UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the

Securities Exchange Act of 1934

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Pursuant to §240.14a-12 |

XAI CLO & Income Opportunities Fund

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(4) and 0-11. |

On June 30, 2026, XAI Floating Rate & Alternative Income Trust (NYSE: XFLT) (“XFLT”) and XAI CLO & Income Opportunities Fund (“OCTIX”) (together, the “Funds”) hosted a webinar in connection with each Fund’s special meeting of shareholders to be held on July 30, 2026. Set forth below are copies of the webinar materials, a transcript of the webinar and the text of an email that will be sent to shareholders, which includes a hyperlink (https://xainvestments.com/knowledge-bank/webinars/?url=presentation-20260630) to a replay of the webinar.

Important Shareholder Update: XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 Your Vote Matters! CONFIDENTIAL – INSTITUTIONAL USE ONLY – NOT FOR DISTRIBUTION

This presentation is intended to be educational in nature and is not for the purpose of recommending a particular investment. The investments discussed may or may not be suitable for the audience of this presentation. Neither XA Investments LLC (“XAI”), King Street Capital Management L.P. (“King Street”) or Rockford Tower Asset Management L.L.C. (“Rockford Tower” and “King Street Sub - Adviser”) is acting as an adviser to the audience members, and audience members should consult their own investment adviser prior to making investment decisions. Each of XAI Floating Rate & Alternative Income Trust (“XFLT”) and XAI CLO & Income Opportunities Fund (“OCTIX” and, together with XFLT, the “Funds” and each a “Fund”) has filed a proxy statement and other proxy materials with the Securities and Exchange Commission (“SEC”) in connection with the matters described herein. The definitive proxy statements have been mailed to shareholders of the Funds. Investors are urged to read the proxy materials and any other relevant documents filed or to be filed with the SEC carefully because they contain or will contain important information about the proposals discussed herein. Free copies of the proxy statements and other proxy materials are or will be available on the SEC’s website at www.sec.gov . This presentation does not constitute an offer to sell or a solicitation of an offer to buy any securities of the Funds. Some information in this presentation reflects proprietary research based upon various data sources. In addition, some information cited in this presentation has been taken from third - party sources that are believed to be reliable but which have not been verified for accuracy or completeness. Neither XAI or King Street nor their respective affiliates (collectively, the “Investment Managers”), is responsible for errors or omissions from these sources. No representation is made with respect to the accuracy, completeness or timeliness of information and the Investment Managers assume no obligation to update or otherwise revise such information. The Investment Managers make no representation that the information contained in this presentation is accurate or complete, nor do they review or assume any responsibility for any information received from, or created by, any third parties, including the performance data of indexes and benchmarks. Views expressed herein are subject to change without notice. All data concerning returns and satisfaction of performance tests are historical and based on the Investment Managers’ knowledge; as such, they do not represent current performance levels, some or all of which may have changed since the dates referenced herein. This document does not constitute investment, tax, legal, regulatory or accounting advice. Under no circumstances should this document be used or considered as an offer to sell or a solicitation of an offer to buy any security, financial instrument or investment vehicle. Investors are advised to make an independent review regarding the economic benefits and risks of purchasing or selling the financial instruments mentioned in this document and reach their own conclusions regarding the legal, tax, regulatory, accounting and other aspects of any transaction in the financial instrument in relation to their particular circumstances. Investments described herein carry a risk of loss, which could be significant, and that investors should be prepared to bear. King Street and/or its affiliated companies may make a market or deal as principal in the financial instruments mentioned in this document or in related securities, options or other derivative instruments based on them. In addition, the Investment Managers, their affiliated companies, shareholders, directors, officers and/or employees, may from time to time have long or short positions in the financial instruments, including loans, securities or in options, futures or other derivative instruments based on them. Performance achieved prior to December 31, 2021 is predominantly based on investments that used U.S. dollar LIBOR as a reference rate. Overnight and 12 - month U.S. dollar LIBOR permanently ceased as of June 30, 2023. 1 - , 3 - , and 6 - month U.S. dollar LIBOR settings ceased as of September 2024. As an alternative to LIBOR, the Financial Reporting Council, in conjunction with the Alternative Reference Rates Committee, a steering committee comprised of large U.S. financial institutions, recommended replacing U.S. dollar LIBOR with Secured Overnight Financing Rate (“SOFR”), an index calculated by reference to short - term repurchase agreements, backed by U.S. Treasury securities. There is no guarantee that the performance of individual investments or the syndicated debt and CLO securities markets as a whole during or after the transition period will be consistent with performance achieved during the LIBOR era. Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted. Similar investments likely would produce different results under different economic and market conditions. These materials contain forward - looking statements. Investors should not place undue reliance on forward - looking statements. Actual results could differ materially from those referenced in forward - looking statements for many reasons. Forward - looking statements are necessarily speculative in nature, and it can be expected that some or all of the assumptions underlying any forward - looking statements will not materialize or will vary significantly from actual results. Variations of assumptions and results may be material. Without limiting the generality of the foregoing, the inclusion of forward - looking statements herein should not be regarded as a representation by the Funds, Investment Managers or any of their respective affiliates or any other person of the results that will actually be achieved by the Fund. None of the foregoing persons has any obligation to update or otherwise revise any forward - looking statements, including any revision to reflect changes in any circumstances arising after the date hereof relating to any assumptions or otherwise. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 2 General Disclosures

Executive Summary XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 3 Source: XA Investments LLC. Sub - Adviser Change • The Board of Trustees of each of XAI Floating Rate & Alternative Income Trust (“XFLT”) and XAI CLO & Income Opportunities Fund (“OCTIX” and, together with XFLT, the “Funds” and each a “Fund”) has unanimously approved Rockford Tower Asset Management (“King Street Sub - Adviser”), a wholly owned subsidiary of King Street Capital Management (“King Street”), to serve as investment sub - adviser for each Fund pursuant to a new investment sub - advisory agreement among the Fund, XA Investments LLC (“XAI,” “XA Investments” or the “Adviser”) and the King Street Sub - Adviser. • A shareholder proxy statement has been filed with the SEC to seek the shareholder vote required to complete the transition. Why King Street? • King Street is a leading global alternative asset manager with approximately $30 billion in assets under management, founded in 1995, supported by 99 investment professionals, and an established CLO platform spanning 29 active U.S. and European CLOs. • Young Choi, Partner and Global Head of Trading at King Street, will serve as lead portfolio manager; he brings 27 years of experience, including 20 years at King Street and prior roles managing a $2 billion leveraged loan and CLO portfolio at Citadel Investment Group. Expanded Opportunity Set • Under the King Street Sub - Adviser’s proposed management, both XFLT and OCTIX will seek access to additional investment opportunities, including European CLO debt, CLO equity, and asset - backed securities. XFLT may also seek additional investments in CLO warehouse opportunities. OCTIX will seek additional opportunistic investments in indirect private credit through listed BDCs. Vote Your Shares • Shareholders of record as of June 2, 2026, are entitled to vote at the Special Meetings scheduled for July 30, 2026, and may cast their vote online, by phone, or by mail ahead of the meeting, or in person on the day of the meeting; the Board unanimously recommends voting “FOR” the proposals. • Shareholders who have questions may contact Okapi Partners LLC, the proxy solicitation agent, toll - free at (855) 305 - 0855 or reach the XA Investments team at (888) 903 - 3358 or at www.xainvestments.com .

ITD Annualized Total Return 3 1 Year Total Return 6 Month Total Return Quarter - to - Date Total Return Inception Date OCTIX Net Returns 3.15% 2.98% - 2.00% - 2.64% 11/4/2024 Class I (OCTIX) 2.19% 4 2.63% - 2.17% - 2.73% 11/29/2024 Class A (OCTAX) 5.40% 5.86% 0.73% - 0.55% Benchmark 5 - 2.25% - 2.88% - 2.73% - 2.09% OCTIX NAV Relative to Benchmark 5. OCTIX’s benchmark is a blended benchmark comprised of 50% ICE BofA U.S. High Yield Index and 50% Morningstar LSTA U.S. Leveraged Loan Index. Current performance may be higher or lower than the data shown. Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 4 ITD Annualized Total Return 1 5 Year Annualized Total Return 3 Year Annualized Total Return 1 Year Total Return Quarter - to - date Total Return XFLT Net Returns 3.28% 2.59% 4.05% - 13.15% - 12.21% $22.30 NAV - 0.10% - 5.30% - 5.16% - 31.05% - 24.75% $17.18 Price 5.19% 5.91% 8.35% 5.94% - 0.78% Benchmark 2 - 1.91% - 3.32% - 4.30% - 19.09% - 11.43% XFLT NAV Relative to Benchmark - 5.29% - 11.21% - 13.51% - 36.99% - 23.97% XFLT Price Relative to Benchmark Sources: XA Investments LLC; Paralel. Notes: Period returns shown net of fees and expenses. The performance shown derives from the Fund’s books and records. 1. Represents annualized total return from 9/26/2017 (XFLT’s inception) - 3/31/2026. 2. XFLT’s benchmark is the Morningstar LSTA Leveraged Loan 100 Index. 3. Represents annualized total return from 11/4/2024 (OCTIX’s inception) - 3/31/2026. 4. Represents annualized total return from 11/29/2024 (OCTAX’s inception) - 3/31/2026. Historical Performance Under Octagon’s Management (as of 3/31/2026)

XFLT and OCTIX Quarter - end NAVs Sources: XA Investments LLC; Paralel. Notes: Data as of 3/31/2026. The NAVs shown derive from the Fund’s books and records. Charts do not represent total return and are not inclusive of distributions. XFLT Quarter - End NAV (9/29/2017 - 3/31/2026) $60.00 54.40% Decrease in NAV Over Reported Period $48.90 $23.90 $40.95 $34.70 $22.30 $15.00 $30.00 $45.00 XFLT NAV OCTIX Quarter - End NAV (12/31/2024 - 3/31/2026) $26.00 6.99% Decrease in NAV Over Reported Period $25.34 $24.96 $25.27 $25.00 $24.67 $23.57 $23.50 $23.00 $24.50 $24.00 $25.00 $25.50 Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 5

