As

confidentially submitted to the Securities and Exchange Commission on August 6, 2025.

This draft registration statement has not been publicly filed with the Securities and Exchange Commission and all information herein

remains strictly confidential.

Registration No. 333-

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Confidential Draft Submission No. 2

FORM S-11

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Fermi LLC

to be converted as described herein to a corporation named

Fermi Inc.

(Exact name of registrant as specified in its charter)

| Texas | 6798 | 33-3560468 | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (IRS Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

600

S. Tyler St.

Suite 1501

Amarillo, TX 79101

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Toby R. Neugebauer

Chief Executive Officer

600

S. Tyler St.

Suite 1501

Amarillo, TX 79101

214-894-7855

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Matthew L. Fry, Esq. Logan J. Weissler, Esq. Haynes and Boone, LLP 2801 N. Harwood Street, Suite 2300 Dallas, Texas 75201 (214) 651-5000 |

Daniel M. LeBey Vinson & Elkins L.L.P. Riverfront Plaza, West Tower 901 East Byrd Street, Suite 1500 Richmond, Virginia 23219 (804) 327-6300 |

David P. Oelman Vinson & Elkins L.L.P. Texas Tower 845 Texas Avenue, Suite 4700 Houston, Texas 77002 (713) 758-2222 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☒

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

Prior to the effectiveness of this registration statement, Fermi LLC intends to convert into a Texas corporation pursuant to a statutory conversion and change its name to Fermi Inc. as described in the section “Corporate Conversion” of the accompanying prospectus. In the accompanying prospectus, we refer to all of the transactions related to our conversion to a corporation as the Corporate Conversion. Unless the context otherwise requires, all references in the accompanying prospectus to the “Company,” “Fermi,” “we,” “us,” “our” or similar terms refer to Fermi LLC and its subsidiaries before the Corporate Conversion, and Fermi Inc. and, where appropriate, its subsidiaries after the Corporate Conversion. Except as disclosed in the prospectus, the financial statements and other financial information included in this registration statement are those of Fermi LLC and its subsidiaries and do not give effect to the Corporate Conversion. Shares of Common Stock of Fermi Inc. are being offered by the accompanying prospectus.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED , 2025.

PRELIMINARY PROSPECTUS

Shares

![]()

Fermi Inc.

Common Stock

This is Fermi Inc.’s initial public offering of its common stock (“Common Stock”). We are offering shares of our Common Stock, and the Selling Shareholders (as defined below) identified in this prospectus are offering shares of Common Stock, for an aggregate of shares of Common Stock being sold by us and the Selling Shareholders in this offering. We will not receive any proceeds from the sale of shares of Common Stock by the Selling Shareholders. Prior to this offering, there has been no public market for our Common Stock. We expect that the initial public offering price of our Common Stock will be between $ and $ per share. We intend to apply to list our Common Stock on the Nasdaq Global Select Market (“Nasdaq”) under the symbol “FRMI.” Additionally, we intend to apply to list our Common Stock on the main market of the London Stock Exchange plc (the “London Stock Exchange”) under the symbol “[ ● ].”

See “Risk Factors” beginning on page 26 to read about factors you should consider before buying shares of our Common Stock.

We intend to elect to qualify to be taxed as a real estate investment trust (“REIT”) under the Internal Revenue Code of 1986, as amended (the “Code”), commencing with our short taxable year ending December 31, 2025, as further described herein. We believe that we are organized and operate in a manner to qualify for taxation as a REIT for U.S. federal income tax purposes. We intend to continue to be organized and operate as a REIT in the future. Shares of our capital stock (including our Common Stock) will be subject to limitations on ownership and transfer that are primarily intended to assist us in maintaining our qualification as a REIT. Subject to certain exceptions, our certificate of formation (“Charter”) will restrict the direct or indirect ownership by one person or entity to no more than % of the value of our then outstanding shares of capital stock and no more than % of the value or number of shares, whichever is more restrictive, of our then outstanding shares of Common Stock. See “Description of Capital Stock—Restrictions on Ownership and Transfer” for a detailed description of the ownership and transfer restrictions applicable to our Common Stock.

