UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-23915

(Investment Company Act File Number)

(Exact Name of Registrant as Specified in Charter)

321 North Clark Street, Suite 2430

Chicago, IL 60654

(Address of Principal Executive Offices)

Benjamin D. McCulloch, Esq.

XA Investments LLC

321 North Clark Street, Suite 2430

Chicago, IL 60654

(Name and Address of Agent for Service)

(312) 374-6930

(Registrant’s Telephone Number)

Date of Fiscal Year End: September 30

Date

of Reporting Period:

| Item 1. | Reports to Stockholders. |

| (a) |

Octagon XAI CLO Income Fund

SHAREHOLDER LETTER

September 30, 2025 (Unaudited)

Dear Shareholder:

We thank you for your investment in the Octagon XAI CLO Income Fund (the “Fund”). The Fund’s Class I (OCTIX) and A (OCTAX) shares commenced operations on November 4, 2024, and December 2, 2024, respectively. This report covers the fiscal period from October 1, 2024, to September 30, 2025, (the "Period").

During the Period, we observed multiple interest rate cuts by the U.S. Federal Reserve (the “Fed”), signaling that the Fed believes inflation is coming under control. The Consumer Price Index started the Period at 2.4% and ended the period at 3.0%.1 Despite continued economic uncertainty surrounding a weaker labor market, interest rates, and the impact of artificial intelligence, the U.S. economy remained resilient during the Period.

During the Period, the U.S. added approximately 1.2 million jobs, as measured by nonfarm payroll figures through August 2025,2,3 while the August 2025 unemployment rate remained healthy at 4.3%, up slightly from 4.1% at the beginning of the Period.2,4 After a 0.60% decrease in real gross domestic product (“GDP”) growth quarter-over-quarter in Q1 2025, Q2 2025 real GDP increased 3.8% quarter-over-quarter, while the advance estimate for Q3 2025 has been delayed due to the federal government shutdown.2,5

The Fed lowered interest rates three times during the Period for a total decrease of 0.75%. The outcome of the Fed’s monetary easing, its impact on the U.S. economy, and the future path of inflation and employment data should drive subsequent monetary policy action and the level of base interest rates in the U.S. economy. Rate changes will be an important consideration with respect to the Fund, as it invests primarily in floating-rate securities including collateralized loan obligation (“CLO”) debt tranches and CLO equity. Amidst the backdrop of an elevated interest rate environment, the Morningstar LSTA U.S. Leveraged Loan Index (the “Morningstar LLI”) returned 7.93% during the Period.6 Loan performance over the Period was supported by higher reference rates, solid corporate earnings, strong investor demand, and robust capital markets activity. The trailing 12-month default rate for the Morningstar LLI decreased to 1.47% as of September 30, 2025, compared to 0.80% as of September 30, 2024.7

The Fund’s Class I share net asset value (“NAV”) at inception was $25.00. The Fund’s Class I shares NAV ended the Period at $25.00, representing no NAV change from inception to September 30, 2025. This resulted in a NAV total return (including the reinvestment of distributions) of 6.60%. The Fund’s benchmark of 50% ICE BofA US High Yield/50% Morningstar LSTA US Leveraged Loan Index returned 6.93% from November 4, 2024 through September 30, 2025.6

During the Period, the Fund paid its first distribution to shareholders on March 3, 2025. The Fund paid a total of $1.4384 per share in distributions for the Fund’s Class I shares and $1.3844 per share for the Fund’s Class A shares during the Period. As of September 30, 2025 the distribution amount for Class I shares represented an annualized distribution rate of 8.00% based on the Fund’s Class I NAV of $25.00 and the distribution amount for Class A shares represented an annualized distribution rate of 7.66% on the Fund’s Class A NAV of $24.98.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at www.xainvestments.com/OCTIX.

Sincerely,

Kimberly Flynn

President

XA Investments LLC

November 15, 2025

| 1 | Source: U.S. Bureau of Labor Statistics, “12-month percentage change, Consumer Price Index, all items, not seasonally adjusted.” |

| 2 | Full data for the period is not available due to the U.S. Federal government shutdown from October 1, 2025 to November 12, 2025. |

| 3 | Source: U.S. Bureau of Labor Statistics. “All Employees, Total Nonfarm.” |

| 4 | Source: U.S. Bureau of Labor Statistics, “Civilian unemployment rate.” |

| 5 | Source: U.S. Bureau of Labor Statistics, “Gross Domestic Product.” |

| 6 | Source: Bloomberg. See “Index Definitions” in Questions & Answers for additional information). |

| 7 | Source: Pitchbook LCD, LLI Default Rate & Distressed Ratios” (October 1, 2025). |

3

Octagon XAI CLO Income Fund

QUESTIONS & ANSWERS

September 30, 2025 (Unaudited)

What is the Fund’s investment objective and how is it pursued?

The Fund’s investment objective is to provide high income and total return. The Fund seeks to achieve its investment objective by investing at least 80% of its Net Assets, plus the amount of any borrowings used for investment purposes, in securities of collateralized loan obligation entities (“CLOs”), including the debt tranches of CLOs (“CLO Debt”) and subordinated tranches of CLOs (often referred to as the “residual” or “equity” tranche)(“CLO Equity”). CLO Debt and CLO Equity are referred to herein as “CLO Investments”. The Fund does not invest more than 20% of its Managed Assets in CLO Equity. "Managed Assets" means the total assets of the Fund, including assets attributable to the Fund’s use of leverage, minus the sum of its accrued liabilities (other than liabilities incurred for the purpose of creating leverage).

The Fund invests primarily in CLO Investments rated below investment grade (that is, below Baa3- by Moody’s Investor Service (“Moody’s”) or below BBB- by Standard & Poor’s Ratings Services (“S&P”) or Fitch Ratings (“Fitch”) or, if unrated, judged to be of comparable quality by the Fund’s investment sub-adviser). Below investment grade securities are often referred to as “high yield” securities or “junk bonds.”

CLOs are a type of structured credit vehicle that typically invest in a diverse portfolio of broadly syndicated leveraged loans. CLOs finance this pool of loans with a capital structure that consists of debt and equity. CLO Debt includes senior and mezzanine debt (collectively, “liabilities”) of a CLO structure with tranches rated from AAA down to BB or B. Interest earned from the underlying loan collateral pool of a CLO is used to pay the coupon interest on the CLO liabilities. CLO Debt investors earn returns based on spreads above 3-month Term Standard Overnight Financing Rate (“SOFR”). CLO Equity represents a residual stake in the CLO structure and is the first loss position in the event of defaults and credit losses. CLO Equity investors receive the excess spread between the CLO assets and liabilities and expenses. CLO Equity is junior in priority of payment and is subject to certain payment restrictions generally set forth in an indenture governing the notes.

Describe CLO market conditions during the Period, and Octagon’s outlook.

US broadly syndicated loan (“BSL”) CLO Debt tranches generated healthy returns over the 12 months ending September 30, 2025 (the “Period”), ranging from 5.83% for AAA rated tranches to 12.64% for BB rated CLO Debt tranches, as measured by the J.P. Morgan Collateralized Loan Obligation Index (“CLOIE”).1 We observed broad tightening in primary broadly syndicated loan (“BSL”) CLO spreads over the Period, punctuated by periods of volatility. Primary BSL CLO AAA liability spreads for top-tier manager deals compressed to an average SOFR plus 1.30% in the third quarter of 2025, from an average SOFR plus 1.37% in the third quarter of 2024.2 Given the leverage within the CLO structure, a wide or tight AAA spread level can make a significant difference in CLO Equity performance. Farther down the capital stack, BSL CLO BB spreads tightened to an average of SOFR plus 5.25% for deals priced in the third quarter of 2025, compared to an SOFR plus 6.12% average for deals priced in the third quarter of 2024.3

Primary CLO volumes were heavy throughout the Period, notwithstanding a temporary slowdown in market activity as volatility emerged in late-March and into April. All told, $213 billion of new BSL and middle market CLOs priced during the Period.4 Additionally, $109 billion of CLO liabilities were refinanced, and $258 billion of deals were reset.4 Robust new issue and reset volumes coupled with elevated deal call activity (i.e., CLO redemptions) and declining paydowns of post-reinvestment period (“post-RP”) CLO liabilities (also known as amortization), led to improved net CLO supply over the Period.5 CLO AAA net supply was negative in 2024, but has increased over the course of 2025 as the balance of post-RP CLOs has declined.5 As of September 30, 2025, post-RP CLOs accounted for roughly 14% of outstanding CLOs, compared to an estimated 40% as of year-end 2023.5

The growth of CLO Debt-focused ETFs (“CLO ETFs”) persisted in the Period and continued to supplement demand from traditional institutional CLO buyers (i.e., US and Japanese banks, insurance companies, etc.). CLO ETFs reported net inflows of approximately $22 billion during the Period, including $20 billion for investment grade CLO ETFs focused on AAA -A rated tranches (the majority of CLO ETFs are investment grade CLO tranche strategies).6 Several new CLO ETFs launched during the Period, helping to increase total assets under management for CLO ETFs to approximately $38 billion as of September 30, 2025, compared to $16 billion as of September 30, 2024.6 Secondary CLO market liquidity remained steady throughout the Period, notwithstanding an uptick in April driven by increased CLO AAA supply as CLO ETFs sold to meet investor redemptions. We expect secondary trading volumes to remain relatively consistent in the near-term, with activity concentrated at the top of the CLO capital structure as CLO ETFs manage flows.