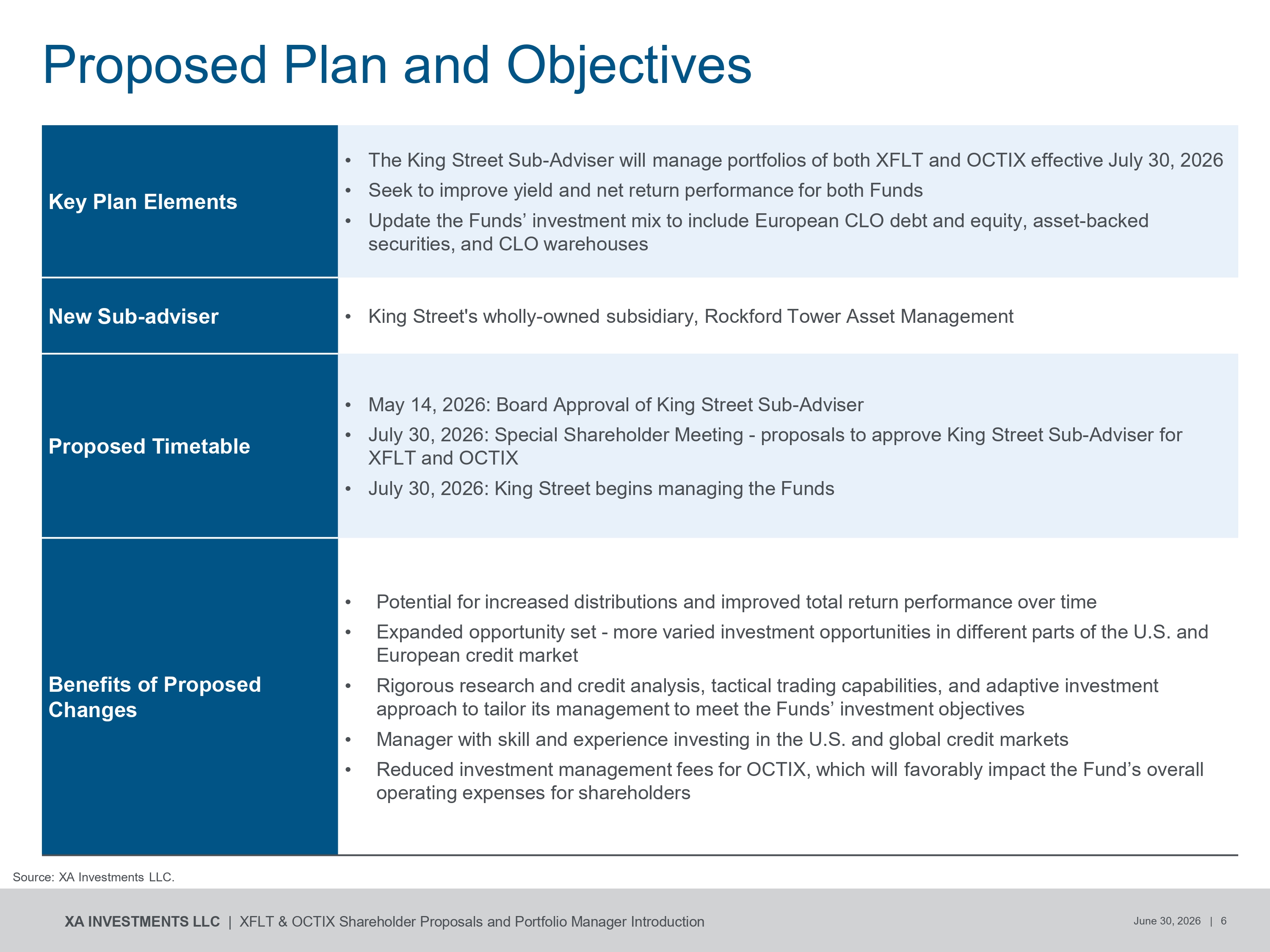

Proposed Plan and Objectives Source: XA Investments LLC. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 6 • The King Street Sub - Adviser will manage portfolios of both XFLT and OCTIX effective July 30, 2026 • Seek to improve yield and net return performance for both Funds • Update the Funds’ investment mix to include European CLO debt and equity, asset - backed securities, and CLO warehouses Key Plan Elements • King Street’s wholly - owned subsidiary, Rockford Tower Asset Management New Sub - adviser • May 14, 2026: Board Approval of King Street Sub - Adviser • July 30, 2026: Special Shareholder Meeting - proposals to approve King Street Sub - Adviser for XFLT and OCTIX • July 30, 2026: King Street begins managing the Funds Proposed Timetable • Potential for increased distributions and improved total return performance over time • Expanded opportunity set - more varied investment opportunities in different parts of the U.S. and European credit market • Rigorous research and credit analysis, tactical trading capabilities, and adaptive investment approach to tailor its management to meet the Funds’ investment objectives • Manager with skill and experience investing in the U.S. and global credit markets • Reduced investment management fees for OCTIX, which will favorably impact the Fund’s overall operating expenses for shareholders Benefits of Proposed Changes

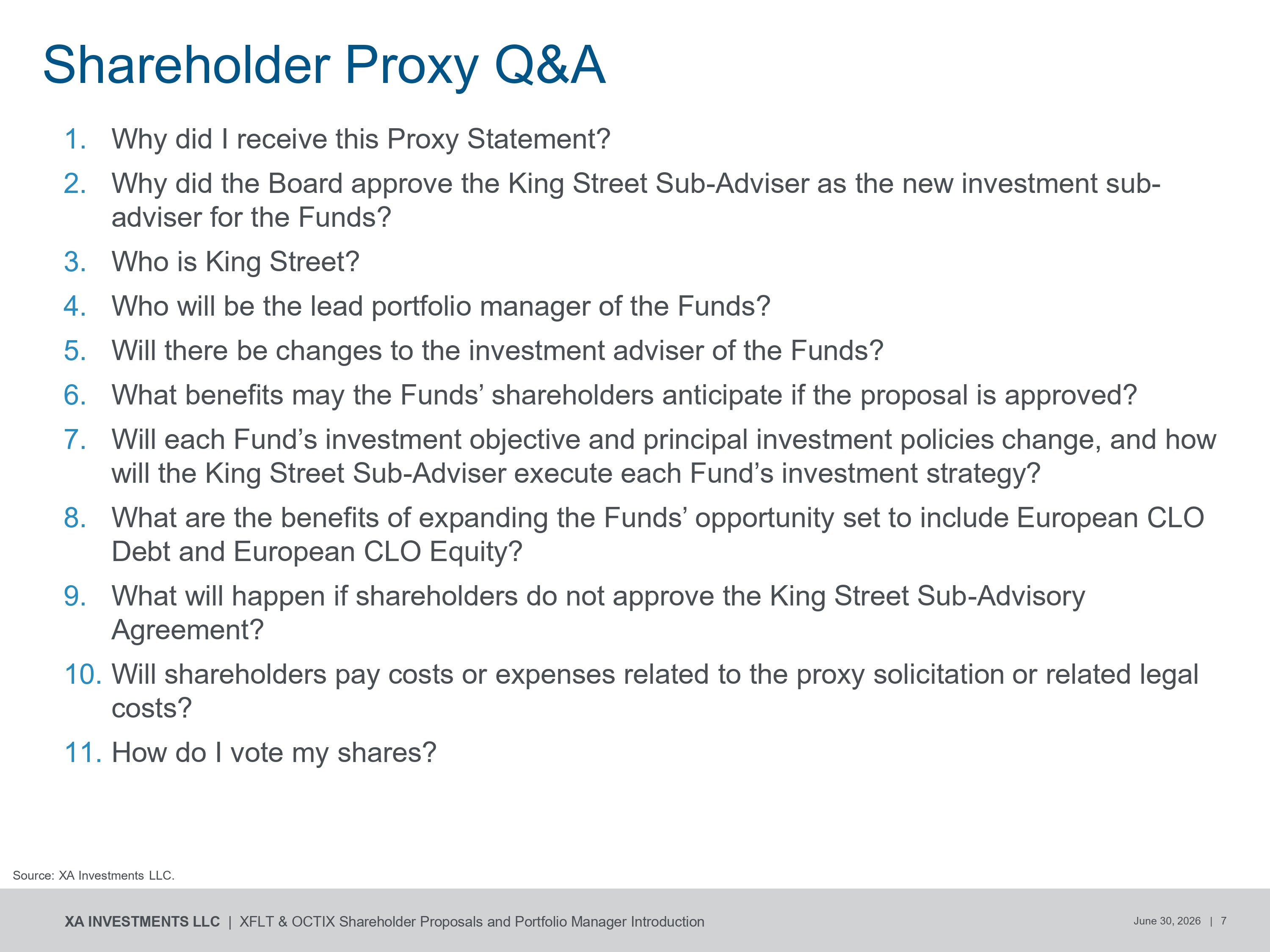

Shareholder Proxy Q&A Source: XA Investments LLC. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 7 1. Why did I receive this Proxy Statement? 2. Why did the Board approve the King Street Sub - Adviser as the new investment sub - adviser for the Funds? 3. Who is King Street? 4. Who will be the lead portfolio manager of the Funds? 5. Will there be changes to the investment adviser of the Funds? 6. What benefits may the Funds’ shareholders anticipate if the proposal is approved? 7. Will each Fund’s investment objective and principal investment policies change, and how will the King Street Sub - Adviser execute each Fund’s investment strategy? 8. What are the benefits of expanding the Funds’ opportunity set to include European CLO Debt and European CLO Equity? 9. What will happen if shareholders do not approve the King Street Sub - Advisory Agreement? 10. Will shareholders pay costs or expenses related to the proxy solicitation or related legal costs? 11. How do I vote my shares?

Introducing Young Choi, Portfolio Manager Mr. Choi is a Partner and the Global Head of Trading at King Street and the Portfolio Manager of Rockford Tower Capital Management. He is based in New York and is a member of the Management Committee, Global Investment Committee, U.S. and European CLO Investment Committees, Risk Committee and Pricing Committee. Prior to joining King Street in 2006, Mr. Choi worked at Citadel Investment Group as a Credit Analyst in the Distressed/High Yield Group and was Portfolio Manager of the firm’s $2 billion U.S. leveraged loan and CLO portfolio. Prior to that, Mr. Choi consulted at Bain & Co. Mr. Choi received a B.A. summa cum laude in Economics and a B.S.E. in Electrical Engineering from Duke University. Partner Global Investment Committee, Global Head of Trading, Portfolio Manager - Rockford Tower Sources: XA Investments LLC; King Street. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 8