Upon completion of this offering and the related corporate conversion, holders of shares of our Common Stock will be entitled to one vote for each share of Common Stock, respectively, held of record on all matters on which shareholders are entitled to vote generally. See “Description of Capital Stock.” We currently operate as a Texas limited liability company under the name Fermi LLC. In connection with this offering, we will consummate the transactions described under the heading “Corporate Conversion” in which Fermi LLC will convert into a Texas corporation pursuant to a statutory conversion and change its name to Fermi Inc. See “Corporate Conversion.”

We are an “emerging growth company” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements in future reports after the closing of this offering. See the section titled “Prospectus Summary—Implications of Being an Emerging Growth Company.”

Neither the Securities and Exchange Commission (“SEC”) nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial public offering price | $ | $ | ||||||

| Underwriting discount and commissions(1) | $ | $ | ||||||

| Proceeds, before expenses, to us | $ | $ | ||||||

| Proceeds, before expenses, to the Selling Shareholders | $ | $ | ||||||

| (1) | See “Underwriting” for additional information regarding underwriting compensation. |

(the “Selling Shareholders”) have granted the underwriters the option, for a period of 30 days, to purchase up to additional shares of Common Stock from them at the initial price to the public less the underwriting discount and commissions. We will not receive any proceeds from the sale of Common Stock by the Selling Shareholders resulting from any exercise of this option by the underwriters.

The underwriters expect to deliver the shares of Common Stock against payment in New York, New York on or about , 2025.

Joint Book-Running Managers

| Cantor | Mizuho |

Prospectus dated , 2025

TABLE OF CONTENTS

Neither we, the Selling Shareholders nor the underwriters have authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we and the underwriters have prepared. We, the Selling Shareholders and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We, the Selling Shareholders and the underwriters are offering to sell shares of Common Stock and seeking offers to buy shares of Common Stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of the Common Stock. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside of the United States: Neither we, the Selling Shareholders nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus or any free writing prospectus we may provide to you in connection with this offering in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside of the United States who come into possession of this prospectus and any free writing prospectus must inform themselves about and observe any restrictions relating to this offering and the distribution of this prospectus outside of the United States.

Through and including , 2025 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This requirement is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

| i |

COMMONLY USED DEFINED TERMS

As used in this prospectus, unless the context indicates or otherwise requires, the terms listed below have the following meanings:

| ● | “we,” “us,” “our,” the “Company,” “Fermi Inc.,” “Fermi” and similar references refer: (i) following the consummation of the Corporate Conversion, to Fermi Inc., and, unless otherwise stated, all of its direct and indirect subsidiaries and (ii) prior to the completion of the Corporate Conversion, to Fermi LLC. |

| ● | “BESS” means Battery Energy Storage System. |

| ● | “behind-the-meter” means electric power generation, including thermal generation, solar and other renewables and battery energy storage systems, that is installed on-site of a customer or end user’s data center operations to supply the load directly, rather than the customer being dependent on power supplied by the electric grid. |

| ● | “Class A Unit” means Class A units of Fermi LLC. |

| ● | “Class B Unit” means Class B units of Fermi LLC. |

| ● | “Code” means the Internal Revenue Code of 1986, as amended. |

| ● | “COL Application” means Fermi’s Combined License Application filed with the NRC on June 18, 2025 relating to the application for approval of new Westinghouse nuclear reactors to be constructed in connection with Project Matador. |

| ● | “combined cycle generation” means an efficient mode of generating thermally derived electric power, where a fuel, in our case natural gas, is combusted in a gas turbine to directly turn the blades in the gas turbine, producing the first stage of electric power via the gas turbine generator. Instead of venting or otherwise dispersing the hot exhaust, the waste heat emanating from this initial cycle is directed to a heat recovery steam generator, with the heat used to produce steam. This steam from the secondary cycle then becomes the motive force to drive a steam turbine, which generates a secondary volume of electricity via a steam turbine generator. |