Considerable spread compression in the loan market remained a headwind for CLO Equity distributions throughout the Period, exacerbated by modest credit losses. For the fiscal year ended September 30, 2025, $720 billion of loans have been repriced.3 Repricing a loan lowers the interest rate a borrower pays to lenders, which reduces the income generated by BSL CLOs. Declining loan spreads can depress CLO equity returns as the excess spread (the arbitrage, i.e., the difference between the spread the CLO receives from its collateral portfolio assets and the spread it pays on its liabilities each quarter) compresses. The median weighted average spread for reinvesting BSL CLOs tightened approximately 0.33% over the Period.6 Meanwhile, the median equity distribution for reinvesting CLOs sequentially declined from 4.0% (of notional) for the third quarter of 2024, to 2.9% for the third quarter of 2025.7 While contracting loan spreads have dragged on CLO Equity distributions this year, elevated CLO reset and refinancing activity has helped to offset a portion of loan collateral portfolios’ reduced coupon income. CLO resets and refinancings of CLO liabilities held by the Fund are generally accretive; not only do CLO resets and refinancings help to mitigate the impact of loan repricings and spread compression, CLO resets can also provide an opportunity to improve collateral portfolio quality (in some instances, before pricing a reset, a CLO manager will sell higher priced CCC loans in an effort to reduce portfolio risk, as capital injections from CLO Equity holders provide cash to rebuild par loss). Furthermore, CLO resets also typically extend the weighted average reinvestment period of the underlying CLO Equity positions in the Fund’s portfolio. Looking ahead, healthy credit fundamentals and tighter CLO liability costs should potentially support optionality value for CLO Equity.

CLO fundamentals remained relatively stable during the Period, despite continued ratings agency downgrade activity and some idiosyncratic credit losses in underlying loan collateral portfolios. The median S&P CCC concentration for reinvesting BSL CLOs declined to under 4% in July and August 2025, then increased to 4.5% as of September 30, 2025—still, the Period-end level compares favorably to the 5.4% median CCC concentration recorded one year prior.6 While junior overcollateralization cushions for reinvesting BSL CLOs remain healthy at a median level of 4.7% as of September 30, 2025,6 we would expect to see widening dispersion as the share of deals with lower overcollateralization cushions increases due to loan downgrades.

We believe that credit fundamentals remain generally sound, though we recognize the potential for idiosyncratic credit situations to emerge across sectors, which underscores the importance of managing downgrade and default risk in underlying loan exposures. Moreover, lower interest rates for corporate borrowers could potentially support more merger and acquisitions activity and bolster new loan supply, which could in turn limit CLO spread tightening and further loan spread loss from repricings.

4

Octagon XAI CLO Income Fund

QUESTIONS & ANSWERS

September 30, 2025 (Continued) (Unaudited)

How did the Fund perform for the Period?

The Fund’s Class I share net asset value (“NAV”) at inception of November 4, 2024 was $25.00. The Fund’s Class I share NAV ended the Period at $25.00, representing no NAV change from inception to September 30, 2025. This resulted in a NAV total return (including the reinvestment of distributions) of 6.60%. The Fund’s benchmark of 50% ICE BofA US High Yield/50% Morningstar LSTA US Leveraged Loan Index returned 6.93% from November 4, 2024 through September 30, 2025.

Relevant indices for the markets in which the Fund invests include the Morningstar LSTA US Leveraged Loan 100 Index (the “Morningstar 100”), which returned 7.93% for the Period, Bloomberg U.S. High Yield 1% Issuer Capped Index, which returned 7.40% for the Period, and the JP Morgan BB/B CLO Debt Index, which returned 13.13% for the Period. There is no representative benchmark index for CLO equity in the marketplace.

What were the distributions over the Period?

During the Period, the Fund paid its first distribution to shareholders on March 3, 2025. The Fund paid a total of $1.4384 per share in distributions for the Fund’s Class I shares and $1.3844 per share for the Fund’s Class A shares during the Period. As of September 30, 2025 the distribution amount for Class I Shares represented an annualized distribution rate of 8.00% based on the Fund’s Class I NAV of $25.00 and the distribution amount for Class A Shares represented an annualized distribution rate of 7.66% on the Fund’s Class A NAV of $24.98.

The Fund intends to pay substantially all of its net investment income, if any, to shareholders through periodic distributions and to distribute any net realized long-term capital gains to shareholders at least annually. The Fund intends to pay monthly distributions to shareholders. However, there is no assurance the Fund will pay regular monthly distributions or that it will do so at a particular rate. The Fund may pay distributions from any permitted source and, from time to time, all or a portion of a distribution may be a return of capital.

Index Definitions

The Fund is actively managed and does not seek to track any index. Index returns are stated for illustrative purposes only, do not reflect the deduction of fees and expenses, and do not represent the performance of the Fund. Past performance is not a predictor of future market performance. It is not possible to invest directly in an index.

The Bloomberg U.S. High Yield 1% Issuer Capped Index measures the performance of high yield bonds, with an individual issuer cap of 1%.

The J.P. Morgan CLO Debt Index represents the post-crisis J.P. Morgan Collateralized Loan Obligation Index (“CLOIE”). The CLOIE is an index that tracks the market for U.S. dollar-denominated broadly syndicated, arbitrage CLOs. The CLOIE is divided by origination (pre- versus post-crisis) and is broken out further into six original rating classes (AAA, AA, A, BBB, BB, B). The sub-index referenced herein tracks BB-rated CLO debt.

The Morningstar LSTA US Leveraged Loan 100 Index (the “Morningstar 100”) is designed to measure the performance of the 100 largest facilities in the US leveraged loan market. Index constituents are market-value weighted, subject to a single loan facility weight cap of 2%.

The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

Risks and Other Considerations

Investing involves risk, including the possible loss of principal and fluctuation in value.

The views expressed in these Questions & Answers reflect those of the portfolio managers only through the report period as stated on the cover. These views are expressed for informational purposes only and are subject to change at any time, based on market and other conditions, and may not come to pass. These views should not be construed as research, investment advice or a recommendation of any kind regarding the Fund or any issuer or security, do not constitute a solicitation to buy or sell any security, and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific investor.

The views expressed in this report may also include forward-looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass. Actual results or events may differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include general economic conditions such as inflation, recession, and interest rates. Neither XAI nor Octagon has any obligation to update or otherwise revise any forward-looking statements, including any revision to reflect changes in any circumstances arising after the date hereof relating to any assumptions or otherwise.

There is no guarantee the Fund’s investment objective will be achieved. CLOs often involve risks that are different from or more acute than risks associated with other types of credit instruments and may be difficult to value or be illiquid. The value of CLOs may decrease if ratings agencies revise their ratings criteria and, as a result, lower the rating of a CLO in which the Fund has invested. The Fund’s shares are not guaranteed or endorsed by any bank or other insured depository institution and are not federally insured by the Federal Deposit Insurance Corporation.

Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted.

Investors should carefully review the prospectus and consider potential risks before investing. These and other risk considerations are described in more detail in the Fund’s prospectus and SAI, each of which can be found on the SEC’s website at www.sec.gov or the Fund’s web page at xainvestments.com/OCTIX.

Paralel Distributors LLC is the distributor for the Fund’s shares. Paralel is not affiliated with XA Investments LLC or Octagon Credit Investors LLC.

5

Octagon XAI CLO Income Fund

QUESTIONS & ANSWERS

September 30, 2025 (Continued) (Unaudited)

| 1 | Source: J.P. Morgan Data Query. Represents the post-crisis J.P. Morgan Collateralized Loan Obligation Index (“CLOIE”). The CLOIE is a benchmark to track the market for US dollar denominated broadly syndicated, arbitrage CLOs. The CLOIE is divided by origination (pre- versus post-crisis) and is broken out further into six original rating classes (AAA, AA, A, BBB, BB, B). It is impossible to invest directly in the index. Past performance is not a predictor of future market performance. |

| 2 | “Top-tier” denotes managers that have issued 20 or more CLOs between 2011 and 2024. Source: Pitchbook LCD, US Credit Markets Quarterly Wrap - Third quarter, 2025 (October 1, 2025). |

| 3 | Source: Pitchbook LCD, US Credit Markets Quarterly Wrap - Third quarter, 2025 (October 1, 2025). |

| 4 | Source: Pitchbook LCD, CLO Global Databank (retrieved from www.lcdcomps.com, October 18, 2025). |

| 5 | Source: BofA Global Research, “CLO Weekly” (October 3, 2025). |

| 6 | Source: BofA Global Research, “CLO Factbook” (October 17, 2025). |

| 7 | Source: BofA Global Research / US Securitized Products Research, “CLO Equity Data” (October 22, 2025). |

6

Octagon XAI CLO Income Fund

PORTFOLIO INFORMATION

September 30, 2025 (Unaudited)