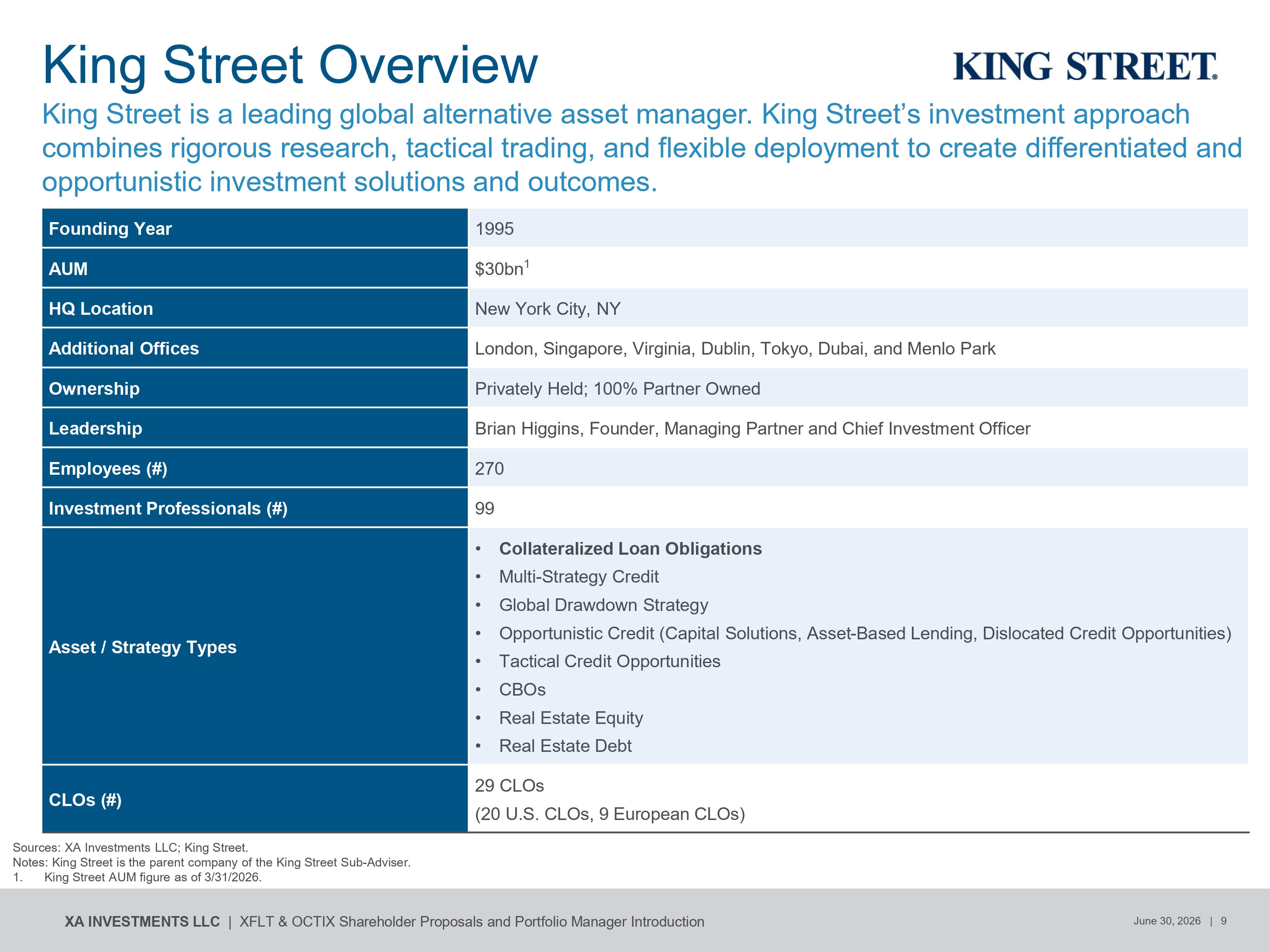

Sources: XA Investments LLC; King Street. Notes: King Street is the parent company of the King Street Sub - Adviser. 1995 Founding Year $30bn 1 AUM New York City, NY HQ Location London, Singapore, Virginia, Dublin, Tokyo, Dubai, and Menlo Park Additional Offices Privately Held; 100% Partner Owned Ownership Brian Higgins, Founder, Managing Partner and Chief Investment Officer Leadership 270 Employees (#) 99 Investment Professionals (#) • Collateralized Loan Obligations • Multi - Strategy Credit • Global Drawdown Strategy • Opportunistic Credit (Capital Solutions, Asset - Based Lending, Dislocated Credit Opportunities) • Tactical Credit Opportunities • CBOs • Real Estate Equity • Real Estate Debt Asset / Strategy Types 29 CLOs (20 U.S. CLOs, 9 European CLOs) CLOs (#) King Street Overview King Street is a leading global alternative asset manager. King Street’s investment approach combines rigorous research, tactical trading, and flexible deployment to create differentiated and opportunistic investment solutions and outcomes. 1. King Street AUM figure as of 3/31/2026. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 9

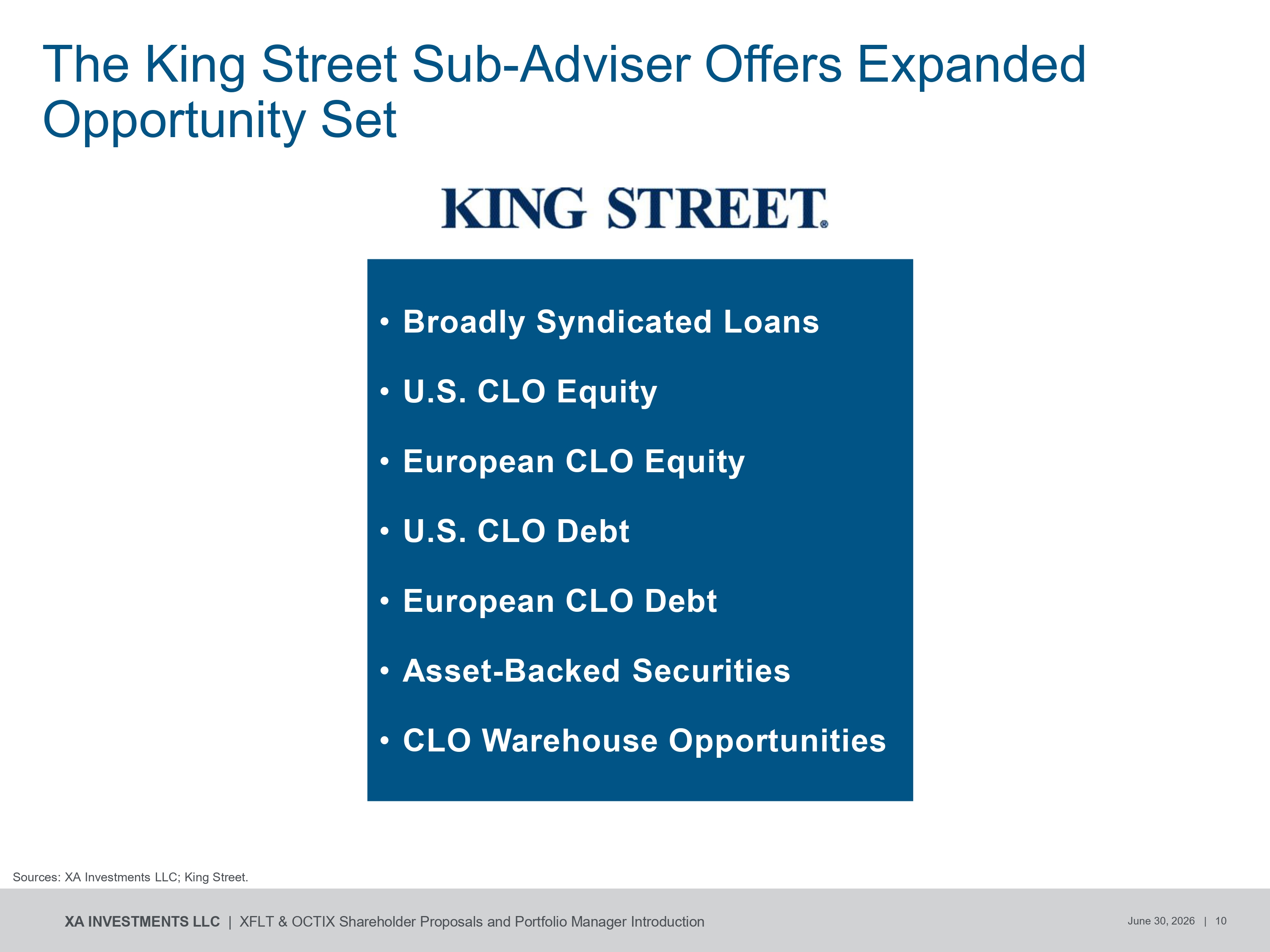

The King Street Sub - Adviser Offers Expanded Opportunity Set • Broadly Syndicated Loans • U.S. CLO Equity • European CLO Equity • U.S. CLO Debt • European CLO Debt • Asset - Backed Securities • CLO Warehouse Opportunities Sources: XA Investments LLC; King Street. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 10