| ● | “Convertible Notes” refers to, collectively the Seed Convertible Notes, the Series A Convertible Notes and the Series B Convertible Note. |

| ● | “Convertible Notes Conversion” refers to the automatic conversion of the Convertible Notes, plus accrued interest (if any), into an aggregate of shares of our Common Stock immediately prior to the completion of this offering, assuming an initial public offering price of $ per share (which is the midpoint of the price range set forth on the cover page of this prospectus). |

| ● | “Corporate Conversion” refers to all of the transactions related to Fermi LLC’s conversion from a Texas limited liability company to a Texas corporation, which will occur prior to the effectiveness of the registration statement of which this prospectus forms a part and as further described in the section titled “Corporate Conversion.” |

| ● | “DOE” means the U.S. Department of Energy. |

| ● | “Existing Owners” refers collectively to the owners of Fermi LLC Units prior to the consummation of the Transactions, who will be holders of our Common Stock immediately following consummation of the Transactions. |

| ● | “Fermi LLC” means Fermi LLC, a Texas limited liability company formed on January 10, 2025. |

| ● | “Fermi LLC Agreement” refers, as applicable, to Fermi LLC’s limited liability company agreement, as currently in effect, or to the limited liability company agreement effective immediately prior to the consummation of this offering, and as such agreement may thereafter be amended and/or restated. |

| ● | “Fermi LLC Units” means units representing limited liability company interests in Fermi LLC issued pursuant to the Fermi LLC Agreement. |

| ii |

| ● | “FERC” means the U.S. Federal Energy Regulatory Commission. |

| ● | “Firebird Acquisition” refers to the indirect acquisition of Firebird Equipment Holdco, LLC by Fermi LLC pursuant to that certain Membership Interest Purchase Agreement, dated July 29, 2025, by and among Fermi LLC, Fermi Equipment Holdco, LLC, Firebird and MAD Energy. We determined that the Firebird Acquisition did not constitute the acquisition of a “business” under Rule 11-01(d) of Regulation S-X. |

| ● | “Firebird” refers to Firebird LNG LLC, a Delaware limited liability company. |

| ● | “GPU” refers to a Graphics Processing Unit. |

| ● | “Groundwater Lease” refers to that certain Groundwater Lease, dated May 14, 2025 by and among The Texas Tech University System, Texas Tech University and Fermi LLC. |

| ● | “GW” means gigawatts, equating to one thousand megawatts. |

| ● | “Hyperscaler” refers to a cloud provider or technology company that is capable of delivering computing infrastructure and services at large scale, typically through large data centers and geographically distributed networks. |

| ● | “Inception” means January 10, 2025. |

| ● | “Lease” refers to that certain 99-year Ground Lease Agreement, dated May 14, 2025 by and among The Texas Tech University System, Texas Tech University and Fermi LLC. |

| ● | “MGD” means million gallons per day. |

| ● | “MW” means megawatts, equating to one thousand kilowatts, or one million watts. |

| ● | “Nasdaq” refers to the Nasdaq Stock Market, LLC. |

| ● | “NRC” means the U.S. Nuclear Regulatory Commission. |

| ● | “NERC” means The North American Electric Reliability Corporation. |

| ● | “Project Matador” means the Advanced Energy and Intelligence Campus at Texas Tech University. |

| ● | “Project Matador Site” means the approximately 5,769 acres of contiguous land held under the Lease in Carson County, Texas. |

| ● | “PUCT” means the Public Utility Commission of Texas. |

| ● | “REIT” means a real estate investment trust within the meaning of Sections 856 through 860 of the Code. |

| ● | “REIT Requirements” means the REIT qualification requirements set forth under Sections 856 through 860 of the Code and the applicable Treasury Regulations. |

| ● | “Restricted Equity Unit Grant” means those grants of restricted equity units to certain employees and consultants of the Company made prior to this offering. |

