts against us or them, including judgments predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States. It may also be difficult for you to enforce judgments obtained in U.S. courts based on the civil liability provisions of the U.S. federal securities laws against us and our executive officers and directors. See “Risk Factors — Risks Related to our Ordinary Shares — You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions in Malaysia or Hong Kong against us or our directors named in the prospectus based on foreign laws.” for more information.

We have appointed Cogency Global Inc. as our agent upon whom process may be served in any action brought against us under the securities laws of the United States.

Conyers Dill & Pearman, our counsel as to the laws of the BVI, has advised us that there is uncertainty as to whether the courts of the BVI would (i) recognize or enforce judgments of United States courts obtained against us or our directors or officers to impose liabilities predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States; or (ii) entertain original actions brought in the BVI against us or our directors or officers predicated upon the federal securities laws of the United States or the securities law of any state in the United States.

We have been advised by Conyers Dill & Pearman that although there is no statutory enforcement in the BVI of judgments obtained in the federal or state courts of the United States (and the BVI is not a party to any treaties for the reciprocal enforcement or recognition of such judgments), the courts of the BVI would recognize as a valid judgment, a final and conclusive judgment in personam obtained in the federal or state courts in the United States under which a sum of money is payable (other than a sum of money payable in respect of multiple damages, taxes or other charges of a like nature or in respect of a fine or other penalty) and would give a judgment based thereon provided that (a) such courts had proper jurisdiction over the parties subject to such judgment, (b) such courts did not contravene the rules of natural justice of the BVI, (c) such judgment was not obtained by fraud, (d) the enforcement of the judgment would

Alt-3

not be contrary to the public policy of the BVI, (e) no new admissible evidence relevant to the action is submitted prior to the rendering of the judgment by the courts of the BVI and (f) there is due compliance with the correct procedures under the laws of the BVI. However, the BVI courts are unlikely to enforce a punitive judgment of a United States court predicated upon the civil liability provisions of the federal securities laws in the United States without retrial on the merits if such judgment is determined by the courts of the BVI to give rise to obligations to make payments that may be regarded as fines, penalties or punitive in nature.

Mah-Kamariyah & Philip Koh, our counsel as to the laws of Malaysia, has advised us that the enforcement of a foreign judgment in Malaysia could be effected through either statutory enforcement or the common law rule of enforcement. Under the Reciprocal Enforcement of Judgments Act 1958 of Malaysia, or REJA, judgments given by superior courts of reciprocating countries, as listed in the First Schedule to the REJA are recognized and may be enforced directly or summarily by way of registration of the judgment provided that such judgments satisfy the requirements as specified under the REJA. Foreign judgments obtained in countries other than the countries listed in the First Schedule to REJA, have to be enforced through the common law rule. Although the United States is not a reciprocating country listed in the First Schedule to the REJA, a judgment pronounced in the United States may still be enforced in Malaysia pursuant to Malaysian common law principles provided that such foreign judgments must fulfil certain conditions which includes the following:

(a) the judgment is for a definite sum, and which is final and conclusive;

(b) the original court granting the judgment had jurisdiction in the action;

(c) the judgment was not obtained by fraud;

(d) the proceedings in which the judgment was obtained were not contrary to natural justice; and

(e) the enforcement of the judgment would not be contrary to public policy in Malaysia.

Hong Kong has no arrangement for the reciprocal enforcement of judgments with the United States. As a result, there is uncertainty as to the enforceability in Hong Kong, in original actions or in actions for enforcement, of judgments of United States courts of civil liabilities predicated solely upon the federal securities laws of the United States or the securities laws of any State or territory within the United States.

Hastings & Co., our counsel as to the laws of Hong Kong, has advised us that there is uncertainty as to whether the courts of Hong Kong would (i) recognize or enforce judgments of United States courts obtained against us or our directors or officers predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States or (ii) entertain original actions brought in Hong Kong against us or our directors or officers predicated upon the securities laws of the United States or any state in the United States.

A judgment of a court in the United States predicated upon U.S. federal or state securities laws may be enforced in Hong Kong at common law by bringing an action in a Hong Kong court on that judgment for the amount due thereunder, and then seeking summary judgment on the strength of the foreign judgment, provided that the foreign judgment, among other things, is (1) for a debt or a definite sum of money (not being taxes or similar charges to a foreign government taxing authority or a fine or other penalty); and (2) final and conclusive on the merits of the claim, but not otherwise. Such a judgment may not, in any event, be so enforced in Hong Kong if (a) it was obtained by fraud; (b) the proceedings in which the judgment was obtained were opposed to natural justice; (c) its enforcement or recognition would be contrary to the public policy of Hong Kong; (d) the court of the United States was not jurisdictionally competent; or (e) the judgment was in conflict with a prior Hong Kong judgment.