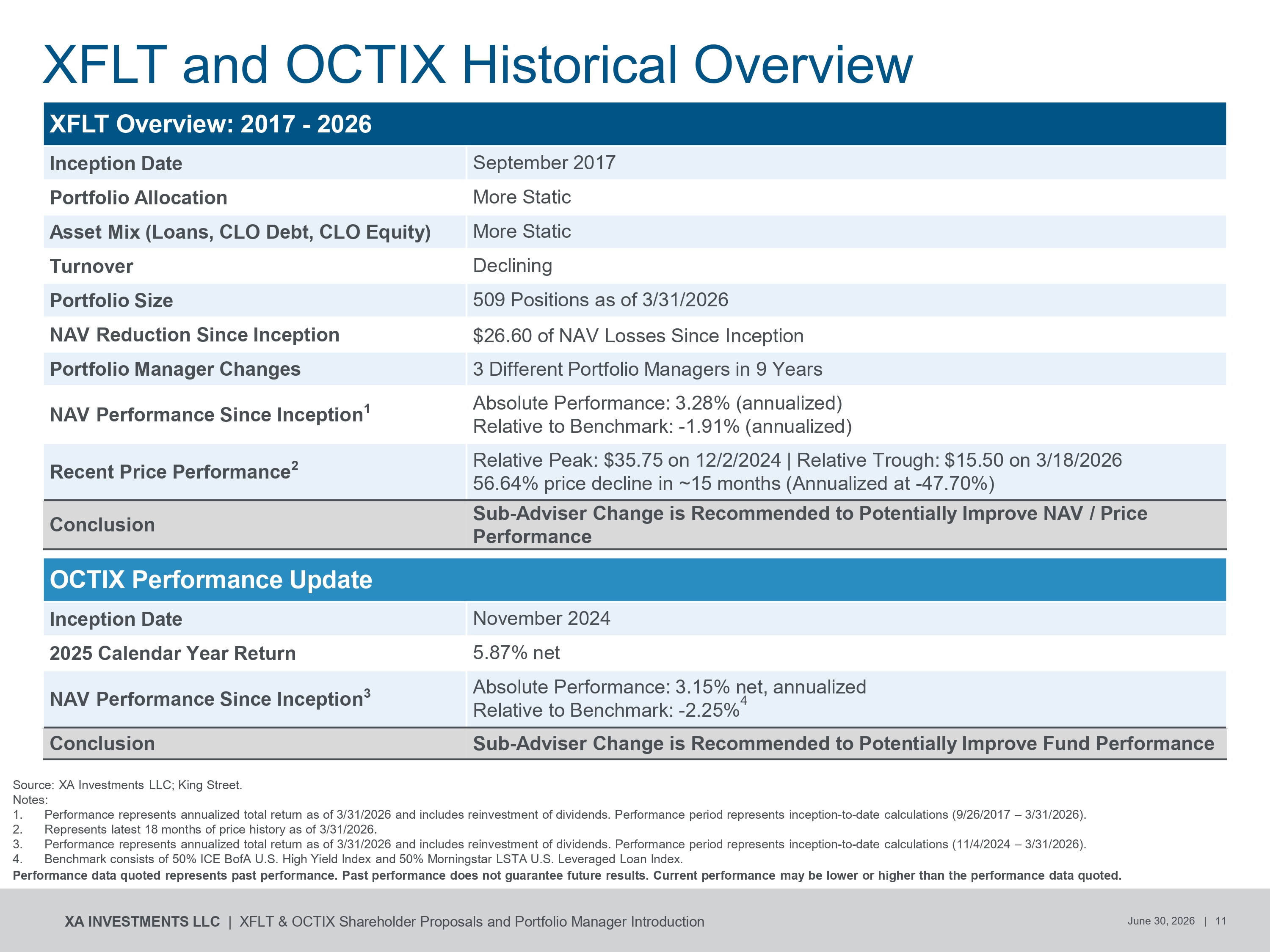

XFLT and OCTIX Historical Overview Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 11 XFLT Overview: 2017 - 2026 September 2017 Inception Date More Static Portfolio Allocation More Static Asset Mix (Loans, CLO Debt, CLO Equity) Declining Turnover 509 Positions as of 3/31/2026 Portfolio Size $26.60 of NAV Losses Since Inception NAV Reduction Since Inception 3 Different Portfolio Managers in 9 Years Portfolio Manager Changes Absolute Performance: 3.28% (annualized) Relative to Benchmark: - 1.91% (annualized) NAV Performance Since Inception 1 Relative Peak: $35.75 on 12/2/2024 | Relative Trough: $15.50 on 3/18/2026 56.64% price decline in ~15 months (Annualized at - 47.70%) Recent Price Performance 2 Sub - Adviser Change is Recommended to Potentially Improve NAV / Price Performance Conclusion OCTIX Performance Update November 2024 Inception Date 5.87% net 2025 Calendar Year Return Absolute Performance: 3.15% net, annualized Relative to Benchmark: - 2.25% 4 NAV Performance Since Inception 3 Sub - Adviser Change is Recommended to Potentially Improve Fund Performance Conclusion Source: XA Investments LLC; King Street. Notes: 1. Performance represents annualized total return as of 3/31/2026 and includes reinvestment of dividends. Performance period represents inception - to - date calculations (9/26/2017 – 3/31/2026). 2. Represents latest 18 months of price history as of 3/31/2026. 3. Performance represents annualized total return as of 3/31/2026 and includes reinvestment of dividends. Performance period represents inception - to - date calculations (11/4/2024 – 3/31/2026). 4. Benchmark consists of 50% ICE BofA U.S. High Yield Index and 50% Morningstar LSTA U.S. Leveraged Loan Index.

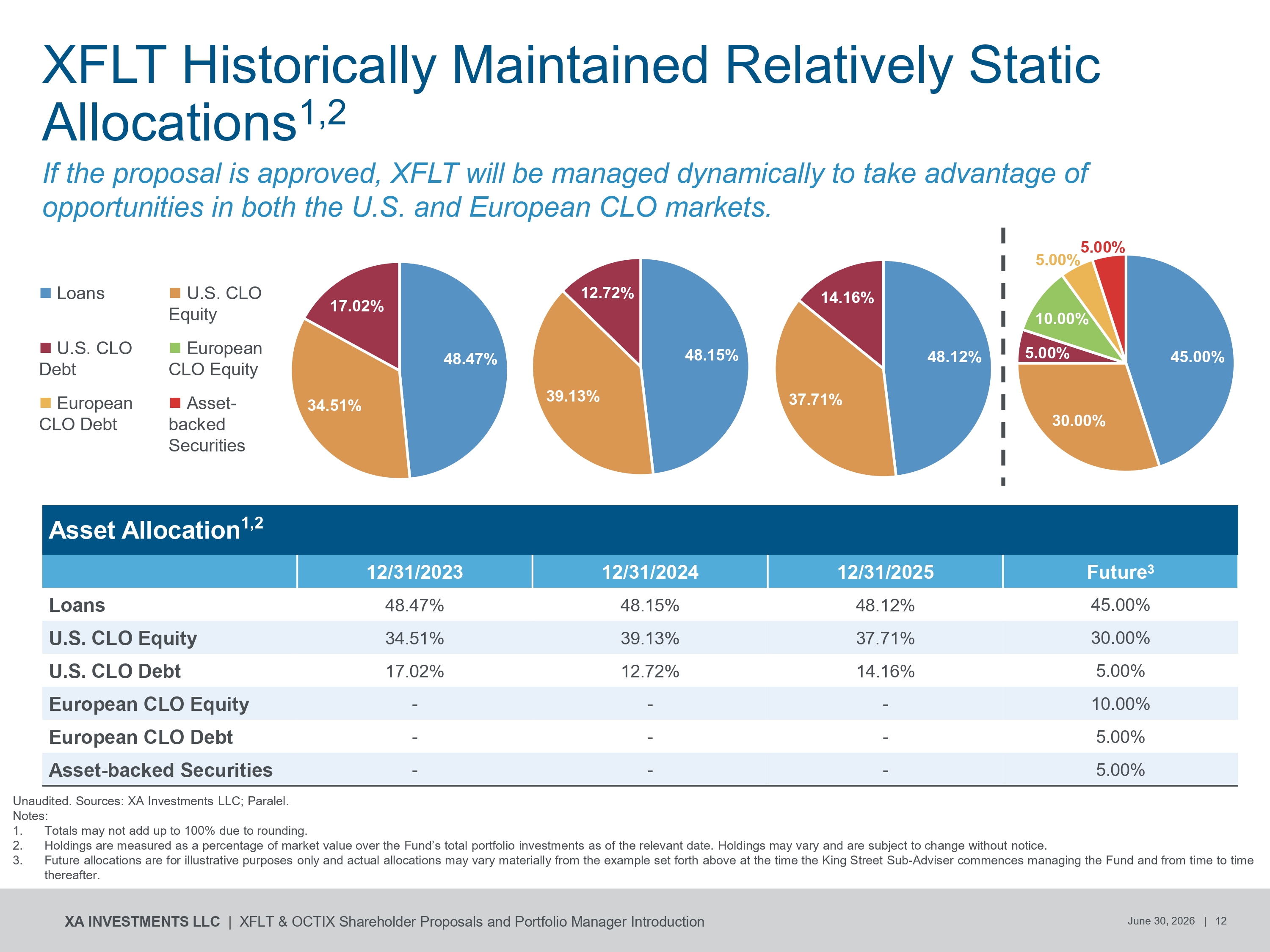

XFLT Historically Maintained Relatively Static Allocations 1,2 Asset Allocation 1,2 Future 3 12/31/2025 12/31/2024 12/31/2023 45.00% 48.12% 48.15% 48.47% Loans 30.00% 37.71% 39.13% 34.51% U.S. CLO Equity 5.00% 14.16% 12.72% 17.02% U.S. CLO Debt 10.00% - - - European CLO Equity 5.00% - - - European CLO Debt 5.00% - - - Asset - backed Securities U.S. CLO Equity Loans European CLO Equity U.S. CLO Debt Asset - backed Securities European CLO Debt Unaudited. Sources: XA Investments LLC; Paralel. Notes: 1. Totals may not add up to 100% due to rounding. 2. Holdings are measured as a percentage of market value over the Fund’s total portfolio investments as of the relevant date. Holdings may vary and are subject to change without notice. 3. Future allocations are for illustrative purposes only and actual allocations may vary materially from the example set forth above at the time the King Street Sub - Adviser commences managing the Fund and from time to time If the proposal is approved, XFLT will be managed dynamically to take advantage of opportunities in both the U.S. and European CLO markets. 48.15% 39.13% 12.72% 48.12% 37.71% 14.16% 48.47% 34.51% 17.02% 45.00% 30.00% 5.00% 10.00% 5.00% 5.00% thereafter. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 12