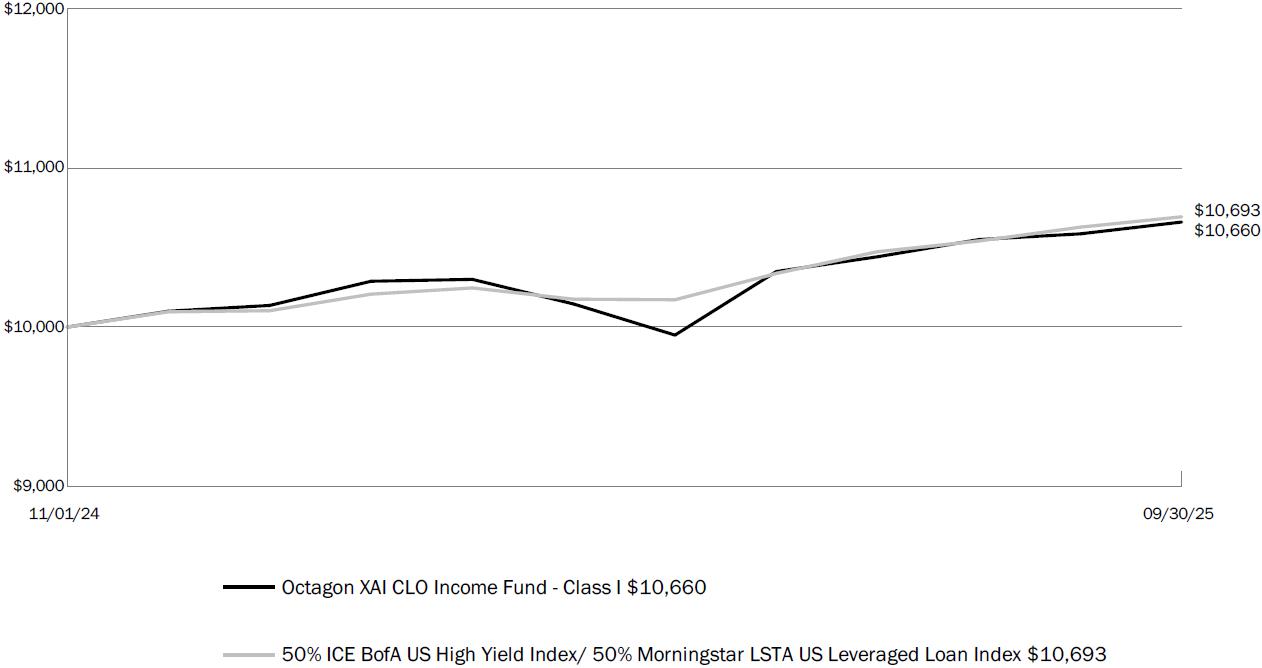

Growth of a $10,000 Investment (as of September 30, 2025)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. Performance reflects the partial waiver of the Fund’s advisory fees and/or reimbursement of expenses for certain periods since the inception date. Without these waivers and/or reimbursements, performance would have been lower. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The chart assumes that distributions from the Fund are reinvested.

Summary Performance (as of September 30, 2025)

| Since | ||||

| Fund/Benchmark | Inception | |||

| Octagon XAI CLO Income Fund - Class I(a) | 6.60 | % | ||

| Octagon XAI CLO Income Fund - Class A(b) | 5.21 | % | ||

| 50% ICE BofA US High Yield Index/50% Morningstar LSTA US Leveraged Loan Index(c) | 6.93 | % | ||

| (a) | Class I inception: November 4, 2024. |

| (b) | Class A inception: December 2, 2024. |

| (c) | The ICE BofA US High Yield Index tracks the performance of US dollar denominated below investment grade rated corporate debt publicly issued in the US domestic market. The Morningstar LSTA US Leveraged Loan Index is a market value weighted index designed to measure the performance of the US leveraged loan market. It is not possible to invest directly in an index. |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than performance data quoted. Please visit our website at www.xainvestments.com/OCTIX to obtain the most recent month-end performance.

7

Octagon XAI CLO Income Fund

PORTFOLIO INFORMATION

September 30, 2025 (Unaudited) (Continued)

Top Ten Portfolio Holdings (as a % of Total Investments)*

| Holding | Type | |||||

| Elmwood CLO 35 Ltd. | Collateralized Loan Obligations Debt | 2.94 | % | |||

| Carlyle US CLO 2019-3 Ltd. | Collateralized Loan Obligations Debt | 2.47 | % | |||

| Sixth Street CLO 28 Ltd. | Collateralized Loan Obligations Debt | 2.46 | % | |||

| CIFC Funding 2019-III Ltd. | Collateralized Loan Obligations Debt | 2.45 | % | |||

| Neuberger Berman Loan Advisers CLO 46 Ltd. | Collateralized Loan Obligations Debt | 2.44 | % | |||

| Sixth Street CLO XXII Ltd. | Collateralized Loan Obligations Debt | 2.44 | % | |||

| Apidos CLO XXXIV | Collateralized Loan Obligations Debt | 2.43 | % | |||

| Generate CLO 19 Ltd. | Collateralized Loan Obligations Debt | 2.35 | % | |||

| Benefit Street Partners CLO XXIX Ltd. | Collateralized Loan Obligations Debt | 2.24 | % | |||

| Barings CLO Ltd. 2024-II | Collateralized Loan Obligations Debt | 1.97 | % | |||

| Total | 24.19 | % | ||||

| * | Holdings may vary, are subject to change, and exclude Money Market Funds. |

| % of Total | ||||

| Asset Allocation* | Investments** | |||

| Collateralized Loan Obligations Debt | 92.46 | % | ||

| Collateralized Loan Obligations Equity | 5.63 | % | ||

| Money Market Funds | 1.90 | % | ||

| * | Holdings may vary and are subject to change. |

| ** | Total may not add up to 100% due to rounding. |

8

Octagon XAI CLO Income Fund

SCHEDULE OF INVESTMENTS

September 30, 2025

| Reference Rate & Spread | Maturity Date | Principal Amount | Value | |||||||||

| COLLATERALIZED LOAN OBLIGATIONS DEBT - 91.63%(a)(b) | ||||||||||||

| AGL CLO 21 Ltd. | 3M SOFR + 5.65% | 10/21/2037 | $ | 500,000 | $ | 502,770 | ||||||

| Anchorage Capital CLO 6 Ltd. | 3M SOFR + 6.15% | 07/22/2038 | 880,000 | 870,414 | ||||||||

| Anchorage Capital CLO 16 Ltd. | 3M SOFR + 5.70% | 01/19/2038 | 500,000 | 494,497 | ||||||||

| Anchorage Capital CLO 21 Ltd. | 3M SOFR + 6.25% | 10/20/2034 | 500,000 | 496,148 | ||||||||

| Anchorage Capital CLO 31 Ltd. | 3M SOFR + 5.70% | 10/20/2038 | 1,000,000 | 1,000,000 | ||||||||

| Apidos CLO XL Ltd. | 3M SOFR + 5.60% | 07/15/2037 | 500,000 | 505,222 | ||||||||

| Apidos CLO XLI Ltd. | 3M SOFR + 5.65% | 10/20/2037 | 685,000 | 695,909 | ||||||||

| Apidos CLO XLVII Ltd. | 3M SOFR + 6.20% | 04/26/2037 | 500,000 | 508,510 | ||||||||

| Apidos CLO XLVIII Ltd. | 3M SOFR + 5.75% | 07/25/2037 | 500,000 | 506,078 | ||||||||

| Apidos CLO XXIII | 3M SOFR + 5.20% | 04/15/2033 | 1,000,000 | 1,000,449 | ||||||||

| Apidos CLO XXXIV | 3M SOFR + 6.76% | 01/20/2035 | 1,250,000 | 1,254,721 | ||||||||

| Apidos CLO XXXV | 3M SOFR + 6.01% | 04/20/2034 | 500,000 | 499,865 | ||||||||

| Ares Loan Funding III Ltd. | 3M SOFR + 6.10% | 07/25/2036 | 500,000 | 500,655 | ||||||||

| Ares XLIV CLO Ltd. | 3M SOFR + 6.25% | 04/15/2034 | 1,000,000 | 1,005,602 | ||||||||

| Bain Capital Credit CLO 2022-3 Ltd. | 3M SOFR + 7.35% | 07/17/2035 | 619,357 | 617,865 | ||||||||

| Barings CLO Ltd. 2021-II | 3M SOFR + 6.51% | 07/15/2034 | 500,000 | 500,314 | ||||||||

| Barings CLO Ltd. 2024-II | 3M SOFR + 5.90% | 07/15/2039 | 1,000,000 | 1,013,343 | ||||||||

| Benefit Street Partners CLO XVII Ltd. | 3M SOFR + 6.15% | 10/15/2037 | 750,000 | 758,345 | ||||||||

| Benefit Street Partners CLO XXIX Ltd. | 3M SOFR + 4.60% | 01/25/2038 | 1,150,000 | 1,153,368 | ||||||||

| Canyon CLO 2021-3 Ltd. | 3M SOFR + 6.00% | 07/15/2034 | 500,000 | 499,986 | ||||||||