Summary of Key Risk Factors

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may materially and adversely affect our business, financial condition, results of operations, cash flows and prospects that you should consider before making a decision to invest in our Class A Ordinary Shares. These risks are discussed more fully in “Risk Factors”. These risks include, but are not limited to, the following:

Risks Related to Doing Business in Malaysia (for a more detailed discussion, see “Risk Factors — Risks Related to Doing Business in Malaysia” beginning on page 14 of this prospectus)

• Our operations are subject to various laws and regulations in Malaysia (see page 14 of this prospectus).

Alt-4

• Developments in the social, political, regulatory and economic environment in Malaysia may have a material adverse impact on us (see page 14 of this prospectus).

• We face the risk that changes in the policies of the Malaysian government could have a significant impact upon the business we may be able to conduct in Malaysia and the profitability of such business (see page 15 of this prospectus).

• Fluctuations in exchange rates could adversely affect our business and the value of our securities (see page 15 of this prospectus).

• We are subject to foreign exchange control policies in Malaysia (see page 15 of this prospectus).

Risks Related to Our Business and Industry (for a more detailed discussion, see “Risk Factors — Risks Related to Our Business and Industry” beginning on page 16 of this prospectus)

• Fluctuations in the prices of our major raw materials could materially and adversely affect our business, financial conditions and results of operations (see page 16 of this prospectus).

• An unanticipated or prolonged interruption of operations at production facility would have a material and adverse effect on our business, financial conditions and results of operations (see page 16 of this prospectus).

• Our failure to acquire raw materials or to fill our customers’ orders in a timely and cost-effective manner could materially and adversely affect our business operations (see page 17 of this prospectus).

• The economy in general may not grow as quickly as expected, which could adversely affect our revenues and business prospects (see page 17 of this prospectus).

• We generate a significant amount of export sales. Conducting business in overseas markets involves risks and uncertainties such as foreign exchange rate exposure and political and economic instability that could lead to reduced overseas sales and reduced profitability associated with such sales (see page 17 of this prospectus).

• If we fail to effectively implement our production plan or our inventories become obsolete, our future performance and operating results will be adversely affected (see page 17 of this prospectus).

• We rely on a limited number of major customers, of which may reduce or stop making purchase orders for our products (see page 18 of this prospectus).

Risks Related to our Corporate Structure (for a more detailed discussion, see “Risk Factors — Risks Related to our Corporate Structure” beginning on page 23 of this prospectus)

• Our dual-class voting structure will limit your ability to influence corporate matters and could discourage others from pursuing any change of control transactions that holders of our Class B Ordinary Shares may view as beneficial (see page 23 of this prospectus).

• We cannot predict the effect our dual-class structure may have on the market price of our Class A Ordinary Shares (see page 23 of this prospectus).

• The future sales of Ordinary Shares by existing shareholders, including the sales pursuant to the Resale Prospectus, may adversely affect the market price of our Ordinary Share. (see page 24 of this prospectus).

• Our Controlling Shareholder has significant voting power and may take actions that may not be in the best interests of our other shareholders (see page 24 of this prospectus).

• We are a “controlled company” within the meaning of the Nasdaq listing rules, and may follow certain exemptions from certain corporate governance requirements that could adversely affect our public shareholders (see page 24 of this prospectus).

• Our Controlling Shareholder’s shareholdings in companies with similar businesses may lead to conflicts of interest with our Company and our other shareholders (see page 25 of this prospectus).

• Certain of our directors may allocate their time to other businesses, thereby causing conflicts of interest in their determination as to how much time to devote to our affairs (see page 25 of this prospectus).

Alt-5

Risks Related to our Class A Ordinary Shares (for a more detailed discussion, see “Risk Factors — Risks Related to our Class A Ordinary Shares” beginning on page 25 of this prospectus)

• If we fail to meet applicable listing requirements, Nasdaq may not approve our listing application, or may delist our Class A Ordinary Shares from trading, in which case the liquidity and market price of our Class A Ordinary Shares could decline (see page 25 of this prospectus).

• There has been no public market for our Class A Ordinary Shares prior to this offering, and you may not be able to resell our Class A Ordinary Shares at or above the price you pay for them, or at all (see page 26 of this prospectus).

• Our Class A Ordinary Shares are expected to initially trade under US$5.00 per share and thus would be known as “penny stock.” Trading in penny stocks has certain restrictions and these restrictions could negatively affect the price and liquidity of our Class A Ordinary Shares (see page 26 of this prospectus).

• Volatility in the price of our Class A Ordinary Shares may subject us to securities litigation (see page 26 of this prospectus).

• The market price of our Class A Ordinary Shares may be highly volatile, and you could lose all or part of your investment (see page 27 of this prospectus).

• Our pre-IPO shareholders, including our Controlling Shareholder, will be able to sell their shares after completion of this offering subject to restrictions under Rule 144 (see page 27 of this prospectus).

• Substantial future sales or perceived sales of our Class A Ordinary Shares in the public market could cause the price of our Class A Ordinary Shares to decline (see page 28 of this prospectus).