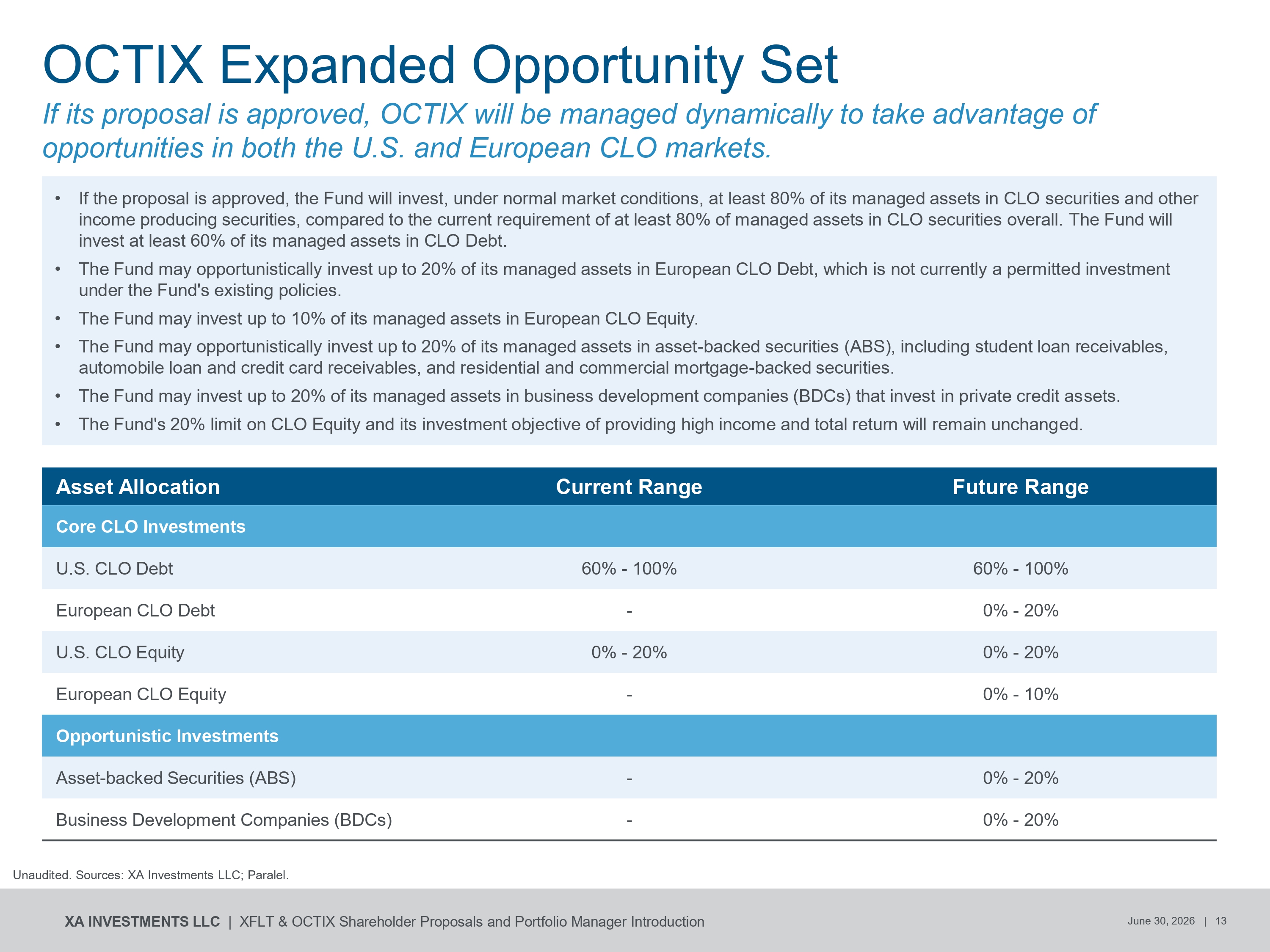

OCTIX Expanded Opportunity Set Unaudited. Sources: XA Investments LLC; Paralel. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 13 If its proposal is approved, OCTIX will be managed dynamically to take advantage of opportunities in both the U.S. and European CLO markets. Future Range Current Range Asset Allocation Core CLO Investments 60% - 100% 60% - 100% U.S. CLO Debt 0% - 20% - European CLO Debt 0% - 20% 0% - 20% U.S. CLO Equity 0% - 10% - European CLO Equity Opportunistic Investments 0% - 20% - Asset - backed Securities (ABS) 0% - 20% - Business Development Companies (BDCs) • If the proposal is approved, the Fund will invest, under normal market conditions, at least 80% of its managed assets in CLO securities and other income producing securities, compared to the current requirement of at least 80% of managed assets in CLO securities overall. The Fund will invest at least 60% of its managed assets in CLO Debt. • The Fund may opportunistically invest up to 20% of its managed assets in European CLO Debt, which is not currently a permitted investment under the Fund’s existing policies. • The Fund may invest up to 10% of its managed assets in European CLO Equity. • The Fund may opportunistically invest up to 20% of its managed assets in asset - backed securities (ABS), including student loan receivables, automobile loan and credit card receivables, and residential and commercial mortgage - backed securities. • The Fund may invest up to 20% of its managed assets in business development companies (BDCs) that invest in private credit assets. • The Fund’s 20% limit on CLO Equity and its investment objective of providing high income and total return will remain unchanged.

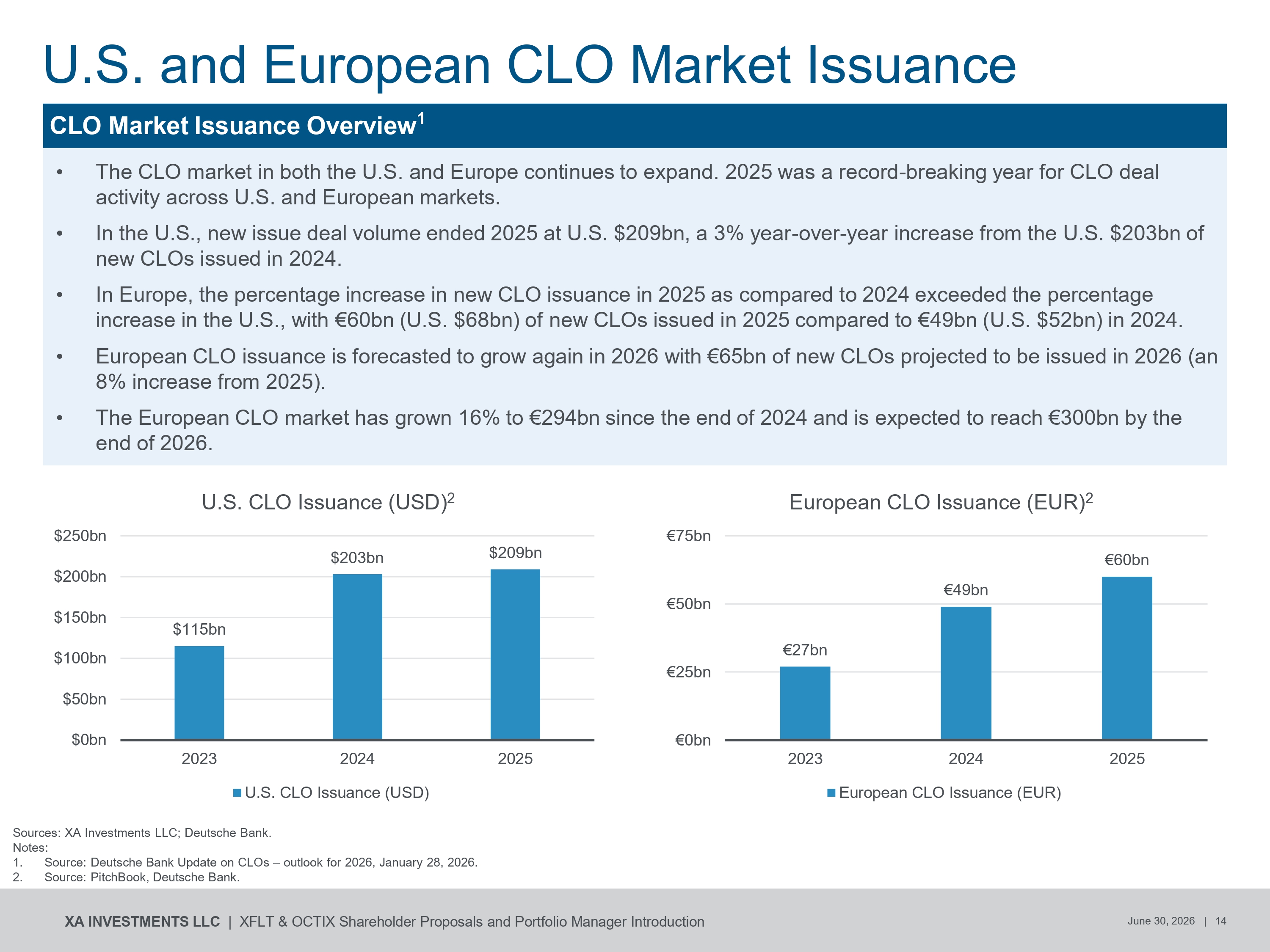

U.S. and European CLO Market Issuance Sources: XA Investments LLC; Deutsche Bank. Notes: 1. Source: Deutsche Bank Update on CLOs – outlook for 2026, January 28, 2026. 2. Source: PitchBook, Deutsche Bank. $115bn $203bn $209bn $0bn $50bn $100bn $150bn $200bn $250bn 2023 2024 2025 U.S. CLO Issuance (USD) 2 U.S. CLO Issuance (USD) CLO Market Issuance Overview 1 • The CLO market in both the U.S. and Europe continues to expand. 2025 was a record - breaking year for CLO deal activity across U.S. and European markets. • In the U.S., new issue deal volume ended 2025 at U.S. $209bn, a 3% year - over - year increase from the U.S. $203bn of new CLOs issued in 2024. • In Europe, the percentage increase in new CLO issuance in 2025 as compared to 2024 exceeded the percentage increase in the U.S., with €60bn (U.S. $68bn) of new CLOs issued in 2025 compared to €49bn (U.S. $52bn) in 2024. • European CLO issuance is forecasted to grow again in 2026 with €65bn of new CLOs projected to be issued in 2026 (an 8% increase from 2025). • The European CLO market has grown 16% to €294bn since the end of 2024 and is expected to reach €300bn by the end of 2026. €27bn €49bn €60bn €0bn €25bn €50bn €75bn 2023 2024 2025 European CLO Issuance (EUR) 2 European CLO Issuance (EUR) XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 14

European vs. U.S. CLO BB Spreads - 200 - 150 - 50 - 100 0 50 100 200 150 250 300 0 200 400 600 800 1,000 1,200 Difference (bps) Spread (bps) CLO BB Spreads: EUR 2.0 vs USD 3.0 (Secondary) Difference (EUR - USD) EUR 2.0 CLO BB Spread USD 3.0 CLO BB Spread Source: King Street. Note: Data as of 4/24/2026. Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 15

Your Vote Matters! Record Date: June 2, 2026 | Special Meetings: July 30, 2026 | Board recommends voting ” FOR ” the proposals H OW T O V OT E Y OU R S H AR E S Online Vote at the website listed on your proxy card and follow the on - screen instructions. By Phone Call the toll - free number on your proxy card to record your voting instructions. By Mail Complete, sign, date and return the enclosed proxy card in the postage - paid envelope. In Person Attend the Special Meeting on July 30, 2026, at the offices of the Funds’ investment adviser. Q U E S TI O N S ? Proxy Solicitation Agent - Okapi Partners LLC Toll - free: (855)305 - 0855 XA Investments Team Phone: (888)903 - 3358 Address: 321 N. Clark Street, Suite 2430, Chicago, IL 60654 Web: www.xainvestments.com XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 16 Shareholders as of June 2, 2026 are entitled to vote at the Special Meetings, which will be held on July 30, 2026, at the XA Investments offices.

XAInvestments.com | (888) 903 - 3358 321 North Clark Street Suite 2430 Chicago, IL 60654 Kevin Davis XA Investments Managing Director, Head of Sales & Distribution Kimberly Flynn, CFA XA Investments President kdavis@xainvestments.com (832) 752 - 4792 kflynn@xainvestments.com (312) 374 - 6931 Join Us for Our Next Webinar | August 4 th Contact Our Team with Questions XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 17