| Carlyle US CLO 2017-2 Ltd. | 3M SOFR + 7.56% | 07/20/2037 | 750,000 | 763,945 | ||||||||

| Carlyle US CLO 2019-3 Ltd. | 3M SOFR + 7.34% | 04/20/2037 | 1,250,000 | 1,273,005 | ||||||||

| Carlyle US CLO 2024-2 Ltd. | 3M SOFR + 6.85% | 04/25/2037 | 500,000 | 508,711 | ||||||||

| Cayuga Park CLO Ltd. | 3M SOFR + 6.26% | 07/17/2034 | 500,000 | 501,127 | ||||||||

| CBAM 2018-8 Ltd. | 3M SOFR + 6.37% | 07/15/2037 | 750,000 | 758,834 | ||||||||

| CIFC Funding 2019-I Ltd. | 3M SOFR + 5.75% | 10/20/2037 | 500,000 | 507,360 | ||||||||

| CIFC Funding 2019-III Ltd. | 3M SOFR + 5.00% | 01/16/2038 | 1,250,000 | 1,261,045 | ||||||||

| CIFC Funding 2021-2 Ltd. | 3M SOFR + 6.46% | 04/15/2034 | 500,000 | 500,915 | ||||||||

| CIFC Funding 2021-V Ltd. | 3M SOFR + 5.10% | 01/15/2038 | 450,000 | 453,451 | ||||||||

| Dryden 87 CLO Ltd. | 3M SOFR + 6.35% | 08/20/2038 | 1,000,000 | 1,008,694 | ||||||||

| Elmwood CLO 27 Ltd. | 3M SOFR + 6.25% | 04/18/2037 | 660,000 | 668,587 | ||||||||

| Elmwood CLO 35 Ltd. | 3M SOFR + 5.25% | 10/18/2037 | 1,500,000 | 1,516,846 | ||||||||

| Garnet CLO 2 Ltd. | 3M SOFR + 5.25% | 10/20/2038 | 415,000 | 417,997 | ||||||||

| Generate CLO 6 Ltd. | 3M SOFR + 7.25% | 10/22/2037 | 1,000,000 | 1,003,388 | ||||||||

| Generate CLO 19 Ltd. | 3M SOFR + 6.00% | 04/22/2036 | 1,200,000 | 1,211,444 | ||||||||

| GoldenTree Loan Management US CLO 25 Ltd. | 3M SOFR + 5.75% | 04/20/2038 | 750,000 | 764,748 | ||||||||

| Lakeside Park CLO Ltd. | 3M SOFR + 4.60% | 04/15/2038 | 1,000,000 | 1,003,544 | ||||||||

| Lodi Park CLO Ltd. | 3M SOFR + 5.65% | 07/21/2037 | 1,000,000 | 1,012,791 | ||||||||

| Madison Park Funding XXVIII Ltd. | 3M SOFR + 6.35% | 01/15/2038 | 1,000,000 | 1,004,694 | ||||||||

| Meacham Park CLO Ltd. | 3M SOFR + 5.35% | 10/20/2037 | 750,000 | 757,580 | ||||||||

| Neuberger Berman Loan Advisers CLO 46 Ltd. | 3M SOFR + 5.15% | 01/20/2037 | 1,250,000 | 1,256,559 | ||||||||

| NYACK Park CLO Ltd. | 3M SOFR + 6.36% | 10/20/2034 | 980,000 | 980,101 | ||||||||

| Oaktree CLO 2024-27 Ltd. | 3M SOFR + 5.60% | 10/22/2037 | 500,000 | 507,447 | ||||||||

| OCP CLO 2016-12 Ltd. | 3M SOFR + 6.00% | 10/18/2037 | 1,000,000 | 1,013,336 | ||||||||

| OCP CLO 2017-13 Ltd. | 3M SOFR + 5.90% | 11/26/2037 | 1,000,000 | 1,000,943 | ||||||||

| OCP CLO 2019-17 Ltd. | 3M SOFR + 6.25% | 07/20/2037 | 1,000,000 | 1,010,504 | ||||||||

| OCP CLO 2022-25 Ltd. | 3M SOFR + 5.85% | 07/20/2037 | 500,000 | 503,577 | ||||||||

| OHA Credit Funding 12-R Ltd. | 3M SOFR + 4.85% | 07/20/2037 | 750,000 | 753,451 | ||||||||

| OHA Credit Partners VII Ltd. | 3M SOFR + 4.50% | 02/20/2038 | 1,000,000 | 997,718 | ||||||||

| OHA Credit Partners XVII Ltd. | 3M SOFR + 5.00% | 01/18/2038 | 1,000,000 | 1,008,268 | ||||||||

| OHA Loan Funding 2015-1 Ltd. | 3M SOFR + 4.80% | 10/19/2038 | 750,000 | 749,980 | ||||||||

| Rad CLO 3 Ltd. | 3M SOFR + 5.88% | 07/15/2037 | 500,000 | 484,702 | ||||||||

| Rad CLO 10 Ltd. | 3M SOFR + 6.11% | 04/23/2034 | 457,240 | 452,744 | ||||||||

| Regatta XII Funding Ltd. | 3M SOFR + 6.90% | 10/15/2037 | 500,000 | 505,310 | ||||||||

| Regatta XXVIII Funding Ltd. | 3M SOFR + 6.85% | 04/25/2037 | 500,000 | 508,682 | ||||||||

| Shackleton 2019-XIV CLO Ltd. | 3M SOFR + 5.90% | 07/20/2034 | 555,000 | 546,660 | ||||||||

| Sixth Street CLO 28 Ltd. | 3M SOFR + 5.45% | 04/21/2038 | 1,250,000 | 1,270,480 | ||||||||

| Sixth Street CLO XXII Ltd. | 3M SOFR + 4.75% | 04/21/2038 | 1,250,000 | 1,258,482 | ||||||||

| Sixth Street CLO XXIV Ltd. | 3M SOFR + 6.65% | 04/23/2037 | 800,000 | 811,132 | ||||||||

| Voya CLO 2024-7 Ltd. | 3M SOFR + 5.25% | 01/20/2038 | 750,000 | 757,852 | ||||||||

| TOTAL COLLATERALIZED LOAN OBLIGATIONS DEBT (Cost $47,578,913) | $47,660,695 | |||||||||||

See Notes to Financial Statements.

9

Octagon XAI CLO Income Fund

SCHEDULE OF INVESTMENTS

September 30, 2025 (Continued)

| Estimated Yield | Maturity Date | Principal Amount | Value | |||||||||

| COLLATERALIZED LOAN OBLIGATIONS EQUITY - 5.59 %(a)(c) | ||||||||||||

| Benefit Street Partners CLO XII-B Ltd. | 15.49% | 10/15/2030 | $ | 500,000 | $ | 406,600 | ||||||

| CIFC Funding 2018-II Ltd. | 16.31% | 10/20/2037 | 1,250,000 | 512,969 | ||||||||

| Neuberger Berman CLO XXI Ltd. | 13.63% | 01/20/2039 | 1,400,000 | 929,054 | ||||||||

| OCP CLO 2024-36, Ltd. | 12.13% | 10/16/2037 | 1,000,000 | 738,000 | ||||||||

| Regatta XIX Funding Ltd. | 12.38% | 04/20/2035 | 500,000 | 317,910 | ||||||||

| TOTAL COLLATERALIZED LOAN OBLIGATIONS EQUITY (Cost $3,235,223) | $2,904,533 | |||||||||||

| Shares | Value | |||||||

| MONEY MARKET FUNDS - 1.88% | ||||||||

| Invesco Short Term Investments Trust Treasury Portfolio, Institutional Class, 3.99% (7-day yield) | 979,912 | 979,912 | ||||||

| TOTAL MONEY MARKET FUNDS (Cost $979,912) | $979,912 | |||||||

| TOTAL INVESTMENTS - 99.10% (Cost $51,794,048) | 51,545,140 | |||||||

| Other Assets in Excess of Liabilities - 0.90% | 466,835 | |||||||

| NET ASSETS - 100.00% | $ | 52,011,975 | ||||||

| (a) | All or a portion of the security is exempt from registration of the Securities Act of 1933. These securities may be resold in transactions exempt from registration under Rule 144A, normally to qualified institutional buyers. As of September 30, 2025, these securities had an aggregate value of $50,565,228 or 97.22% of net assets. |

| (b) | Variable rate investment. Interest rates reset periodically. Interest rate shown reflects the rate in effect at September 30, 2025. For securities based on a published reference rate and spread, the reference rate and spread are indicated in the description above. Leveraged loans and CLO debt securities typically have reference Rate Floors (“Rate Floors”) embedded in their loan agreements and organizational documents. Leveraged loans generally have Rate Floors of 0% or more, while CLO debt securities often set Rate Floors at 0%. Rate Floors serve to establish a minimum base rate to be paid by the borrower before the fixed spread. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| (c) | CLO subordinated notes, income notes, Y notes and M notes are considered CLO equity positions. CLO equity positions are entitled to recurring distributions which are generally equal to the remaining cash flow of payments made by underlying securities less contractual payments to debt holders and fund expenses. The effective yield is estimated based upon the amount and timing of these recurring distributions in addition to the estimated amount of terminal principal payment. Effective yields for the CLO equity positions are updated generally once per quarter or on a transaction such as an add-on purchase, refinancing or reset. The estimated yield and investment cost may ultimately not be realized. Estimated yields shown are as of September 30, 2025. |

Investment Abbreviations:

Ltd. – Limited

SOFR – Secured Overnight Financing Rate

Reference Rates:

3M SOFR as of September 30, 2025 was 4.37%.