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY

As a company with less than US$1.235 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”), enacted in April 2012. An “emerging growth company” may take advantage of reduced reporting requirements that are otherwise applicable to larger public companies. In particular, as an emerging growth company, we:

• may present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations;

• are not required to provide a detailed narrative disclosure discussing our compensation principles, objectives and elements and analyzing how those elements fit with our principles and objectives, which is commonly referred to as “compensation discussion and analysis;”

• are not required to obtain an attestation and report from our auditors on our management’s assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002;

• are not required to obtain a non-binding advisory vote from our shareholders on executive compensation or golden parachute arrangements (commonly referred to as the “say-on-pay”, “say-on frequency” and “say-on-golden-parachute” votes);

• are exempt from certain executive compensation disclosure provisions requiring a pay-for-performance graph and chief executive officer pay ratio disclosure;

• are eligible to claim longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act; and

• will not be required to conduct an evaluation of our internal control over financial reporting.

We intend to take advantage of all of these reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act. Our election to use the phase-in periods may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the phase-in periods under §107 of the JOBS Act.

Alt-6

We will remain an emerging growth company until the earliest of (i) the last day of the fiscal year during which we have total annual gross revenues of at least US$1.235 billion; (ii) the last day of our fiscal year following the fifth anniversary of the completion of this offering; (iii) the date on which we have, during the preceding three-year period, issued more than US$1.0 billion in non-convertible debt; or (iv) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur if the market value of our Class A Ordinary Shares that are held by non-affiliates exceeds US$700 million as of the last business day of our most recently completed second fiscal quarter. Once we cease to be an emerging growth company, we will not be entitled to the exemptions provided in the JOBS Act discussed above.

IMPLICATIONS OF BEING A FOREIGN PRIVATE ISSUER

We are a “foreign private issuer” within the meaning of the rules under the Exchange Act. As such, we are exempt from certain provisions of the Exchange Act that are applicable to United States domestic public companies. For example:

• we are not required to provide as many Exchange Act reports, or as frequently, as a domestic public company;

• for interim reporting, we are permitted to comply solely with our home country requirements, which are less rigorous than the rules that apply to domestic public companies;

• we are not required to provide the same level of disclosure on certain issues, such as executive compensation;

• we are exempt from provisions of Regulation Fair Disclosure aimed at preventing issuers from making selective disclosures of material information;

• we are not required to comply with the sections of the Exchange Act regulating the solicitation of proxies, consents, or authorizations in respect of a security registered under the Exchange Act; and

• our officers, directors and principal shareholders are not required to comply with Section 16 of the Exchange Act requiring them to file public reports of their share ownership and trading activities and establishing insider liability for profits realized from any “short-swing” trading transaction.

Furthermore, Nasdaq Rule 5615(a)(3) provides that a foreign private issuer, such as us, may rely on our home country corporate governance practices in lieu of certain of the rules in the Nasdaq Rule 5600 Series and Rule 5250(d), provided that we nevertheless comply with Nasdaq’s notification of non-compliance requirement (Rule 5625), the voting rights requirement (Rule 5640) and that we have an audit committee that satisfies Rule 5605(c)(3), consisting of committee members that meet the independence requirements of Rule 5605(c)(2)(A)(ii). If we rely on our home country corporate governance practices in lieu of certain of the rules of Nasdaq, our shareholders may not have the same protections afforded to shareholders of companies that are subject to all of the corporate governance requirements of Nasdaq. If we choose to do so, we may utilize these exemptions for as long as we continue to qualify as a foreign private issuer.

IMPLICATIONS OF BEING A CONTROLLED COMPANY

Controlled companies are exempt from the majority of independent director requirements. Controlled companies are subject to an exemption from Nasdaq standards requiring that the board of a listed company consist of a majority of independent directors within one year of the listing date.

Public Companies that qualify as a “controlled company” with securities listed on the Nasdaq, must comply with the exchange’s continued listing standards to maintain their listings. Nasdaq has adopted qualitative listing standards. Companies that do not comply with these corporate governance requirements may lose their listing status. Under the Nasdaq rules, a “controlled company” is a company with more than 50% of its voting power held by a single person, entity or group. Under Nasdaq rules, a “controlled company” is exempt from certain corporate governance requirements including:

• the requirement that a majority of the board of directors consist of independent directors;

Alt-7

• the requirement that a listed company have a nominating and governance committee that is composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities;

• the requirement that a listed company have a compensation committee that is composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities; and

• the requirement for an annual performance evaluation of the nominating and governance committee and compensation committee.

Controlled companies must still comply with the exchange’s other corporate governance standards. These include having an audit committee and the special meetings of independent or non-management directors.