Investment in XFLT (referred to in this section as the “Trust”) involves special risk considerations, which are summarized below. The Trust is designed as a long - term investment and not as a trading vehicle. The Trust is not intended to be a complete investment program. The Trust’s performance and the value of its investments will vary in response to changes in interest rates, inflation and other market factors. Investors should see the “Risks” section in the Trust’s most recent Annual Report on Form N - CSR for a detailed discussion of factors investors should consider carefully before deciding to invest in the Trust. Investment and Market Risk. An investment in common shares of beneficial interest of the Trust (“Common Shares”) is subject to investment risk, including the possible loss of the entire principal amount that you invest. Your investment in Common Shares represents an indirect investment in the securities owned by the Trust. Your Common Shares at any point in time may be worth less than your original investment, even after taking into account the reinvestment of distributions. A prospective investor should invest in the Common Shares only if the investor can sustain a complete loss in its investment. Structured Credit Instruments Risk. Holders of structured credit instruments bear risks of the underlying investments, index or reference obligation as well as risks associated with the issuer of the instrument, which is often a special purpose vehicle, and may also be subject to counterparty risk. Below Investment Grade Securities Risk. The Trust intends to invest primarily in below investment grade credit instruments, which are commonly referred to as “high - yield” securities or “junk” bonds. Investment in securities of below investment grade quality involves substantial risk of loss. Securities of below investment grade quality are considered predominantly speculative with respect to the issuer’s capacity to pay interest and repay principal when due and therefore involve a greater risk of default or decline in market value due to adverse economic and issuer - specific developments. Issuers of below investment grade securities are not perceived to be as strong financially as those with higher credit ratings. These issuers face ongoing uncertainties and exposure to adverse business, financial or economic conditions and are more vulnerable to financial setbacks and recession than more creditworthy issuers, which may impair their ability to make interest and principal payments. Securities of below investment grade quality display increased price sensitivity to changing interest rates and to a deteriorating economic environment. The market values of certain below investment grade securities tend to reflect individual issuer developments to a greater extent than do higher - rated securities, which react primarily to fluctuations in the general level of interest rates. The market values for securities of below investment grade quality tend to be more volatile and such securities tend to be less liquid than investment grade debt securities, which could result in the Trust being unable to sell such securities for an extended period of time, if at all. To the extent that a secondary market does exist for certain below investment grade securities, the market for them may be subject to irregular trading activity, wide bid/ask spreads and extended trade settlement periods. Because of the substantial risks associated with investments in below investment grade securities, you could have an increased risk of losing money on your investment in Common Shares, both in the short - term and the long - term. To the extent that the Trust invests in below investment grade securities that are unrated, the Trust’s ability to achieve its investment objectives will be more dependent on the Sub - Adviser’s credit analysis than would be the case when the Trust invests in rated securities. Market Discount Risk. Shares of closed - end management investment companies frequently trade at a discount from their net asset value, which is a risk separate and distinct from the risk that the Trust’s net asset value could decrease as a result of its investment activities. Although the value of the Trust’s net assets is generally considered by market participants in determining whether to purchase or sell Common Shares, whether investors will realize gains or losses upon the sale of Common Shares will depend entirely upon whether the market price of Common Shares at the time of sale is above or below the investor’s purchase price for Common Shares. Because the market price of Common Shares will be determined by factors such as net asset value, dividend and distribution levels (which are dependent, in part, on expenses), supply of and demand for Common Shares, stability of dividends or distributions, trading volume of Common Shares, general market and economic conditions and other factors beyond the control of the Trust, the Trust cannot predict whether Common Shares will trade at, below or above net asset value or at, below or above the initial public offering price. This risk may be greater for investors expecting to sell their Common Shares soon after the completion of the public offering, as the net asset value of the Common Shares will be reduced immediately following the offering as a result of the payment of certain offering costs. Common Shares of the Trust are designed primarily for long - term investors; investors in Common Shares should not view the Trust as a vehicle for trading purposes. CLO Risk. CLOs often involve risks that are different from or more acute than risks associated with other types of credit instruments. For instance, due to their often complicated structures, various CLOs may be difficult to value and may constitute illiquid investments. In addition, there can be no assurance that a liquid market will exist in any CLO when the Trust seeks to sell its interest therein. Moreover, the value of CLOs may decrease if the ratings agencies reviewing such securities revise their ratings criteria and, as a result, lower their original rating of a CLO in which the Trust has invested. Restructuring of Investments Held by CLOs. The manager of a CLO has broad authority to direct and supervise the investment and reinvestment of the investments held by the CLO, which may include the execution of amendments, waivers, modifications and other changes to the investment documentation in accordance with the collateral management agreement. During periods of economic uncertainty and recession, the incidence of amendments, waivers, modifications and restructurings of investments may increase. Such amendments, waivers, modifications and other restructurings will change the terms of the investments and in some cases may result in the CLO holding assets not meeting its criteria for investments. This could adversely impact the coverage tests under an indenture governing the notes issued by the CLO. If as a result of any such restructurings, the Trust’s investment sub - adviser (the “Sub - Adviser”) determines that continuing to hold instruments issued by such CLO is no longer in the best interest of the Trust, the Sub - Adviser may dispose of such CLO instruments. In certain instances, the Trust may be unable to dispose of such investments at advantageous prices and/or may be required to reinvest the proceeds of such disposition in lower - yielding investments. CLO Management Risk. The activities of any CLO in which the Trust may invest will generally be directed by a collateral manager. In the Trust’s capacity as holder of subordinated notes, the Trust is generally not able to make decisions with respect to the management, disposition or other realization of any investment, or other decisions regarding the business and affairs, of that CLO. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 18 XFLT Risk Considerations

CLO Subordinated Note Risk. The Trust may invest in subordinated notes issued by a CLO, which are junior in priority of payment and are subject to certain payment restrictions generally set forth in an indenture governing the notes. In addition, they generally have only limited voting rights and generally do not benefit from any creditors’ rights or ability to exercise remedies under the indenture governing the notes. The subordinated notes are not guaranteed by another party. The subordinated notes are unsecured and rank behind all of the secured creditors, known or unknown, of the issuer, including the holders of the secured notes it has issued. Consequently, to the extent that the value of the issuer’s portfolio of loan investments has been reduced as a result of conditions in the credit markets, defaulted loans, capital gains and losses on the underlying assets, prepayment or changes in interest rates, the value of the subordinated notes realized at their redemption could be reduced. Accordingly, the subordinated notes may not be paid in full and may be subject to up to 100% loss. Subordinated notes are subject to greater risk that the senior notes issued by the CLO. CLO subordinated notes do not have a fixed coupon and payments on CLO subordinated notes will be based on the income received from the underlying collateral and the payments made to the secured notes, both of which may be based on floating notes. While payments on CLO subordinated notes will vary, CLO subordinated notes may not offer the same level of protection against changes in interest rates as other floating - rate instruments. Subordinated notes are illiquid investments and subject to extensive transfer restrictions, and no party is under any obligation to make a market for subordinated notes. Corporate Credit Investments Risk. Corporate debt instruments pay fixed, variable or floating rates of interest. The value of fixed - income securities in which the Trust invests will change in response to fluctuations in interest rates. In addition, the value of certain fixed - income securities can fluctuate in response to perceptions of creditworthiness, political stability or soundness of economic policies. Fixed - income securities are subject to the risk of the issuer’s inability to meet principal and interest payments on its obligations (i.e., credit risk) and are subject to price volatility due to such factors as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity (i.e., market risk). Senior Loan Risk. Senior Loans are generally of below investment grade credit quality and are subject to greater risks than investment grade corporate obligations. The prices of these investments may be volatile and will generally fluctuate due to a variety of factors that are inherently difficult to predict, including, but not limited to, changes in interest rates, prevailing credit spreads, general economic conditions, financial market conditions, U.S. and non - U.S. economic or political events, developments or trends in any particular industry, and the financial condition of certain borrowers. Second Lien Loans Risk. Second lien loans are secured by liens on the collateral securing the loan that are subordinated to the liens of at least one other class of obligations of the related obligor, and thus, the ability of the Trust to exercise remedies after a second lien loan becomes a defaulted loan is subordinated to, and limited by, the rights of the senior creditors holding such other classes of obligations. In many circumstances, the Trust may be prevented from foreclosing on the collateral securing a second lien loan until the related senior loan is paid in full. Unsecured Loan Risk. Unsecured loans do not benefit from any security interest in the assets of the borrower. Liens on such borrowers’ assets, if any, will secure the applicable borrower’s obligations under its outstanding secured indebtedness and may secure certain future indebtedness that is permitted to be incurred by the borrower under its secured loan agreements. The holders of obligations secured by such liens will generally control the liquidation of, and be entitled to receive proceeds from, any realization of such collateral to repay their obligations in full before unsecured instruments held by the Trust. In addition, the value of such collateral in the event of liquidation will depend on market and economic conditions, the availability of buyers and other factors. There can be no assurance that the proceeds, if any, from sales of such collateral would be sufficient to satisfy the Trust’s unsecured obligations after payment in full of all secured loan obligations of the borrower. If such proceeds were not sufficient to repay the borrower’s outstanding secured loan obligations, then the Trust’s unsecured claims against the borrower would rank equally with the unpaid portion of such secured creditors’ claims against the borrower’s remaining assets, if any. As a result, the prices of unsecured loans may be more volatile than those of senior loans, second lien and other secured loans and other investments held by the Trust. Loan Participation and Assignment Risk . The Trust may purchase senior loans, second lien loans and unsecured loans on a direct assignment basis from a participant in the original syndicate of lenders or from subsequent assignees of such interests. The Trust may also purchase, without limitation, participations in senior loans, second lien loans and unsecured loans. The purchaser of an assignment typically succeeds to all the rights and obligations of the assigning institution and becomes a lender under the credit agreement with respect to the debt obligation; however, the purchaser’s rights can be more restricted than those of the assigning institution, and, in any event, the Trust may not be able to unilaterally enforce all rights and remedies under the loan and with regard to any associated collateral. A participation typically results in a contractual relationship only with the institution participating out the interest, not with the borrower. In purchasing participations, the Trust generally will have no right to enforce compliance by the borrower with the terms of the loan agreement against the borrower, and the Trust may not directly benefit from the collateral supporting the debt obligation in which it has purchased the participation. As a result, the Trust will be exposed to the credit risk of both the borrower and the institution selling the participation. Further, in purchasing participations in lending syndicates, the Trust may not be able to conduct the same due diligence on the borrower with respect to a loan hat the Trust would otherwise conduct. In addition, as a holder of the participations, the Trust may not have voting rights or inspection rights that the Trust would otherwise have if it were investing directly in the loan, which may result in the Trust being exposed to greater credit or fraud risk with respect to the borrower. Illiquid Investments Risk. The Trust expects to invest in restricted, as well as thinly traded, instruments and securities (including privately placed securities and instruments, which are assets which are subject to Rule 144A. There may be no trading market for these securities and instruments, and the Trust might only be able to liquidate these positions, if at all, at disadvantageous prices. Stressed and Distressed Investments Risk. The Trust may invest in stressed and distressed securities. The ability of the Trust to obtain a profit from these investments may often depend upon factors that are intrinsic to the particular issuer, rather than the market as a whole. Appreciation in the value of such securities may be contingent upon the occurrence of certain events, such as a successful reorganization or merger. If the expected event does not occur, the Trust may incur a loss on the position. Distressed securities may have a limited trading market, resulting in limited liquidity and presenting difficulties to the Trust in valuing its positions. Due to the illiquid nature of many distressed investments, as well as the uncertainties of the reorganization and active management process, the Sub - Adviser may be unable to predict with confidence what the exit strategy will ultimately be for any given position, or that one will definitely be available. Certain distressed investment opportunities may allow a holder to have significant influence on the management, operations and strategic direction of the portfolio companies in which it invests. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 19 XFLT Risk Considerations (cont.)