| ● | “Restricted Equity Unit Grant Net Settlement” means the net issuance of shares of Common Stock in connection with the Restricted Equity Unit Grants made prior to the consummation of this offering after giving effect to the withholding of shares of Common Stock to satisfy the estimated tax withholding and remittance obligations (as further described herein). |

| ● | “Seed Convertible Notes” refers to that certain series of convertible unsecured promissory notes of Fermi LLC issued in May 2025. |

| ● | “Series A Convertible Notes” refers to that certain series of convertible secured promissory notes of Fermi LLC issued in June and July 2025. |

| ● | “Series B Convertible Note” refers to that certain convertible secured promissory note of Fermi LLC issued July 29, 2025, in connection with the Firebird Acquisition. |

| ● | “SMR” means Small Modular Reactor. |

| ● | “SPS” means the Southwestern Public Service Company. |

| ● | “SPP” means the Southwest Power Pool. |

| ● | “TBOC” refers to the Texas Business Organizations Code, as amended. |

| ● | “Transactions” refers collectively to the organizational transactions described in the section titled “Corporate Conversion, ” the Firebird Acquisition, and the Convertible Notes Conversion. |

| ● | “Treasury Regulations” refers to the United States Treasury Regulations promulgated under the Code. |

| ● | “Unit Split” means the 150-for-1 forward unit split of the Company’s issued and outstanding Class A Units and Class B Units, effected pursuant to an amendment to the Fermi LLC Agreement on July 2, 2025. |

| ● | “Westinghouse” means Westinghouse Electric Company LLC. |

| ● | “Westinghouse Reactors” means AP1000 Pressurized Water Reactors developed by Westinghouse. |

| iii |

BASIS OF PRESENTATION

Fermi LLC, the registrant whose name appears on the cover of the registration statement of which this prospectus forms a part, is a Texas limited liability company. Prior to effectiveness of such registration statement, Fermi LLC intends to convert into a Texas corporation pursuant to a statutory conversion and change its name to Fermi Inc. as described in the section titled “Corporate Conversion.” As a result of the Corporate Conversion, the members of Fermi LLC will become holders of shares of Common Stock of Fermi Inc. shares of Common Stock of Fermi Inc. are being offered by this prospectus. Except as otherwise disclosed, the financial statements and other financial information included elsewhere in this prospectus do not give effect to the Corporate Conversion. We do not expect that the Corporate Conversion will have a material effect on the results of our operations.

Unless otherwise indicated, information presented in this prospectus assumes (i) that the underwriters’ option to purchase additional shares of Common Stock is not exercised, (ii) that the initial public offering price of the shares of our Common Stock will be $ per share (which is the midpoint of the price range set forth on the front cover page of this prospectus) and (iii) the filing and effectiveness of the Charter and the bylaws (our “Bylaws”), each of which will be adopted immediately prior to the consummation of this offering. See “Description of Capital Stock” for a description of our Charter and Bylaws. For additional information, please see “Corporate Conversion” and “Certain Relationships and Related Party Transactions.”

PRESENTATION OF FINANCIAL INFORMATION

The audited financial statements of Fermi LLC included in this prospectus (our “financial statements”) were prepared in accordance with U.S. Generally Accepted Accounting Principles (“GAAP”) and audited in accordance with the standards of the Public Company Accounting Oversight Board (“PCAOB”) and in accordance with auditing standards generally accepted in the United States of America.

Certain monetary amounts, percentages, and other figures included in this prospectus have been subject to rounding adjustments. Percentage amounts included in this prospectus have not in all cases been calculated on the basis of such rounded figures, but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this prospectus may vary from those obtained by performing the same calculations using the figures in our financial statements included elsewhere in this prospectus. Certain other amounts that appear in this prospectus may not sum due to rounding.

INDUSTRY AND MARKET DATA

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications or other published independent sources, and management estimates. Management estimates are derived from publicly available information released by independent industry analysts and other third-party sources, as well as data from our internal research, and are based on assumptions made by us upon reviewing such data, and our experience in, and knowledge of, such industry and markets, which we believe to be reasonable. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section titled “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these publications.