Upon completion of this offering and the sale of our Class A Ordinary Shares by the Selling Shareholders pursuant to the Resale Prospectus, the outstanding shares of LIL will consist of 13,150,000 Ordinary Shares, assuming the underwriters do not exercise their over-allotment option to purchase additional Class A Ordinary Shares, or 13,435,000 Ordinary Shares, assuming the over-allotment option is exercised in full. Immediately after completion of this offering, our Controlling Shareholder will own 63.34% of our total issued and outstanding Ordinary Shares, representing 92.05% of the total voting power, assuming that the underwriters do not exercise their over-allotment option, or 62.00% of our total issued and outstanding Ordinary Shares, representing 91.62% of the total voting power, assuming that the over-allotment option is exercised in full. As a result, we will be a “controlled company” as defined under Nasdaq Listing Rule 5615(c) because our Controlling Shareholder will hold more than 50% of the voting power for the election of directors, and our Controlling Shareholder may have the ability to determine matters requiring approval by shareholders. As a “controlled company”, we are permitted to elect not to comply with certain corporate governance requirements. We do not plan to rely on these exemptions, but we may elect to do so after we complete this offering. If we elected to rely on the “controlled company” exemptions, a majority of the members of our board of directors might not be independent directors, our nominating and corporate governance and compensation committees might not consist entirely of independent directors upon closing of the offering, and you would not have the same protection afforded to shareholders of companies that are subject to Nasdaq’s corporate governance rules

IMPACT OF COVID-19

Since late December 2019, the outbreak of COVID-19 spread rapidly throughout China and later to the rest of the world. On January 30, 2020, the International Health Regulations Emergency Committee of the World Health Organization declared the outbreak a “Public Health Emergency of International Concern (PHEIC)”, and later on March 11, 2020 a global pandemic. The COVID-19 outbreak has led governments across the globe to impose a series of measures intended to contain its spread, including border closures, travel bans, quarantine measures, social distancing, and restrictions on business operations and large gatherings. From 2020 to the middle of 2021, COVID-19 vaccination program had been greatly promoted around the globe. While the spread of COVID-19 was substantially controlled in 2021, several types of COVID-19 variants emerged in different parts of the world and restrictions were re-imposed from time to time in certain cities to combat sporadic outbreaks.

The impacts of COVID-19 on our business, financial condition, and results of operations include, but are not limited to, the following:

• the Malaysia Factory was affected by the implementation of the Restriction of Movement Order (the “Order”) announced by the Malaysian government on March 16, 2020. This Order, effective nationwide initially for 2 weeks from March 18, 2020 and the Malaysia Factory was therefore requested to shut down. We had managed to obtain the conditional approval on April 19, 2020 from the Malaysian government to partially resume the operation in the Malaysia Factory subject to certain health precautionary requirements. Nonetheless, under these circumstances the production capacity of the Malaysia Factory is still far behind from its full capacity due to the uncertainty of labor workforce and lower efficiency after implementing the necessary measures to curb against the COVID-19. The Order was later changed to Conditional Movement Control Order (the “CMCO”) on May 4, 2020 and then to Recovery Movement Control Order (the “RMCO”) on June 10, 2020 and the RMCO was extended until the end of 2020. The RMCO caused a disruption on the Malaysia Factory’s operations including delay in receipt of raw material and delivery of finished products and the visit of customers from outside Malaysia.

Alt-8

• The Malaysian government reimposed Full Movement Control Order (the “FMCO”) on May 28, 2021. This FMCO, effective nationwide with total lockdown for 2 weeks from June 1, 2021 and extended to June 28, 2021. On 27 June 2021, the Malaysian government announced that country-wide lockdowns will be extended indefinitely until daily cases fall below 4,000. The Malaysia Factory obtained the conditional approval to continue with partial operation from June 1, 2021, under these circumstances the production capacity of the Malaysia Factory was still far behind from its full capacity. Later on, the Malaysian government introduced National Recovery Plan to help the country emerge from the COVID-19 pandemic and its economic fallout. On September 15, 2021, the Malaysia Factory’s workers vaccination ratio was higher than 80% and were allowed to operate with 100% manpower.

• As of March 2022, Malaysia stood at position 26 as the country with the highest COVID-19 cases as recorded under the coronavirus statistics of the “worldometer”. Total COVID-19 cases in Malaysia hit approximately 3.6 million and associated fatality of 33,228. These figures are huge relative to the small size economy of the country. We are witnessing the adverse impact on the purchasing power of consumers in Malaysia, where our operations are mainly conducted as a direct result of the prolonged pandemic. As such, the extent to which the coronavirus may continue to adversely impact the Malaysian economy is uncertain. In the event that the Malaysian economy suffers, demand for our products may diminish, which would in turn result in adverse impacts on our revenues, cash flows, financial condition and business prospect.