Leverage Risk. The Trust uses leverage to seek to enhance total return and income. The Trust may use leverage through (i) the issuance of senior securities representing indebtedness, including through borrowing from financial institutions or issuance of debt securities, including notes or commercial paper (collectively, “Indebtedness”), (ii) the issuance of preferred shares (“Preferred Shares”) and/or (iii) reverse repurchase agreements, securities lending, short sales or derivatives, such as swaps, futures or forward contracts, that have the effect of leverage (“portfolio leverage”). The Trust may utilize leverage to the maximum extent permitted under the Investment Company Act of 1940. The Trust has entered into a revolving credit facility and any borrowings through the credit facility are secured by eligible securities held in the Trust’s portfolio of investments. The Trust has also issued preferred shares, which are senior securities that constitute shares of beneficial interest of the Trust. Preferred shares rank senior to the Trust’s Common Shares in priority of payment of dividends and as to the distribution of assets upon dissolution, liquidation or winding up of the Trust’s affairs; equal in priority with all other future series of preferred shares the Trust may issue as to priority of payment of dividends and as to distributions of assets upon dissolution, liquidation or the winding - up of the Trust’s affairs; and subordinate in right of payment to amounts owed under the Trust’s existing credit facility, and to the holder of any future senior indebtedness, which may be issued without the vote or consent of preferred shareholders. The use of leverage is a speculative technique that involves special risks. The Trust currently anticipates utilizing leverage to seek to enhance total return and income. There can be no assurance that the Adviser’s and the Sub - Adviser’s expectations will be realized or that a leveraging strategy will be successful in any particular time period. Use of leverage creates an opportunity for increased income and capital appreciation but, at the same time, creates special risks. Leverage is a speculative technique that exposes the Trust to greater risk and increased costs than if it were not implemented. The more leverage that is utilized by the Trust, the more exposed the Trust will be to the risks of leverage. The use of leverage by the Trust causes the net asset value of the common shares to fluctuate significantly in response to changes in interest rates and other economic indicators. As a result, the net asset value, market price and dividend rate of the common shares is likely to be more volatile than those of a fund that is not exposed to leverage. Leverage increases operating costs, which may reduce total return. The Trust pays interest on its borrowings, which may reduce the Trust’s return. Increases in interest rates that the Trust must pay on its borrowings will increase the cost of leverage and may reduce the return to common shareholders. The risk of increases in interest rates may be greater in the current market environment because interest rates are near historically low levels. During the time in which the Trust is utilizing leverage, the amount of the investment advisory fee paid by the Trust will be higher than if the Trust did not utilize leverage because the fees paid will be calculated based on the Trust’s Managed Assets, including proceeds of leverage. Common shareholders bear the portion of the management fee attributable to assets purchased with the proceeds of leverage, which means that common shareholders effectively bear the entire management fee. Other Investment Companies Risk. Investments in other investment companies present certain special considerations and risks not present in making direct investments in securities in which the Trust may invest. Investments in other investment companies involve operating expenses and fees that are in addition to the expenses and fees borne by the Trust. Such expenses and fees attributable to the Trust’s investments in other investment companies are borne indirectly by common shareholders. Accordingly, investment in such entities involves expense and fee layering. Exchange - Traded Fund Risk. For ETFs tracking an index of securities, the cumulative percentage increase or decrease in the net asset value of the shares of an ETF may over time diverge significantly from the cumulative percentage increase or decrease in the relevant index due to the compounding effect experienced by an ETF which results from a number of factors, including, leverage (if applicable), daily rebalancing, fees, expenses and interest income, which in turn results in greater non - correlation between the return of an ETF and its corresponding index. Short Sales Risk. Short sales involve selling securities of an issuer short in the expectation of covering the short sale with securities purchased in the open market at a price lower than that received in the short sale. If the price of the issuer’s securities declines, the Trust may then cover the short position with securities purchased in the market. The profit realized on a short sale will be the difference between the price received in the sale and the cost of the securities purchased to cover the sale. The possible losses from selling short a security differ from losses that could be incurred from a cash investment in the security; the former may be unlimited, whereas the latter can only equal the total amount of the cash investment. Short selling activities are also subject to restrictions imposed by the federal securities laws and the various national and regional securities exchanges, which restrictions could limit the Trust’s investment activities. There can be no assurance that securities necessary to cover a short position will be available for purchase. Derivatives Risk. Derivatives are financial contracts in which the value depends on, or is derived from, the value of an underlying asset, reference rate or index. The Trust may, but is not required to, engage in various derivatives transactions for hedging and risk management purposes, to facilitate portfolio management and to seek to enhance total return of earn income. The Trust’s use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments. Derivatives are subject to a number of risks, such as interest rate risk, market risk, counterparty risk, and credit risk. Off - Exchange Derivatives Risk . The Trust may invest a portion of its assets in investments which are not traded on organized exchanges and as such are not standardized . Such transactions may include forward contracts, swaps or options . While some markets for such derivatives are highly liquid, transactions in off - exchange derivatives may involve greater risk than investing in exchange - traded derivatives because there is no exchange market on which to close out an open position . Options Risk . Trading in options involves a number of risks . Specific market movements of the option and the instruments underlying an option cannot be predicted . No assurance can be given that a liquid offset market will exist for any particular option or at any particular time . If no liquid offset market exists, the Trust might not be able to effect an offsetting transaction in a particular option . Futures Risk. Futures contracts markets are highly volatile and are influenced by a variety of factors, including national and international political and economic developments. In addition, because of the low margin deposits normally required in futures trading, a high degree of leverage is typical of a futures trading account. As a result, a relatively small price movement in a futures contract may result in substantial losses to the trader. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 20 XFLT Risk Considerations (cont.)

Swaps Risk. The Trust may utilize swap agreements including, without limitation, interest rate, index and currency swap agreements. The use of swaps is a highly specialized activity that involves investment techniques and risks different from those associated with ordinary securities transactions. There are risks relating to the financial soundness and creditworthiness of the counterparty to swap agreements. Credit Default Swaps Risk. The Trust may enter into credit default swap agreements. The “buyer” in a credit default contract is obligated to pay the “seller” a periodic stream of payments over the term of the contract provided that no event of default on an underlying reference obligation has occurred. The Trust may be either the buyer or seller in a credit default swap transaction. Credit default swap transactions involve greater risks than if a Trust had invested in the reference obligation directly. Credit default swaps are subject to the risk of non - performance by the swap counterparty, including risks relating to the financial soundness and creditworthiness of the swap counterparty. Hedging Transactions Risk. The success of any hedging strategy utilized by the Trust’s will be subject to the Sub - Adviser’s ability to correctly assess the degree of correlation between the performance of the instruments used in the hedging strategy and the performance of the investments in the portfolio being hedged. Since the characteristics of many securities change as markets change or time passes, the success of the Trust’s hedging strategy will also be subject to the Sub - Adviser’s ability to continually recalculate, readjust, and execute hedges in an efficient and timely manner. Counterparty Risk. The Trust will be subject to credit risk with respect to the counterparties to the derivative contracts entered into by the Trust. Synthetic Investment Risk . The Trust may be exposed to certain additional risks should the Sub - Adviser uses derivatives transactions as a means to synthetically implement the Trust’s investment strategies . Customized derivative instruments will likely be highly illiquid, and it is possible that the Trust will not be able to terminate such derivative instruments prior to their expiration date or that the penalties associated with such a termination might impact the Trust’s performance in a materially adverse manner . Segregation and Cover Risk. In connection with certain derivatives transactions, the Trust may be required to segregate liquid assets or otherwise cover such transactions and/or to deposit amounts as premiums or to be held in margin accounts. Such amounts may not otherwise be available to the Trust for investment purposes. The Trust may earn a lower return on its portfolio than it might otherwise earn if it did not have to segregate assets in respect of, or otherwise cover, its derivatives transactions positions. Interest Rate Risk. Interest rate risk is the risk that credit securities will decline in value because of changes in market interest rates. When market interest rates rise, the market value of fixed income credit securities generally will fall. These risks may be greater in the current market environment because while interest rates were historically low in recent years, the Federal Reserve has been increasing the Federal Funds rate to address inflation. Prevailing interest rates may be adversely impacted by market and economic factors. If interest rates rise the markets may experience increased volatility, which may adversely affect the value and/or liquidity of certain of the Trust’s investments. The prices of longer - term securities fluctuate more than prices of shorter - term securities as interest rates change. The Trust’s use of leverage will tend to increase the interest rate risk to which its Common Shares are subject. The Trust invests primarily in variable and floating rate credit instruments and other structured credit investments, which generally are less sensitive to interest rate changes than fixed rate instruments, but generally will not increase in value if interest rates decline. Prepayment Risk. The frequency at which prepayments (including voluntary prepayments by the obligors and accelerations due to defaults) occur on bonds and loans will be affected by a variety of factors including the prevailing level of interest rates and spreads as well as economic, demographic, tax, social, legal and other factors. The adverse effects of prepayments may impact the Trust’s portfolio in several ways. During periods of declining interest rates, when the issuer of a security exercises its option to prepay principal earlier than scheduled, the Trust may be required to reinvest the proceeds of such prepayment in lower - yielding securities. Particular investments may experience outright losses, as in the case of an interest - only security in an environment of faster actual or anticipated prepayments. In addition, particular investments may underperform relative to hedges that the Sub - Adviser may have constructed for these investments, resulting in a loss to the Trust’s overall portfolio. Inflation/Deflation Risk. Inflation risk is the risk that the value of assets or income from investments will be worth less in the future as inflation decreases the value of money. As inflation increases, the real value of the Common Shares and distributions can decline. Deflation risk is the risk that prices throughout the economy decline over time — the opposite of inflation. Deflation may have an adverse effect on the creditworthiness of issuers and may make issuer default more likely, which may result in a decline in the value of the Trust’s portfolio. Duration and Maturity Risk. The Trust has no set policy regarding maturity or duration of credit instruments in which it may invest or of the Trust’s portfolio generally. The price of fixed rate securities with longer maturities or duration generally is more significantly impacted by changes in interest rates than those of fixed rate securities with shorter maturities or duration. Therefore, generally speaking, the longer the duration of the Trust’s portfolio, the more exposure the Trust will have to interest rate risk described above. The Sub - Adviser may seek to adjust the portfolio’s duration or maturity based on its assessment of current and projected market conditions and all factors that the Sub - Adviser deems relevant. The Trust may incur costs in seeking to adjust the portfolio average duration or maturity. There can be no assurance that the Sub - Adviser’s assessment of current and projected market conditions will be correct or that any strategy to adjust the portfolio’s duration or maturity will be successful at any given time. Credit Risk. Credit risk is the risk that an issuer of securities will be unable to pay principal and interest when due, or that the value of the security will suffer because investors believe the issuer is less able to pay. Non - U.S. Investments Risk. The risk of loss associated with investments in securities of foreign issuers include currency exchange risks, expropriation, or limits on repatriating an investment, government intervention, confiscatory taxation, political, economic or social instability, illiquidity, less efficient markets, price volatility and market manipulation. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 21 XFLT Risk Considerations (cont.)