See Notes to Financial Statements.

10

Octagon XAI CLO Income Fund

| STATEMENT OF ASSETS AND LIABILITIES | ||

| September 30, 2025 |

| ASSETS: | ||||

| Investments, at value (Cost $51,794,048) | $ | 51,545,140 | ||

| Receivable for fund shares sold | 1,020,024 | |||

| Interest receivable | 999,177 | |||

| Receivable for investment securities sold | 107,092 | |||

| Prepaid expenses and other assets | 16,766 | |||

| Total Assets | 53,688,199 | |||

| LIABILITIES: | ||||

| Payable for investment securities purchased | 1,106,850 | |||

| Distributions payable to common shareholders | 336,884 | |||

| Accrued investment advisory fees payable (Note 3) | 96,354 | |||

| Accrued professional fees payable | 73,476 | |||

| Accrued fund accounting and administration fees payable | 27,036 | |||

| Accrued transfer agent fees payable | 8,473 | |||

| Accrued custodian fees payable | 6,273 | |||

| Accrued printing fees payable | 3,421 | |||

| Accrued distribution and servicing fees payable (Note 3) | 3,149 | |||

| Accrued trustees' fees and expenses payable | 1,291 | |||

| Other payable and accrued expenses | 13,017 | |||

| Total Liabilities | 1,676,224 | |||

| NET ASSETS | $ | 52,011,975 | ||

| COMPOSITION OF NET ASSETS: | ||||

| Paid in capital | $ | 52,300,460 | ||

| Distributable earnings/(Accumulated loss) | (288,485 | ) | ||

| NET ASSETS | $ | 52,011,975 | ||

| PRICING OF SHARES | ||||

| Class I: | ||||

| Offering price and net asset value per share of beneficial interest | $ | 25.00 | ||

| Net Assets applicable to common shareholders | $ | 40,833,493 | ||

| Shares of beneficial interest outstanding, at $0.01 par value per share, and unlimited common shares authorized | 1,633,113 | |||

| Class A: | ||||

| Net asset value per share of beneficial interest | $ | 24.98 | ||

| Maximum offering price per share(a) | $ | 25.44 | ||

| Net Assets applicable to common shareholders | $ | 11,178,482 | ||

| Shares of beneficial interest outstanding, at $0.01 par value per share, and unlimited common shares authorized | 447,500 | |||

| (a) | Includes maximum sales charge of 2.00%. |

See Notes to Financial Statements.

11

Octagon XAI CLO Income Fund

| STATEMENT OF OPERATIONS | ||

| For the Period Ended September 30, 2025* |

| INVESTMENT INCOME: | ||||

| Interest and other income | $ | 3,029,408 | ||

| Total Investment Income | 3,029,408 | |||

| EXPENSES: | ||||

| Investment advisory fees (Note 3) | 423,010 | |||

| Class A distribution and servicing fees (Note 4) | 42,282 | |||

| Fund accounting and administration fees | 159,882 | |||

| Professional fees | 128,757 | |||

| Transfer agent fees | 65,304 | |||

| Principal financial officer fees (Note 3) | 54,333 | |||

| Chief compliance officer fees (Note 3) | 31,694 | |||

| Printing expenses | 18,837 | |||

| Registration and filing fees | 18,598 | |||

| Custodian fees | 10,426 | |||

| Trustees' fees and expenses | 9,364 | |||

| Excise tax | 4,309 | |||

| Other expenses | 19,890 | |||

| Total Expenses | 986,686 | |||

| Less expenses waived from Investment Advisor (Note 3) | ||||

| Class I | (288,177 | ) | ||

| Class A | (33,049 | ) | ||

| Less distribution and servicing fees reimbursed (Note 4) | ||||

| Class A | (24,990 | ) | ||

| Net Expenses | 640,470 | |||

| NET INVESTMENT INCOME | 2,388,938 | |||

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | ||||

| Net realized loss on: | ||||

| Investment securities | (67,645 | ) | ||

| Total net realized loss | (67,645 | ) | ||

| Net change in unrealized appreciation/depreciation on: | ||||

| Investment securities | (248,908) | |||

| Net change in unrealized appreciation/depreciation | (248,908 | ) | ||

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | (316,553 | ) | ||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 2,072,385 | ||

| * | Reflects operations for the period from November 4, 2024 (commencement of Fund operations) to September 30, 2025. Prior to the commencement of Fund operations, the Fund had been inactive except for matters related to the Fund’s registration and establishment. |

See Notes to Financial Statements.

12

Octagon XAI CLO Income Fund

STATEMENT OF CHANGES IN NET ASSETS

| For the Period | ||||

| Ended September 30, | ||||

| 2025(a) | ||||

| OPERATIONS: | ||||

| Net investment income | $ | 2,388,938 | ||

| Net realized loss | (67,645 | ) | ||

| Net change in unrealized appreciation/depreciation | (248,908 | ) | ||

| Net increase in net assets from operations | 2,072,385 | |||

| DISTRIBUTIONS: | ||||

| From distributable earnings | ||||

| Class I | (1,900,707 | ) | ||

| Class A | (464,472 | ) | ||

| From tax return of capital | ||||

| Class I | (84,465 | ) | ||

| Class A | (20,641 | ) | ||

| Total distributions | (2,470,285 | ) | ||

| SHARE TRANSACTIONS: | ||||

| Shares sold | ||||

| Class I | 40,572,991 | |||

| Class A | 11,113,500 | |||

| Distributions reinvested | ||||

| Class I | 393,658 | |||

| Class A | 229,926 | |||

| Shares repurchased | ||||

| Class I | (200 | ) | ||

| Net increase in net assets from share transactions | 52,309,875 | |||

| Net increase in net assets | 51,911,975 | |||

| NET ASSETS | ||||

| Beginning of period | 100,000 | |||

| End of period | $ | 52,011,975 | ||

| * | Reflects operations for the period from November 4, 2024 (commencement of Fund operations) to September 30, 2025. Prior to the commencement of Fund operations, the Fund had been inactive except for matters related to the Fund’s registration and establishment. |

See Notes to Financial Statements.

13

Octagon XAI CLO Income Fund

FINANCIAL HIGHLIGHTS

For a Share Class throughout the Period Presented

| For the Period | | |||

| Ended | | |||

| September 30, | | |||

| Class I | 2025(a) | | ||

| Net Asset Value - Beginning of Period | $ | 25.00 | (b) | |

| INCOME FROM INVESTMENT OPERATIONS: | | |||

| Net investment income(c) | 1.93 | | ||

| Net realized and unrealized loss on investments | (0.32 | ) | ||

| Total Income/(Loss) from Investment Operations | 1.61 | | ||

| DISTRIBUTIONS: | | |||

| From distributable earnings | (1.54 | ) | ||

| Tax return of capital | (0.07 | ) | ||

| Total Distributions | (1.61 | ) | ||

| | ||||

| Net Asset Value - End of Period | $ | | ||

| Total Investment Return - Net Asset Value(d) | 6.60 | % | ||

| RATIOS/SUPPLEMENTAL DATA: | | |||

| Net assets, end of period (000s) | $ | 40,833 | | |

| Ratio of expenses excluding waivers to average net assets | 3.43 | %(e)(f) | ||

| Ratio of expenses including waivers to average net assets | 2.18 | %(e)(g) | ||

| Ratio of net investment income excluding waivers to average net assets | 7.24 | %(e)(f) | ||

| Ratio of net investment income including waivers to average net assets | 8.49 | %(e)(g) | ||

| Portfolio turnover rate | 14 | % | ||

| (a) | Reflects operations for the period from November 4, 2024 (commencement of Fund operations) to September 30, 2025. Prior to the commencement of Fund operations, the Fund had been inactive except for matters related to the Fund’s registration and establishment. |

| (b) | The net asset value at the beginning of the period represents the registration and initial sale of Class I shares on January 18, 2024. There were no operations other than that initial sale prior to November 4, 2024 (Commencement of Operations). |

| (c) | Calculated based on the average number of common shares outstanding. |

| (d) | Total investment return is calculated assuming an investment made at the net asset value at the beginning of the period and reinvestment of all distributions. Total investment return includes the Fund's operating expense cap and fee waiver, as applicable. Total investment return does not reflect brokerage commissions, if any, and are not annualized. |

| (e) | Annualized. |

| (f) | Differences in annualized operating expenses among share classes is due to different share class inception dates and share class specific expenses. |

| (g) | Reflects the waiver of investment advisory fees per the Operating Expense Limitation Agreement (see Note 3). Differences in annualized operating expenses among share classes is due to different share class inception dates and share class specific expenses. |

See Notes to Financial Statements.