According to WHO, the COVID-19 pandemic “has been on a downward trend” with immunity increasing due to increasing administration of vaccines globally. Whilst there are remaining uncertainties posted by the potential evolution of COVID-19, the WHO Director-General announced on 5 May 2023 that COVID-19 no longer constitutes a PHEIC and is now an established and ongoing health issue, concurring with the advice of the IHR Emergency Committee of the WHO. Notwithstanding such announcement, disruptions like general slowdown in economic conditions globally and volatility in the capital markets posed by COVID-19 are far-reaching and prevalent. The extent to which COVID-19 impacts our operating subsidiary’s business in the future will depend on future developments, which are highly uncertain and cannot be predicted, including new information which may emerge concerning the severity of COVID-19 and the actions to contain COVID-19 or treat its impact, among others. If the disruptions posed by COVID-19 or other matters of global concern continue for an extended period of time, our operating subsidiary’s ability to pursue its business objectives may be materially adversely affected. In addition, our ability to raise equity and debt financing which may be adversely impacted by COVID-19 and other events, including as a result of increased market volatility, decreased market liquidity and third-party financing being unavailable on terms acceptable to us or at all. We will continue to closely monitor the situation throughout 2024 and beyond.

CORPORATE INFORMATION

Our principal executive office is located at Lot A99, Jalan 2A-3, A101 & A102, Jalan 2A, Kawasan Perusahaan MIEL Sungai Lalang, 08000 Sungai Petani, Kedah Darul Aman, Malaysia. Our telephone number is +604-4417802. Our registered office in the BVI is located at Commerce House, Wickhams Cay 1, P.O. Box 3140, Road Town, Tortola, VG 1110, British Virgin Islands. Our website is www.linkers-hk.com. Information contained on, or that can be accessed through, our website is not a part of, and shall not be incorporated by reference into, this prospectus.

Our agent for service of process in the United States is Cogency Global Inc., located at 122 East 42nd Street, 18th Floor, New York, NY 10168.

Alt-9

THE OFFERING(1)

|

Offering Price |

4(2) |

|

|

Number of Class A Ordinary Shares offered by the Selling Shareholders in aggregate |

|

|

|

Number of Ordinary Shares issued and outstanding prior to this offering: |

|

|

|

Number of Ordinary Shares issued and outstanding after this offering: |

13,435,000 Ordinary Shares, including 10,935,000 Class A Ordinary Shares and 2,500,000 Class B Ordinary Shares, assuming full exercise of the underwriters’ over-allotment option |

|

|

Voting Rights |

Class A Ordinary Shares are entitled to one (1) vote per share. Class B Ordinary Shares are entitled to twenty (20) votes per share. |

|

|

Holders of Class A Ordinary Shares and Class B Ordinary Shares will vote together as a single class, unless otherwise required by law or our Memorandum and Articles. The holder of our Class B Ordinary Shares will hold approximately 92.05% of the total votes for our issued and outstanding Shares including 9.61% of the total votes from his Class A Ordinary Shares and 82.44% of the total votes from his Class B Ordinary Shares, following the completion of this Offering, assuming no exercise of the underwriters’ over-allotment option, and will have the ability to control the outcome of matters submitted to our shareholders for approval, including the election of our directors and the approval of any change in control transaction. See the sections titled “Principal Shareholders” and “Description of Share” for additional information. |

||

|

Use of proceeds: |

We will not receive any of the proceeds from the sale of the Ordinary Shares by the Selling Shareholders named in this Resale Prospectus. |

____________

(1) Estimate only. To be finalized at pricing.

(2) Any shares sold by the Selling Shareholders covered by this prospectus will only occur after the commencement of trading of our Ordinary Shares on the Nasdaq Capital Market, and such sales will begin at prevailing market prices or at privately negotiated prices.

Alt-10

ENFORCEMENT OF CIVIL LIABILITIES

We are incorporated under the laws of the BVI with limited liability. We are incorporated in the BVI because of certain benefits associated with being a BVI business company, such as political and economic stability, an effective judicial system, a favorable tax system, the absence of foreign exchange control or currency restrictions and the availability of professional and support services. However, the BVI has a less developed body of securities laws as compared to the United States and provides less protection for investors. In addition, BVI companies may not have standing to sue before the federal courts of the United States.

Substantially all of our assets are located outside the United States. In addition, all of our directors and executive officers are nationals or residents in Malaysia or Hong Kong and substantially all of their assets are located outside the United States. As a result, it may be difficult for you to effect service of process within the United States upon us or these persons, or to enforce judgments obtained in U.S. courts against us or them, including judgments predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States. It may also be difficult for you to enforce judgments obtained in U.S. courts based on the civil liability provisions of the U.S. federal securities laws against us and our executive officers and directors.

We have appointed Cogency Global Inc., as our agent to receive service of process with respect to any action brought against us in the United States in connection with this offering under the federal securities laws of the United States or of any State in the United States.

Enforceability

BVI

Conyers Dill & Pearman, our counsel as to the laws of the BVI, has advised us that there is uncertainty as to whether the courts of the BVI would (i) recognize or enforce judgments of United States courts obtained against us or our directors or officers to impose liabilities predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States; or (ii) entertain original actions brought in the BVI against us or our directors or officers predicated upon the federal securities laws of the United States or the securities law of any state in the United States.