Equity Investments Risk. Incidental to the Trust’s investments in credit instruments, the Trust may acquire or hold equity securities, or warrants to purchase equity securities, of a borrower or issuer. Common equity securities prices fluctuate for a number of reasons, including changes in investors’ perceptions of the financial condition of an issuer, the general condition of the relevant stock market and broader domestic and international political and economic events. European CLO Risks. European CLOs are not denominated in U.S. dollars and primarily hold loans to non - U.S. companies. Investing in securities of non - U.S. issuers may involve certain risks not typically associated with investing in securities of U.S. issuers. These risks include: (i) there may be less publicly available information about non - U.S. issuers or markets due to less rigorous disclosure or accounting standards or regulatory practices; (ii) non - U.S. markets may be smaller, less liquid and more volatile than the U.S. market; (iii) potential adverse effects of fluctuations in currency exchange rates or controls on the value of the Trust’s investments; (iv) the economies of non - U.S. countries may grow at slower rates than expected or may experience a downturn or recession; (v) the impact of economic, political, social or diplomatic events as well as of foreign governmental laws or restrictions and differing legal standards; (vi) certain non - U.S. countries may impose restrictions on the ability of non - U.S. issuers to make payments of principal and interest to investors located in the United States due to blockage of non - U.S. currency exchanges or otherwise; and (vii) withholding and other non - U.S. taxes. Foreign companies are generally not subject to the same accounting, auditing and financial reporting standards as are U.S. companies. In addition, there may be difficulty in obtaining or enforcing a court judgment abroad, including in the event the issuer of a non - U.S. security defaults or enters bankruptcy, administration, or other proceedings. Changes in the non - U.S. currency/United States dollar exchange rate may affect the value of non - U.S. dollar - denominated securities and the unrealized appreciation or depreciation of investments. While certain or all of the Trust’s non - U.S. dollar - denominated securities may be hedged into U.S. dollars, hedging may not alleviate all currency risks. Forward foreign currency exchange contracts involve certain risks, including the risk of failure of the counterparty to perform its obligations under the contract and the risk that the use of forward contracts may not serve as a complete hedge because of an imperfect correlation between movements in the prices of the contracts and the prices of the currencies hedged. While forward foreign currency exchange contracts may limit the risk of loss due to a decline in the value of the hedged currencies, they also may limit any potential gain that might result should the value of the currencies increase. In addition, because forward currency exchange contracts are privately negotiated transactions, there can be no assurance that the Trust will have flexibility to roll - over a forward currency exchange contract upon its expiration if it desires to do so. Hedging against a decline in the value of a currency does not eliminate fluctuations in the value of a portfolio security traded in that currency or prevent a loss if the value of the security declines. Moreover, it may not be possible for the Trust to hedge against a devaluation that is so generally anticipated that the Trust is not able to contract to sell the currency at a price above the devaluation level it anticipates. The cost to the Trust of engaging in currency exchange transactions varies with such factors as the currency involved, the length of the contract period and prevailing market conditions. Political or economic disruptions in European countries may adversely affect security values. A significant number of countries in Europe are member states in the European Union (the “EU”), which faces major issues involving its membership, structure, procedures and policies. By adopting the Euro as its currency, a member state relinquishes control over its own monetary policies. In general, monetary policy is set for the Eurozone by the European Central Bank and fiscal policy is overseen and approved by the EU. European countries that are members of, or candidates to join, the Economic and Monetary Union (“EMU”) may be subject to various restrictions, including restrictions on deficits and debt levels. As a result of the foregoing, monetary and fiscal policies may not address the needs of all member countries. In addition, the fiscal policies of a single member state can impact and pose economic risks to the EU as a whole. There is continued concern over national - level support for the Euro, which could lead to certain countries leaving the EMU, the implementation of capital controls, or potentially the dissolution of the Euro. The dissolution of the Euro would have significant negative effects on European economies and would cause funds with holdings denominated in Euros to face substantial challenges, including difficulties relating to settlement of trades and valuation of holdings, diminished liquidity, and the redenomination of holdings into other currencies. The European financial markets have experienced volatility and adverse trends due to concerns about economic downturns, rising government debt levels and the possible default of government debt in several European countries. A default or debt restructuring by any European country can adversely impact holders of that country’s debt and can affect exposures to other EU countries and their financial companies as well. Portfolio Turnover Risk. The Trust may engage in active and frequent trading of its portfolio securities. High portfolio turnover may result in increased transaction costs to the Trust, including brokerage commissions, dealer mark - ups and other transaction costs on the sale of securities and on reinvestment in other securities. The sale of portfolio securities may result in the realization and/or distribution to shareholders of higher capital gains or losses as compared to a fund with less active trading policies. These effects of higher than normal portfolio turnover may adversely affect Trust performance. Asset Backed Securities Risks. Asset - backed securities are a form of structured debt obligation. ABS are payment claims that are securitized in the form of negotiable paper that is issued by a financing company (generally called a special purpose vehicle). Collateral assets are brought into a pool according to specific diversification rules. A special purpose vehicle is founded for the purpose of securitizing these payment claims and the assets of the special purpose vehicle are the diversified pool of collateral assets. The special purpose vehicle issues marketable securities that are intended to represent a lower level of risk than an underlying collateral asset individually, due to the diversification in the pool. The redemption of the securities issued by the special purpose vehicle takes place out of the cash flow generated by the collected assets. A special purpose vehicle may issue multiple securities with different priorities to the cash flows generated and the collateral assets. The collateral for ABS may include, among other assets, home equity loans, automobile and credit card receivables, boat loans, computer leases, airplane leases, mobile home loans, recreational vehicle loans and hospital account receivables. The Trust may invest in these and other types of ABS that may be developed in the future. There is the possibility that recoveries on the underlying collateral may not, in some cases, be available or may be insufficient to support payments on these securities. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 22 XFLT Risk Considerations (cont.)

Asset Backed Securities Risks (cont.). The Trust may invest in ABS issued by legal entities that are sponsored by banks, investment banks, other financial institutions or companies, asset management firms or funds and are specifically created for the purpose of issuing such ABS. Investors in ABS receive payments that are part interest and part return of principal or certain ABS may be interest - only securities or principal - only securities. These payments typically depend upon the cash flows generated by an underlying pool of assets and vary based on the rate at which the underlying obligors pay off their liabilities under the underlying assets. The pooled assets provide cash flow to the issuer, which then makes interest and principal payments to investors. As a result, these investments involve the risk, among other risks, that the borrower may default on its obligations backing the ABS and, thus, the value of and interest generated by such investment will decline. In addition to the general risks (such as interest rate risk, prepayment risk, extension risk, market risk, credit risk and liquidity and valuation risk) associated with credit or debt securities discussed herein, ABS are subject to additional risks due to their structure. During periods of declining interest rates, prepayment of borrowings underlying asset - backed securities can be expected to accelerate. Accordingly, the Trust’s ability to reinvest the returns of principal at comparable yields is subject to generally prevailing interest rates at that time. ABS are also subject to liquidity and valuation risk and, therefore, may be difficult to value accurately or sell at an advantageous time or price and involve greater transaction costs and wider bid/ask spreads than certain other instruments. In addition, the assets or collateral underlying an ABS may be insufficient or unavailable in the event of a default and enforcing rights with respect to these assets or collateral may be difficult and costly. While traditional fixed - income securities typically pay a fixed rate of interest until maturity, when the entire principal amount is due, an ABS represents an interest in a pool of assets that has been securitized and typically provides for monthly or quarterly payments of interest, at a fixed or floating rate, and may provide for payments of principal from the cash flow of these assets. This pool of assets (and any related assets of the issuing entity) is often the only source of payment for the ABS. The ability of an ABS issuer to make payments on the ABS, and the timing of such payments, is therefore dependent on collections on these underlying assets. The recoveries on the underlying collateral may not, in some cases, be sufficient to support payments on these securities, or may be unavailable in the event of a default and enforcing rights with respect to these assets or collateral may be difficult and costly, which may result in losses to investors in an ABS. Generally, obligors may prepay the underlying assets in full or in part at any time, subjecting the Trust to prepayment risk related to the ABS it holds. While the expected repayment streams on ABS are determined by the contractual amortization schedules for the underlying assets, an investor’s yield to maturity on an ABS is uncertain and may be reduced by the rate and speed of prepayments of the underlying assets, which may be influenced by a variety of economic, social and other factors. Any prepayments, repurchases, purchases or liquidations of the underlying assets could shorten the average life of the ABS to an extent that cannot be fully predicted. Some ABS may be structured to include a period of rapid amortization triggered by events such as a significant rise in the default rate of the underlying collateral, a sharp drop in the credit enhancement level because of credit losses on the underlying assets, a specified regulatory event or the bankruptcy of the originator. A rapid amortization event will cause any revolving period to end earlier than expected and all collections on the underlying assets will be used to pay principal to investors earlier than expected. In general, the senior most securities will be paid prior to any payments being made on the subordinated securities, and if such payments are made earlier than expected, the Trust’s yield on such ABS may be negatively affected. In addition, investments in ABS entail additional risks relating to the underlying pools of assets, including credit risk, default risk (such as a borrower’s default on its obligation and the default, failure or inadequacy or unavailability of a guarantee, if any, underlying the ABS intended to protect investors in the event of default) and prepayment and extension risk with respect to the underlying pool or individual assets represented in the pool . The underlying assets of an ABS may include, without limitation, residential or commercial mortgages, motor vehicle installment sales or installment loan contracts, leases of various types of real, personal and other property, receivable from credit card agreements and automobile finance agreements, student loans, consumer loans, and income from other income streams, such as income from business loans . Moreover, additional risks relating to investments in ABS may arise principally because of the type of ABS in which the Trust invests, with such risks primarily associated with the particular assets collateralizing the ABS (such as their type or nature), the structure of such ABS, or the tranche or priority of the ABS held by the Trust (with junior or equity tranches generally carrying higher levels of risk) Mortgage - Backed Securities (“MBS”) represent an interest in a pool of mortgages. MBS are subject to certain risks, such as: credit risk associated with the performance of the underlying mortgage properties and of the borrowers owning these properties; risks associated with their structure and execution (including the collateral, the process by which principal and interest payments are allocated and distributed to investors and how credit losses affect the return to investors in such MBS); risks associated with the servicer of the underlying mortgages; adverse changes in economic conditions and circumstances, which are more likely to have an adverse impact on MBS secured by loans on certain types of commercial properties than on those secured by loans on residential properties; prepayment and extension risks associated with the underlying assets of certain MBS, which can shorten the weighted average maturity and lower the return of the MBS, or lengthen the expected maturity, respectively, leading to significant fluctuations in the value of the MBS; loss of all or part of the premium, if any, paid; and decline in the market value of the security, whether resulting from changes in interest rates, prepayments on the underlying mortgage collateral or perceptions of the credit risk associated with the underlying mortgage collateral. The value of MBS may be substantially dependent on the servicing of the underlying pool of mortgages. In addition, the Trust’s level of investment in MBS of a particular type or in MBS issued or guaranteed by affiliated obligors, serviced by the same servicer or backed by underlying collateral located in a specific geographic region, may subject the Trust to additional risk. XA INVESTMENTS LLC | XFLT & OCTIX Shareholder Proposals and Portfolio Manager Introduction June 30, 2026 | 23 XFLT Risk Considerations (cont.)