14

Octagon XAI CLO Income Fund

FINANCIAL HIGHLIGHTS

For a Share Class throughout the Period Presented (Continued)

| For the Period | ||||

| Ended | ||||

| September 30, | ||||

| Class A | 2025(a) | |||

| Net Asset Value - Beginning of Period | $ | 25.25 | ||

| INCOME FROM INVESTMENT OPERATIONS: | ||||

| Net investment income(b) | 1.68 | |||

| Net realized and unrealized loss on investments | (0.41 | ) | ||

| Total Income/(Loss) from Investment Operations | 1.27 | |||

| DISTRIBUTIONS: | ||||

| From distributable earnings | (1.47 | ) | ||

| Tax return of capital | (0.07 | ) | ||

| Total Distributions | (1.54 | ) | ||

| Net Asset Value - End of Period | $ | |||

| Total Investment Return - Net Asset Value(c) | 5.21 | % | ||

| RATIOS/SUPPLEMENTAL DATA: | ||||

| Net assets, end of period (000s) | $ | 11,178 | ||

| Ratio of expenses excluding waivers to average net assets | 3.71 | %(d)(e) | ||

| Ratio of expenses including waivers to average net assets | 2.53 | %(d)(f) | ||

| Ratio of net investment income excluding waivers to average net assets | 6.96 | %(d)(e) | ||

| Ratio of net investment income including waivers to average net assets | 8.14 | %(d)(f) | ||

| Portfolio turnover rate | 14 | % | ||

| (a) | Reflects operations for the period from December 2, 2024 (inception of Class A Shares) to September 30, 2025. |

| (b) | Calculated based on the average number of common shares outstanding. |

| (c) | Total investment return is calculated assuming an investment made at the net asset value at the beginning of the period and reinvestment of all distributions and does not include maximum sales charge. Total investment return includes the Fund's operating expense cap and fee waiver, as applicable. Total investment return does not reflect brokerage commissions, if any, and are not annualized. |

| (d) | Annualized. |

| (e) | Differences in annualized operating expenses among share classes is due to different share class inception dates and share class specific expenses. |

| (f) | Reflects the waiver of investment advisory fees per the Operating Expense Limitation Agreement (see Note 3) and the reimbursement of distribution and/or shareholder servicing fees (see Note 4). Differences in annualized operating expenses among share classes is due to different share class inception dates and share class specific expenses. |

See Notes to Financial Statements.

15

Octagon XAI CLO Income Fund

NOTES TO FINANCIAL STATEMENTS

September 30, 2025

NOTE 1 - ORGANIZATION

Octagon XAI CLO Income Fund (the “Fund”) was organized on November 13, 2023, as a Delaware Statutory Trust and is registered with the Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified, closed-end management investment company that operates as an “interval fund.” The Fund continuously offers common shares of beneficial interest (the “Shares”) under Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”). The Fund has adopted a fundamental policy to make a quarterly repurchase offer (“Repurchase Offer”) of between 5% and 25% of the Fund’s outstanding Shares.

The Fund’s investment objective is to provide high income and total return. Under normal market conditions, the Fund will invest at least 80% of its managed assets in securities of collateralized loan obligation entities (“CLOs”), including the debt tranches of CLOs (“CLO Debt”) and subordinated tranches of CLOs (often referred to as the “residual” or “equity” tranche) (“CLO Equity”). “Managed Assets” means the total assets of the Fund, including assets attributable to the Fund’s use of leverage, minus the sum of its accrued liabilities (other than liabilities incurred for the purpose of creating leverage). The Fund will purchase CLO investments in the primary and secondary markets.

The Fund offers, on a continuous basis, two classes of common shares of beneficial interest: Class I Shares and Class A Shares. The Fund has received exemptive relief from the SEC which permits the Fund to, among other things, issue multiple classes of shares, impose on certain of the classes a sales charge or an early withdrawal charge and schedule waivers of such, and impose class specific annual asset-based distribution and/or shareholder service fees on the assets of the various classes of shares to be used to pay for expenses incurred in fostering the distribution and/or shareholder servicing of shares of the particular class. Class I commenced operations on November 4, 2024 and Class A commenced operations on December 2, 2024. The Fund had no operations prior to November 4, 2024, other than matters relating to its registration and initial sale of 4,000 Class I Shares of the Fund to XA Investments LLC ("XAI" or the Adviser"), which represented the initial capital of $100,000 at $25.00 per share.

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Accounting and Use of Estimates – The financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”), which requires management to make estimates and assumptions that affect the reported amounts and disclosures, including contingent assets and liabilities, in the financial statements during the period reported. Management believes the estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the Fund ultimately realizes upon sale of the securities. The Fund is considered an investment company under U.S. GAAP and follows the accounting and reporting guidance applicable to investment companies in the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946. The financial statements have been prepared as of the close of the New York Stock Exchange (“NYSE”) on September 30, 2025.

Expense Recognition – Expenses are recorded on the accrual basis of accounting.

Calculation of Net Asset Value – The calculation of net asset value ("NAV") per common share of each class of shares is determined daily, on each day that the NYSE is open for trading, as of the close of regular trading on the NYSE (normally 4:00 p.m. Eastern Time). The Fund’s NAV per common share for each class of shares is calculated separately based on the fees and expenses applicable to each class of shares and by dividing the share class’s proportionate value of the Fund’s total assets, less its liabilities, by the number of share class’s common shares outstanding.

Cash– The Fund considers its investment in an FDIC insured interest bearing account to be cash. The Fund maintains cash balances, which at times may exceed federally insured limits. The Fund maintains these balances with a high quality financial institution. The Fund monitors this credit risk and has not experienced any losses related to this risk.

Securities- Transactions and Investment Income – Investment security transactions are accounted for on a trade date basis. Dividend income is recorded on the ex dividend date. Realized gains and losses from securities transactions and unrealized appreciation and depreciation of securities are determined using the identified cost basis method for financial reporting purposes.

Interest income from investments is recorded using the accrual basis of accounting to the extent such amounts are expected to be collected. Amortization of premium or accretion of discount is recognized using the effective interest method, which is included in interest income. Collateralized loan obligation (“CLO”) equity investments recognize investment income on the accrual basis utilizing an effective interest methodology based upon an effective yield to maturity utilizing projected cash flows. ASC Topic 325-40, Beneficial Interests in Securitized Financial Assets, requires investment income from CLO equity investments and fee rebates to be recognized under the effective interest method, with any difference between the cash distribution and the amount calculated pursuant to the effective interest method being recorded as an adjustment to the cost basis of the investment. There were no fee rebates for CLO equity investments held by the Fund as of September 30, 2025.

Effective yields for the Fund’s CLO equity positions are monitored and evaluated on a quarterly basis. The Fund also updates a CLO equity investment’s effective yield in each instance where there is a respective add-on purchase, refinancing or reset involving the CLO equity investment held. The effective yield will be set to 0.00% if: (1) the aggregate projected amount of future recurring distributions is less than the amortized investment cost, and/or (2) there is significant uncertainty with respect to the timing of future residual distributions from equity positions that are in the process of being redeemed or that have missed or are not currently making distributions. The future distributions for CLO equity positions with a 0.00% effective yield will be recognized solely as return of cost basis until the aggregate projected amount of future recurring distributions exceeds the amortized investment cost.

Adopted Accounting Standards – In this reporting period, the Fund adopted FASB Accounting Standards Update 2023-07, Segment Reporting (“Topic 280”) – Improvements to Reportable Segment Disclosures (“ASU 2023-07”), which requires a public entity to make enhanced disclosures about significant segment expenses that are regularly provided to the chief operating decision maker (the “CODM”). The Fund’s Secretary and Chief Legal Officer acts as the CODM. Adoption of the new standard impacted financial statement disclosures only and did not affect the Fund’s financial position or the results of its operations. The Fund represents a single operating segment, as the CODM monitors the operating results of the Fund as a whole and the Fund’s long-term strategic asset allocation is pre-determined in accordance with the terms of its prospectus, based on a defined investment strategy which is executed by the Fund’s portfolio managers as a team. The financial information in the form of the Fund’s portfolio composition, total returns, expense ratios and changes in net assets resulting from operations, which are used by the CODM to assess the segment’s performance versus the Fund’s comparative benchmarks and to make resource allocation decisions for the Fund’s single segment, is consistent with that presented within the Fund’s financial statements. Segment assets are reflected on the accompanying Statement of Assets and Liabilities and significant segment expenses are listed on the accompanying Statement of Operations.

16

Octagon XAI CLO Income Fund

NOTES TO FINANCIAL STATEMENTS

September 30, 2025 (Continued)

Fair Value Measurements – The Fund records investments at fair value. The Fund values debt securities at the last available- bid price for such securities or,- if such prices are not available, at prices for securities of comparable maturity, quality, and type. The Fund values exchange traded options and other exchange traded derivative contracts at the midpoint of the best bid and asked prices at the close on those exchanges on which they are traded.