We have been advised by Conyers Dill & Pearman that although there is no statutory enforcement in the BVI of judgments obtained in the federal or state courts of the United States (and the BVI is not a party to any treaties for the reciprocal enforcement or recognition of such judgments), the courts of the BVI would recognize as a valid judgment, a final and conclusive judgment in personam obtained in the federal or state courts in the United States under which a sum of money is payable (other than a sum of money payable in respect of multiple damages, taxes or other charges of a like nature or in respect of a fine or other penalty) and would give a judgment based thereon provided that (a) such courts had proper jurisdiction over the parties subject to such judgment, (b) such courts did not contravene the rules of natural justice of the BVI, (c) such judgment was not obtained by fraud, (d) the enforcement of the judgment would not be contrary to the public policy of the BVI, (e) no new admissible evidence relevant to the action is submitted prior to the rendering of the judgment by the courts of the BVI and (f) there is due compliance with the correct procedures under the laws of the BVI. However, the BVI courts are unlikely to enforce a punitive judgment of a United States court predicated upon the civil liability provisions of the federal securities laws in the United States without retrial on the merits if such judgment is determined by the courts of the BVI to give rise to obligations to make payments that may be regarded as fines, penalties or punitive in nature.

Malaysia

Mah-Kamariyah & Philip Koh, our counsel as to the laws of Malaysia, has advised us that the enforcement of a foreign judgment in Malaysia could be effected through either statutory enforcement or the common law rule of enforcement. Under the Reciprocal Enforcement of Judgments Act 1958 of Malaysia, or REJA, judgments given by superior courts of reciprocating countries, as listed in the First Schedule to the REJA are recognized and may be enforced directly or summarily by way of registration of the judgment provided that such judgments satisfy the requirements as specified under the REJA. Foreign judgments obtained in countries other than the countries listed in

Alt-11

the First Schedule to the REJA, have to be enforced through the common law rule. Although the United States is not a reciprocating country listed in the First Schedule to the REJA, a judgment pronounced in the United States may still be enforced in Malaysia pursuant to Malaysian common law principles provided that such foreign judgments must fulfil certain conditions which includes the following:

(a) the judgment is for a definite sum, and which is final and conclusive;

(b) the original court granting the judgment had jurisdiction in the action;

(c) the judgment was not obtained by fraud;

(d) the proceedings in which the judgment was obtained were not contrary to natural justice; and

(e) the enforcement of the judgment would not be contrary to public policy in Malaysia.

Hong Kong

Hastings & Co., our counsel as to the laws of Hong Kong, has advised us that there is uncertainty as to whether the courts of Hong Kong would (i) recognize or enforce judgments of United States courts obtained against us or our directors or officers predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States or (ii) entertain original actions brought in Hong Kong against us or our directors or officers predicated upon the securities laws of the United States or any state in the United States.

Hong Kong has no arrangement for the reciprocal enforcement of judgments with the United States. As a result, there is uncertainty as to the enforceability in Hong Kong, in original actions or in actions for enforcement, of judgments of United States courts of civil liabilities predicated solely upon the federal securities laws of the United States or the securities laws of any State or territory within the United States.

A judgment of a court in the United States predicated upon U.S. federal or state securities laws may be enforced in Hong Kong at common law by bringing an action in a Hong Kong court on that judgment for the amount due thereunder, and then seeking summary judgment on the strength of the foreign judgment, provided that the foreign judgment, among other things, is (1) for a debt or a definite sum of money (not being taxes or similar charges to a foreign government taxing authority or a fine or other penalty) and (2) final and conclusive on the merits of the claim, but not otherwise. Such a judgment may not, in any event, be so enforced in Hong Kong if (a) it was obtained by fraud; (b) the proceedings in which the judgment was obtained were opposed to natural justice; (c) its enforcement or recognition would be contrary to the public policy of Hong Kong; (d) the court of the United States was not jurisdictionally competent; or (e) the judgment was in conflict with a prior Hong Kong judgment.

Alt-12

USE OF PROCEEDS

We will not receive any of the proceeds from the sale of the Ordinary Shares by the Selling Shareholders.

SELLING SHAREHOLDERS

The following table sets forth the name of the Selling Shareholders, the number of Shares owned by the Selling Shareholders immediately prior to the date of this Resale Prospectus and the number of Shares to be offered by the Selling Shareholders pursuant to this Resale Prospectus. The table also provides information regarding the beneficial ownership of our Shares by the Selling Shareholders as adjusted to reflect the assumed sale of all of the Shares offered under this Resale Prospectus.

The percentage of Ordinary Shares beneficially owned prior to the offering is based on 11,250,000 Ordinary Shares issued and outstanding prior to this offering, as described in “The Offering” section, including the 2,200,000 Ordinary Shares in aggregate that the Selling Shareholders are selling pursuant to this Resale Prospectus. At each general meeting, each shareholder who is present in person or by proxy (or, in the case of a shareholder being a corporation, by its duly authorized representative) will have one vote for each Class A Ordinary Share which such shareholder holds and 20 votes for each Class B Ordinary Share which such shareholder holds. Holders of Class A Ordinary Shares and holders of Class B Ordinary Shares shall vote together as a single class, on all matters that require shareholders’ approval.