TRADEMARKS AND TRADE NAMES

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks, trade names or products in this prospectus is not intended to, and does not imply, a relationship with us or an endorsement or sponsorship by or of us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, service marks and trade names.

| iv |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements within the meaning of U.S. federal securities laws. In particular, statements pertaining to our business and growth strategies, investment and development activities and trends in our business, contain forward-looking statements. When used in this prospectus, the words “estimate,” “anticipate,” “expect,” “believe,” “intend,” “may,” “will,” “could,” “should,” “would,” “seek,” “position,” “support,” “drive,” “enable,” “optimistic,” “target,” “opportunity,” “approximately” or “plan,” or the negative of these words and phrases or similar words or phrases that are predictions of or indicate future events or trends and that do not relate solely to historical matters are intended to identify forward-looking statements. You can also identify forward-looking statements by discussions of strategy, plans or intentions of management.

Forward-looking statements involve numerous risks and uncertainties, and you should not rely on them as predictions of future events. Forward-looking statements depend on assumptions, data or methods that may be incorrect or imprecise and we may not be able to realize them. We do not guarantee that the transactions and events described will happen as described (or that they will happen at all), including with respect to historical environmental conditions at the Project Matador Site, which increases site preparation and timelines. The following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements:

| ● | our business model is highly dependent on the successful construction, development, leasing, and continued maintenance of Project Matador (as defined herein); |

| ● | our ability to access adequate project financing, commercial borrowings and debt and equity capital markets to fund our significant anticipated capital expenditures; |

| ● | our ability to construct, operate and maintain power generation facilities on schedule and at anticipated costs, either of which may be impacted by supply chain disruptions, including the impact on labor availability, raw materials and input commodity costs and availability, and manufacturing and transportation; |

| ● | the market for generating nuclear power is not yet established and may not achieve the growth potential we expect or may grow more slowly than expected; |

| ● | general business and economic conditions; |

| ● | environmental history, remediation, and associated risks; |

| ● | our ability to obtain and renew leases with our tenants on terms favorable to us, and manage our growth, business, financial results and results of operations; |

| ● | our ability to respond to price fluctuations and rapidly changing technology; |

| ● | the impact of tariffs and global trade disruptions on us and our tenants; |

| ● | changes in political conditions, geopolitical turmoil, political instability, civil disturbances, and restrictive governmental actions; |

| ● | we and our customers operate in a politically sensitive environment, and the public perception of nuclear energy can affect our customers and us; |

| ● | the degree and nature of our competition; |

| v |

| ● | our failure to generate sufficient cash flows to service indebtedness; |

| ● | material negative changes in the creditworthiness and the ability of our tenants to meet their contractual obligations; |

| ● | increases and volatility in interest rates; |

| ● | increased power, labor, equipment procurement, shipping, refurbishment or construction costs; |

| ● | labor shortages or our inability to attract and retain talent; |

| ● | changes in, or the failure or inability to comply with, government regulation, including regulation of our facilities’ environmental footprint and the project’s electric generation and storage assets; |

| ● | a failure of our information technology systems, systems conversions and integrations, cybersecurity attacks or a breach of our information security systems, networks or processes; |

| ● | our inability to obtain and/or maintain necessary government or other required consents or permits; |

| ● | our failure to qualify as a REIT and maintain our REIT qualification for U.S. federal income tax purposes; |

| ● | changes in, or the failure or inability to comply with, local, state, federal and applicable international laws and regulations, including related to taxation, real estate and zoning laws, and increases in real property tax rates; |

| ● | the impact of any financial, accounting, legal or regulatory issues or litigation that may affect us; and |

| ● | additional factors discussed in the sections entitled “Business and Properties,” “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus. |