The Fund values equity securities at the last reported sale price on the principal exchange or in the principal off-exchange market in which such securities are traded, as of the close of regular trading on the NYSE on the day the securities are being valued or, if there are no sales, at the mean between the last available bid and asked prices on that day. Securities traded primarily on the Nasdaq Stock Market (“Nasdaq”) are normally valued by the Fund at the Nasdaq Official Closing Price (“NOCP”) provided by Nasdaq each business day. The NOCP is the most recently reported price as of 4:00 p.m., Eastern Time, unless that price is outside the range of the “inside” bid and asked prices (i.e., the bid and asked prices that dealers quote to each other when trading for their own accounts); in that case, Nasdaq will adjust the price to equal the inside bid or asked price, whichever is closer. Because of delays in reporting trades, the NOCP may not be based on the price of the last trade to occur before the market closes.

Generally, trading in many foreign securities will be substantially completed each day at various times prior to the close of the NYSE. The values of these securities used in determining the net asset value generally will be computed as of such times. Occasionally, events affecting the value of foreign securities may occur between such times and the close of the NYSE which will not be reflected in the computation of net asset value unless it is determined that such events would materially affect the net asset value, in which case adjustments would be made and reflected in such computation pursuant to the fair valuation procedures described herein. Such adjustments may be based upon factors such as developments in non-U.S. markets, the performance of U.S. securities markets and the performance of instruments trading in U.S. markets that represent non-U.S. securities.

Short-term securities with remaining maturities of less than 60 days may be valued at amortized cost, to the extent that amortized cost is determined to approximate fair value. Investments in open-end investment companies, including money market Funds, are valued at their net asset value at the end of each business day. These valuations are typically categorized as Level 1 in the fair value hierarchy.

The Fund values derivatives transactions in accordance with valuation guidelines adopted by the Board of Trustees of the Fund (the “Board of Trustees”). Accrued payments to the Fund under such transactions will be assets of the Fund and accrued payments by the Fund will be liabilities of the Fund.

The Fund may utilize bid quotations provided by independent pricing services or, if independent pricing services are unavailable, dealers to value certain of its securities and other instruments at their market value. The Fund may use independent pricing services to value certain securities held by the Fund at their market value. The Fund periodically verifies valuations provided by independent pricing services.

If independent pricing services or dealer quotations are not available for a given security, such security will be valued in accordance with valuation guidelines adopted by the Board of Trustees that the Board of Trustees believes are designed to accurately reflect the fair value of securities valued in accordance with such guidelines.

The Board of Trustees has designated XAI as the “valuation designee” for the Fund pursuant to Rule 2a-5 under the Investment Company Act. The valuation designee is responsible for making fair value determinations pursuant to Valuation Policies and Procedures adopted by XAI and the Fund (the “Valuation Policy”). A committee of voting members comprised of senior personnel of XAI considers various pricing issues and establishes fair valuations of portfolio securities and other instruments held by the Fund in accordance with the Valuation Policy (the “Pricing Committee”). XAI as valuation designee is subject to monitoring and oversight by the Board of Trustees. As a general principle, the fair value of a portfolio instrument is the amount that an owner might reasonably expect to receive upon the instrument’s current sale. A range of factors and analysis may be considered when determining fair value, including relevant market data, interest rates, credit considerations and/or issuer specific news. The Pricing Committee may consult with and receive input from third parties, such as the Sub-Adviser, and will utilize a variety of market data including yields or prices of investments of comparable quality, type of issue, coupon, maturity, rating, indications of value from security dealers, evaluations of anticipated cash flows or collateral, spread over U.S. Treasury obligations, and other information and analysis. In addition, the Pricing Committee may consider valuations provided by valuation firms retained to assist in the valuation of certain of the Fund’s investments. Fair valuation involves subjective judgments. While the Fund’s use of fair valuation is intended to result in calculation of net asset value that fairly reflects values of the Fund’s portfolio securities as of the time of pricing, the Fund cannot guarantee that any fair valuation will, in fact, approximate the amount the Fund would actually realize upon the sale of the securities in question. It is possible that the fair value determined for a portfolio instrument may be materially different from the value that could be realized upon the sale of that instrument.

The Fund may use non-binding indicative bid prices provided by an independent pricing service or broker as the primary basis for determining the value of CLO debt and CLO equity (subordinated securities), which may be adjusted for pending distributions, as applicable, as of the valuation date. These bid prices are non-binding, and may not be determinative of an actual transaction price. As such, they may be considered Level 3 in the fair value hierarchy, absent additional information. In valuing the Fund’s investments in CLO debt and CLO equity (subordinated securities), in addition to non-binding indicative bid prices provided by an independent pricing service or broker, the Pricing Committee also may consider a variety of relevant factors, as set forth in the Valuation Policy, including recent trading prices for specific investments, recent purchases and sales known to the Fund in similar securities, other information known to the Fund relating to the securities, and discounted cash flows based on output from a third-party financial model, using projected future cash flows.

Information that becomes known after the Fund’s NAV has been calculated on a particular day will not be used to retroactively adjust the price of a security or the Fund’s previously determined NAV.

The Fund discloses the classification of its fair value measurements following a three-tier hierarchy based on the inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

17

Octagon XAI CLO Income Fund

NOTES TO FINANCIAL STATEMENTS

September 30, 2025 (Continued)

Various inputs are used in determining the value of the Fund’s investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments.

These inputs are categorized in the following hierarchy under applicable financial accounting standards:

Level 1 – Unadjusted quoted prices in active markets for identical investments, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date;

Level 2 – Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and

Level 3 – Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date.

The following is a summary of the inputs used to value the Fund’s investments as of September 30, 2025:

| Investments in Securities at Value(a) | Level

1 - Quoted Prices | Level

2 - Significant Observable Inputs | Level

3 - Significant Unobservable Inputs | Total | ||||||||||||

| Collateralized Loan Obligations Debt | $ | – | $ | 47,660,695 | $ | – | $ | 47,660,695 | ||||||||

| Collateralized Loan Obligations Equity | – | 2,904,533 | – | 2,904,533 | ||||||||||||

| Money Market Funds | 979,912 | – | – | 979,912 | ||||||||||||

| Total | $ | 979,912 | $ | 50,565,228 | $ | – | $ | 51,545,140 |

| (a) | For detailed descriptions and other security classifications, see the accompanying Schedule of Investments. |

There weren’t any transfers into or out of level 3 for the period ended September 30, 2025.

NOTE 3 - INVESTMENT ADVISORY AND OTHER AGREEMENTS

XAI serves as the investment adviser to the Fund and is responsible for overseeing the Fund’s overall investment strategy and its implementation. Octagon Credit Investors, LLC (“Octagon” or the “Sub-Adviser”) serves as the investment sub-adviser of the Fund and is responsible for investing the Fund’s assets. The Fund pays an advisory fee to the Adviser. The Adviser pays to the Sub-Adviser a sub-advisory fee out of the advisory fee received by the Adviser.

Pursuant to an investment advisory agreement between the Fund and the Adviser, the Fund pays the Adviser a fee, payable monthly in arrears, in an annual amount equal to 1.50% of the Fund’s average daily Managed Assets. “Managed Assets” means the total assets of the Fund, including assets attributable to the Fund’s use of leverage, minus the sum of its accrued liabilities (other than liabilities incurred for the purpose of creating leverage). For the period ended September 30, 2025, the Fund incurred $423,010 in advisory fees.

Pursuant to an investment sub-advisory agreement among the Fund, the Adviser and the Sub- Adviser, the sub-advisory fee, payable monthly in arrears to the Sub-Adviser, is calculated as a specified percentage of the advisory fee payable by the Fund to the Adviser (before giving effect to any fees waived or expenses reimbursed by the Adviser). The specified percentage is equal to the blended percentage computed by applying the following percentages to the average daily Managed Assets of the Fund:

| Percentage of Advisory | ||||

| Average Daily Managed Assets | Fee | |||

| First $200 million | 70 | % | ||

| Next $300 million | 60 | % | ||

| Over $500 million | 50 | % | ||

The Fund does not pay a performance or incentive fee to the Adviser or the Sub-Adviser. For the period ended September 30, 2025, the Fund incurred $1,809 in reimbursements made to the Sub-Adviser. These costs are included in other expenses in the Statement of Operations. The Fund pays all costs and expenses of its operations, subject to the Operating Expense Limitation Agreement (as described below).

The Fund, the Adviser and the Sub-Advisor have entered into a letter agreement, effective as of November 11, 2024 (the “Operating Expense Limitation Agreement”), pursuant to which the Adviser and the Sub-Adviser have agreed to waive a portion of their advisory or sub-advisory fees, as applicable, or reimburse the Fund for certain operating expenses so that the annual operating expenses of the Fund (exclusive of any Excluded Expenses (as defined below) do not exceed 0.68% of the Fund’s Managed Assets (the “Operating Expense Limitation”). For purposes of the Operating Expense Limitation Agreement, “Excluded Expenses” are (i) investment advisory fees, (ii) investor support and secondary market services fees, (iii) taxes, (iv) expenses incurred directly or indirectly by the Fund as a result of an investment in a permitted investment (including, without limitation, acquired fund fees and expenses), (v) expenses associated with the acquisition or disposition of portfolio investments (including, without limitation, brokerage commissions and other trading or transaction expenses), (vi) leverage expenses (including, without limitation, costs associated with the issuance or incurrence of leverage, commitment fees, interest expense or dividends on preferred shares), (vii) distribution and/or shareholder servicing (12b-1) fees, (viii) dividends on short sales, if any, (ix) securities lending costs, if any, (x) expenses of holding, and soliciting proxies for, meetings of shareholders of the Fund (except to the extent relating to routine items such as the election of trustees), (xi) expenses of a reorganization, restructuring, redomiciling or merger of the Fund or the acquisition of all or substantially all of the assets of another fund, or (xii) any extraordinary expenses not incurred in the ordinary course of the Fund’s business (including, without limitation, expenses related to litigation, derivative actions, demands related to litigation, regulatory or other government investigations and proceeding).