We have determined beneficial ownership in accordance with the rules of the SEC. These rules generally attribute beneficial ownership of securities to persons who possess sole or shared voting power or investment power with respect to those securities. The person is also deemed to be a beneficial owner of any security of which that person has a right to acquire beneficial ownership within 60 days. Unless otherwise indicated, the person identified in this table has sole voting and investment power with respect to all shares shown as beneficially owned by him, her or it, subject to applicable community property laws.

|

Name of Selling Shareholder: |

Ordinary Shares |

Maximum number of |

Ordinary Shares |

Approximate |

|||||||||||

|

Class A |

Class B |

Class A |

Class B |

Class A |

Class B |

||||||||||

|

CHIU Hok Yu |

381,375 |

— |

298,375 |

— |

83,000 |

— |

0.62 |

% |

|||||||

|

SIN Lai Yan |

431,375 |

— |

431,375 |

— |

— |

— |

— |

|

|||||||

|

Allied Worldwide Investment Limited(2) |

411,375 |

— |

411,375 |

— |

— |

— |

— |

|

|||||||

|

Apex Infinite Investment Limited(3) |

411,375 |

— |

411,375 |

— |

— |

— |

— |

|

|||||||

|

Billion Track International Limited(4) |

337,500 |

— |

337,500 |

— |

— |

— |

— |

|

|||||||

|

Premier Ace Limited(5) |

310,000 |

— |

310,000 |

— |

— |

— |

— |

|

|||||||

____________

(1) Assumes the sale of our Ordinary Shares by the Selling Shareholders pursuant to the Resale Prospectus filed herewith.

(2) Our Ordinary Shares held by Allied Worldwide Investment Limited are beneficially owned by FOO Chi Ming.

(3) Our Ordinary Shares held by Apex Infinite Investment Limited are beneficially owned by SO Kang Ming.

(4) Our Ordinary Shares held by Billion Track International Limited are beneficially owned by CHEUNG Yuen Ching.

(5) Our Ordinary Shares held by Premier Ace Limited are beneficially owned by TAM Wai Ming.

Lock-up Agreements

The Selling Shareholders, with respect to their Ordinary Shares sold pursuant to the Resale Prospectus in this offering, have not entered into Lock-up Agreement.

Alt-13

SELLING SHAREHOLDERS PLAN OF DISTRIBUTION

The Selling Shareholders and any of their pledgees, donees, assignees and successors-in-interest may, from time to time, sell any or all of their Class A Ordinary Shares being offered under this Resale Prospectus on any stock exchange, market or trading facility on which shares of our Class A Ordinary Shares are traded or in private transactions. No sales of the Class A Ordinary Shares covered by this prospectus shall occur until after completion of our initial public offering. No shares covered by this prospectus will be sold through R.F. Lafferty & Co., Inc. or Revere Securities LLC in our initial public offering, nor will they receive any compensation from the sale of these shares. These sales may be at fixed or negotiated prices. The Selling Shareholders may use any one or more of the following methods when disposing of shares:

• ordinary brokerage transactions and transactions in which the broker-dealer solicits purchasers;

• block trades in which the broker-dealer will attempt to sell the shares as agent but may position; and resell a portion of the block as principal to facilitate the transaction;

• purchases by a broker-dealer as principal and resales by the broker-dealer for its account;

• an exchange distribution in accordance with the rules of the applicable exchange;

• privately negotiated transactions;

• to cover short sales made after the date that the registration statement of which this Resale Prospectus is a part is declared effective by the SEC;

• broker-dealers may agree with the Selling Shareholders to sell a specified number of such shares at a stipulated price per share;

• a combination of any of these methods of sale; and

• any other method permitted pursuant to applicable law.

The shares may also be sold under Rule 144 under the Securities Act of 1933, as amended, if available for the Selling Shareholders, rather than under this Resale Prospectus. The Selling Shareholders have the sole and absolute discretion not to accept any purchase offer or make any sale of shares if they deem the purchase price to be unsatisfactory at any particular time.

The Selling Shareholders may pledge their shares to their brokers under the margin provisions of customer agreements. If the Selling Shareholders defaults on a margin loan, the broker may, from time to time, offer and sell the pledged shares.

Broker-dealers engaged by the Selling Shareholders may arrange for other broker-dealers to participate in sales. Broker-dealers may receive commissions or discounts from the Selling Shareholders (or, if any broker-dealer acts as agent for the purchaser of shares, from the purchaser) in amounts to be negotiated, which commissions as to a particular broker or dealer may be in excess of customary commissions to the extent permitted by applicable law.