You are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of this prospectus. While forward-looking statements reflect our good faith beliefs, they are not guarantees of future performance. We undertake no obligation to publicly release the results of any revisions to these forward-looking statements that may be made to reflect events or circumstances after the date of this prospectus or to reflect the occurrence of unanticipated events, except as required by law. In light of these risks and uncertainties, the forward-looking events discussed in this prospectus might not occur as described, or at all.

| vi |

This summary highlights selected information that is presented in greater detail elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our Common Stock. You should read this entire prospectus carefully, including the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our financial statements and the related notes included elsewhere in this prospectus before making an investment decision. Unless the context otherwise requires, the terms the “Company,” “Fermi,” “we,” “us” and “our,” prior to the Corporate Conversion (as defined herein), refer to Fermi LLC and its subsidiaries, and after the Corporate Conversion, refer to Fermi Inc., the issuer of the shares of Common Stock offered hereby, and its subsidiaries. For the definitions of certain terms used in this prospectus and not defined herein, see “Commonly Used Defined Terms.”

Overview

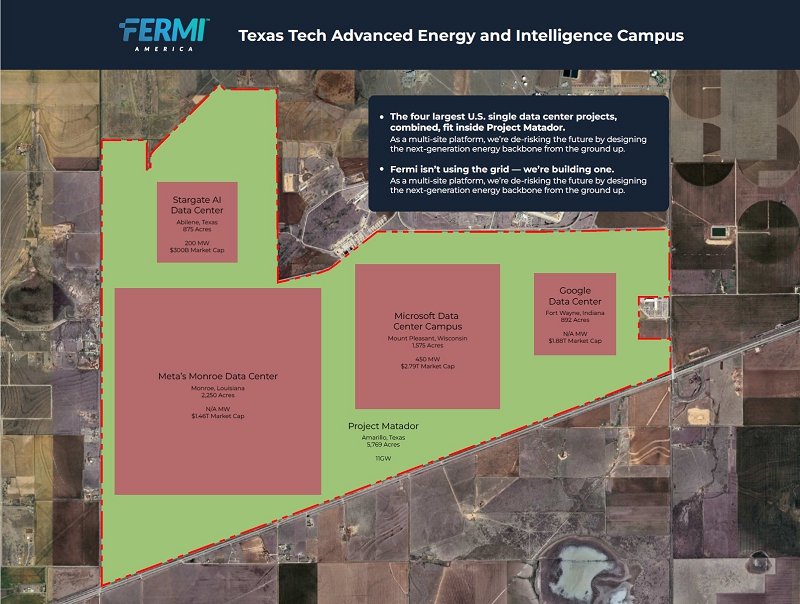

Fermi’s mission is to power the artificial intelligence (“AI”) needs of tomorrow. We are an advanced energy and hyperscaler development company purpose-built for the AI era. Our mission is to deliver up to 11 gigawatts (“GW”) of low-carbon, HyperRedundant™, and on-demand power directly to the world’s most compute-intensive businesses with 1 GW of power projected to be online by the end of 2026. We have entered into a long-term lease on a site large enough to simultaneously house the next four largest data center campuses by square footage currently in existence. In a world in which power is considered a key currency for AI innovation, we believe that Fermi has a unique combination of important advantages that will help propel America’s AI economy forward. Fermi will offer investors an opportunity to invest in AI growth and grid-independent energy infrastructure through a tax-efficient public REIT structure.