18

Octagon XAI CLO Income Fund

NOTES TO FINANCIAL STATEMENTS

September 30, 2025 (Continued)

The Operating Expense Limitation Agreement provides that the Adviser and the Sub-Adviser may recoup amounts reimbursed pursuant to the Operating Expense Limitation Agreement for a period not to exceed three years following the date of such waiver or reimbursement, to the extent such recoupment does not cause the Fund’s operating expenses to exceed (a) the Operating Expense Limitation in effect at the time the expense was paid or absorbed, and (b) the Operating Expense Limitation in effect at the time of such recoupment. Any recoupment shall be allocated between the Adviser and the Sub- Adviser in the same proportion as the allocation of waived fees and/or reimbursed expenses being recouped. The Operating Expense Limitation Agreement shall remain in effect according to its terms until March 31, 2026, unless sooner terminated with the written consent of the Board of Trustees of the Fund. The agreement will terminate automatically upon the termination of the Advisory Agreement or the Sub-Advisory Agreement unless a new Advisory Agreement with the Adviser (or an affiliate of the Adviser) or a new Sub-Advisory Agreement with the Sub-Adviser (or an affiliate of the Sub-Adviser), as applicable, to replace the terminated agreement becomes effective upon such termination.

| Fees Waived/ Reimbursed By Advisor | Recoupment of Past Waived Fees By Advisor(a) | |||||||

| Class I | $ | 490,657 | $ | 202,480 | ||||

| Class A | 80,654 | 47,605 |

| (a) | As of September 30, 2025, $33,353 was payable to the Advisor. |

As of September 30, 2025, the reimbursed expenses subject to potential recovery by year of expiration are as follows:

| Expiring | ||||

| September 30, 2028 | ||||

| Class I | $ | 288,177 | ||

| Class A | 33,049 | |||

| Total | $ | 321,226 |

Paralel Technologies LLC (“PRT”) serves as the Fund’s administrator, accounting agent and transfer agent pursuant to an Administration and Fund Accounting Agreement and Transfer Agent Agreement, respectively, and receives customary fees from the Fund for such services. Administrative and accounting fees and transfer agency fees paid by the Fund for the period ended September 30, 2025 are disclosed in the Statement of Operations.

Paralel Distributors LLC (the “Distributor”) acts as the principal underwriter for the Fund and distributes shares pursuant to a Distribution Agreement. The Fund’s shares may be offered through other brokers, dealers and other financial intermediaries that have entered into selling agreements with the Distributor. The Distributor is a broker-dealer registered under the Securities Exchange Act of 1934, as amended, and is a member of the Financial Industry Regulatory Authority (“FINRA”). Paralel Distributors LLC is an affiliate of PRT.

Employees of PINE Advisors LLC (“PINE”) serve as the Fund’s chief compliance officer and principal financial officer. PINE provides services that assist the Fund’s chief compliance officer in monitoring and testing the policies and procedures of the Fund in conjunction with requirements under Rule 38a-1 under the 1940 Act and receives an annual base fee. PINE receives an annual base fee for the services provided to the Fund and is reimbursed for certain out-of-pocket expenses by the Fund. Service fees paid by the Fund for the period ended September 30, 2025 are disclosed in the Statement of Operations.

U.S. Bank N.A. (the “Custodian”) serves as the Fund’s custodian, under which the Custodian holds the Fund’s assets in compliance with the 1940 Act. Custodian fees paid by the Fund for the period ended September 30, 2025, are disclosed in the Statement of Operations.

Indemnification – The Fund indemnifies its officers and Trustees for certain liabilities that may arise from the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on industry experience, the Fund expects the risk of loss due to these warranties and indemnities to be remote.

NOTE 4 - DISTRIBUTION AND SERVICING PLAN

The Fund has adopted a Distribution and Servicing Plan for the Class A Shares of the Fund. The Distribution and Servicing Plan operates in a manner consistent with Rule 12b-1 under the 1940 Act, which regulates the manner in which an open-end investment company may directly or indirectly bear the expenses of distributing its shares. Although the Fund is not an open-end investment company, it has undertaken to comply with the terms of Rule 12b-1 as a condition of exemptive relief which it has been granted under the 1940 Act which permits it to have, among other things, a multi-class structure and distribution and/or shareholder servicing fees. The Distribution and Servicing Plan permits the Fund to compensate the Distributor for providing or procuring through financial firms, distribution, administrative, recordkeeping, shareholder and/or related services with respect to the Class A Shares. Most or all of the distribution and/or service fees are paid to financial firms through which shareholders may purchase or hold Class A Shares.

The maximum annual rates at which the distribution and/or servicing fees may be paid under the Distribution and Servicing Plan for Class A Shares (calculated as a percentage of the Fund’s average daily net assets attributable to the Class A Shares) is 0.85%. Payment of the Distribution and/or Servicing Fee is governed by the Fund’s Distribution and Servicing Plan.

The Fund also may pay for sub-transfer agency, sub-accounting and certain other administrative services outside of its Distribution and Servicing Plan.

Class I Shares do not incur a Distribution and/or Servicing Fee.

19

Octagon XAI CLO Income Fund

NOTES TO FINANCIAL STATEMENTS

September 30, 2025 (Continued)

The Adviser and the Sub-Adviser have agreed to enter into an Expense Limitation and Reimbursement Agreement with the Fund through May 4, 2026 (the “Limitation Period”). Under the Expense Limitation and Reimbursement Agreement, the Adviser and the Sub-Adviser have agreed to reimburse the Fund for a portion of distribution and/or shareholder servicing fees paid and/or accrued during the Limitation Period in an amount equal to 0.50% of the Fund’s average daily net assets. Any reimbursement amount shall be allocated between the Adviser and the Sub-Adviser in the same proportion as the Specified Percentage (as defined in the Sub-Advisory Agreement) as calculated at the time of such reimbursement. During the Reimbursement Period, the Expense Limitation and Reimbursement Agreement may be terminated or modified only with the written consent of the Board of Trustees. For a period not to exceed three years from the date on which fees are waived, the Adviser and the Sub-Adviser may recoup amounts reimbursed, provided that, after giving effect to such recoupment, the Fund’s expense ratio (excluding Excluded Expenses, as defined below) is not greater than (i) the Fund’s expense ratio (excluding Excluded Expenses) at the time the fees were waived or (ii) any expense limitation in effect at the time of such recoupment. “Excluded Expenses” are management fees, distribution and/or servicing fees, taxes, leverage interest, brokerage commissions, dividend and interest expenses on short sales, acquired fund fees and expenses (as determined in accordance with SEC Form N-2), expenses incurred in connection with any merger or reorganization, and extraordinary expenses, such as litigation expenses. Any recoupment payment shall be allocated between the Adviser and the Sub-Adviser in the same proportion as the allocation of the reimbursement amount being recouped pursuant to such recoupment payment (i.e. in the same proportion as the Specified Percentage as (defined in the Sub-Advisory Agreement) as calculated at the time of the applicable reimbursement). The Expense Limitation and Reimbursement Agreement is separate from the Operating Expense Limitation Agreement. For the period ended September 30, 2025, the amount of distribution and/or shareholder servicing fees reimbursed to the Fund subject to recoupment were $24,990.

NOTE 5 - CAPITAL TRANSACTIONS

The Fund engages in a continuous offering of its Shares under Rule 415 under the Securities Act of 1933, as amended. The Fund offers to sell, through the Distributor, its Shares at the then-current NAV per Share. The Fund, pursuant to exemptive relief granted by the SEC, offers multiple classes of shares. The maximum sales load imposed on purchases and distribution and/or servicing fees charged vary depending on the share class.

Share transactions were as follows:

| Period Ended | Period Ended | |||||||

| September 30, 2025(a) | September 30, 2024(b) | |||||||

| Class I | ||||||||

| Common shares sold | 1,613,376 | 4,000 | ||||||

| Common shares issued as reinvestment of dividends | 15,745 | – | ||||||

| Common shares repurchased | (8 | ) | – | |||||

| Net increase in shares outstanding | 1,629,113 | 4,000 | ||||||

| Class A | ||||||||

| Common shares sold | 438,307 | – | ||||||

| Common shares issued as reinvestment of dividends | 9,193 | – | ||||||

| Common shares repurchased | – | – | ||||||

| Net increase in shares outstanding | 447,500 | – | ||||||

| (a) | Reflects operations for the period from November 4, 2024 (commencement of operations) to September 30, 2025 for Class I Shares and December 2, 2024 to September 30, 2025 for Class A Shares. |

| (b) | For the period ended September 30, 2024, the Fund did not have capital transactions outside of the initial seed purchase on January 18, 2024. |