If sales of shares offered under this Resale Prospectus are made to broker-dealers as principals, we would be required to file a post-effective amendment to the registration statement of which this Resale Prospectus is a part. In the post-effective amendment, we would be required to disclose the names of any participating broker-dealers and the compensation arrangements relating to such sales, and to include any material information with respect to the plan of distribution not previously disclosed in this Registration Statement or any material change to such information in the Registration Statement.

The Selling Shareholders and any broker-dealers or agents that are involved in selling the shares offered under this Resale Prospectus may be deemed to be “underwriters” within the meaning of the Securities Act in connection with these sales. Commissions received by these broker-dealers or agents and any profit on the resale of the shares purchased by them may be deemed to be underwriting discount under the Securities Act. Any broker-dealers or agents that are deemed to be underwriters may not sell shares offered under this Resale Prospectus unless and until we set forth the names of the underwriters and the material details of their underwriting arrangements in a supplement to this Resale Prospectus or, if required, in a replacement resale prospectus included in a post-effective amendment to the registration statement of which this Resale Prospectus is a part.

Alt-14

The Selling Shareholders and any other persons participating in the sale or distribution of the shares offered under this Resale Prospectus will be subject to applicable provisions of the Exchange Act, and the rules and regulations under that act, including Regulation M. These provisions may restrict activities of, and limit the timing of purchases and sales of any of the shares by, the Selling Shareholders or any other person. Furthermore, under Regulation M, persons engaged in a distribution of securities are prohibited from simultaneously engaging in market making and other activities with respect to those securities for a specified period of time prior to the commencement of such distributions, subject to specified exceptions or exemptions. All of these limitations may affect the marketability of the shares.

Rule 2710 requires members firms to satisfy the filing requirements of Rule 2710 in connection with the resale, on behalf of Selling Shareholders, of the securities on a principal or agency basis. NASD Notice to Members 88-101 states that in the event the Selling Shareholders intends to sell any of the shares registered for resale in this Resale Prospectus through a member of FINRA participating in a distribution of our securities, such member is responsible for insuring that a timely filing, if required, is first made with the Corporate Finance Department of FINRA and disclosing to FINRA the following:

• it intends to take possession of the registered securities or to facilitate the transfer of such certificates;

• the complete details of how the Selling Shareholder’s shares are and will be held, including location of the particular accounts;

• whether the member firm or any direct or indirect affiliates thereof have entered into, will facilitate or otherwise participate in any type of payment transaction with the Selling Shareholders, including details regarding any such transactions; and

• in the event any of the securities offered by the Selling Shareholders are sold, transferred, assigned or hypothecated by any Selling Shareholders in a transaction that directly or indirectly involves a member firm of FINRA or any affiliates thereof, that prior to or at the time of said transaction the member firm will timely file all relevant documents with respect to such transaction(s) with the Corporate Finance Department of FINRA for review.

No FINRA member firm may receive compensation in excess of that allowable under FINRA rules, including Rule 2710, in connection with the resale of the securities by the Selling Shareholders. If any of the ordinary shares offered for sale pursuant to this Resale Prospectus are transferred other than pursuant to a sale under this Resale Prospectus, then subsequent holders could not use this Resale Prospectus until a post-effective amendment or prospectus supplement is filed, naming such holders. We offer no assurance as to whether any of the Selling Shareholders will sell all or any portion of the shares offered under this Resale Prospectus.

We have agreed to pay all fees and expenses we incur incident to the registration of the shares being offered under this Resale Prospectus. However, each of the Selling Shareholders and purchaser is responsible for paying any discount, and similar selling expenses they incur.

We and the Selling Shareholders have agreed to indemnify one another against certain losses, damages and liabilities arising in connection with this Resale Prospectus, including liabilities under the Securities Act.

Alt-15

LEGAL MATTERS

We are being represented by Loeb & Loeb LLP with respect to certain legal matters of U.S. federal securities laws. The validity of our Class A Ordinary Shares offered in this offering and certain other matters of BVI law will be passed upon for us by Conyers Dill & Pearman, our counsel as to BVI law. Legal matters as to Malaysian law will be passed upon for us by Mah-Kamariyah & Philip Koh. Legal matters as to Hong Kong law will be passed upon for us by Hastings & Co. The representative of the underwriters, R.F. Lafferty & Co., Inc., is being represented by VCL Law LLP with respect to certain legal matters of U.S. federal securities laws.

Alt-16

Linkers Industries Limited

2,200,000 Class A Ordinary Shares

––––––––––––––––––––––––––

RESALE PROSPECTUS

––––––––––––––––––––––––––

You should rely only on the information contained in this Resale Prospectus. No dealer, salesperson or other person is authorized to give information that is not contained in this Resale Prospectus. This Resale Prospectus is not an offer to sell nor is it seeking an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. The information contained in this Resale Prospectus is correct only as of the date of this prospectus, regardless of the time of the delivery of this prospectus or the sale of these securities.

Until December 29, 2024, all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriter with respect to their unsold subscriptions.