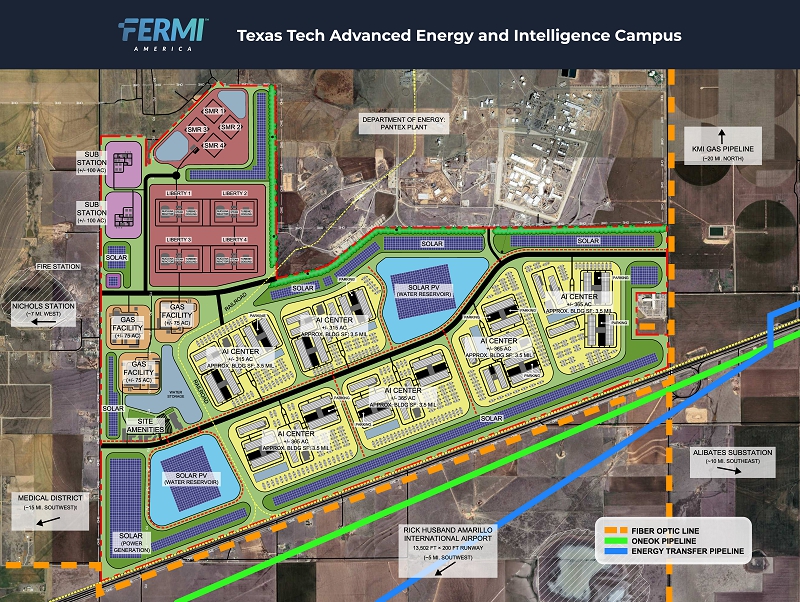

At the heart of our vision is the Advanced Energy and Intelligence Campus at Texas Tech University (“Project Matador”), which is a multi-gigawatt energy and data center development campus designed to support the accelerating needs of to-be-built AI infrastructure. Situated on a 5,769-acre site in Amarillo, Texas, Project Matador is secured by Fermi pursuant to a 99-year Ground Lease Agreement on land owned by Texas Tech University (the “Lease”), which we believe will provide long-term site control and potential efficiencies through a partnership with a public university. We believe our HyperRedundant™ site is strategically located adjacent to one of the largest known natural gas fields in the United States that is (i) within a high-radiance solar corridor, (ii) well-positioned for advanced nuclear development and (iii) supportive of multiple energy pathways including near-term natural gas power development. While Fermi’s mission is to expand beyond natural gas-fired generation, we believe our ready access to large volumes of natural gas from adjacent pipeline infrastructure could enable us to scale up to 11 GW of natural gas-fired base load power generation over time. Beyond natural gas-fired generation, our Combined License Application (“COL Application”) for 4 GW of nuclear power has undergone a preliminary review and has been accepted for processing by the U.S. Nuclear Regulatory Commission (the “NRC”), which reinforces Project Matador’s readiness for low-carbon baseload generation beyond natural gas-fired generation. With existing water, fiber, and natural gas infrastructure readily accessible, we believe Fermi is uniquely-positioned to deploy an integrated mix of natural gas, nuclear and solar energy power to enable grid-independent, high-density computing power on the Project Matador Site. Through a combination of natural gas turbine purchases, a focus on procuring other long lead-time equipment, and negotiations with Southwestern Public Service Company (“SPS”), the local utility, we expect to secure approximately 1 GW of power for our operations by the end of 2026 (including an expected 200 megawatts (“MW”) from our expected contractual arrangement with SPS). We believe this rapid power delivery timeline is a critical differentiator that will allow Fermi to attract tenants that require near-term access to large-scale, reliable energy to power their AI data center compute needs. Project Matador is in close proximity to the DOE’s Pantex Plant (the “Pantex Plant”), the nation’s primary nuclear weapons center, which employs approximately 4,600 skilled nuclear professionals. Our proximity to the Pantex Plant offers us the opportunity to access a highly experienced workforce steeped in nuclear safety culture and expertise. We believe this proximity to critical United States nuclear and security infrastructure will be highly attractive to our prospective tenants. With key regulatory approvals in progress, growing stakeholder relationships and energy infrastructure readiness, we believe that Project Matador represents unmatched, sector-defining potential to deliver up to 11 GW of power to on-site compute centers by 2035 through a redundant and flexible mix of natural gas, nuclear and solar energy power. Project Matador is expected to be anchored by what we believe would become the nation’s second-largest nuclear generation complex with capacity to house up to four AP1000 Pressurized Water Reactors developed by Westinghouse. Through our REIT structure, Fermi will offer investors exposure to AI infrastructure growth and long-term, large-scale and reliable energy development in a tax-efficient public vehicle.

| 1 |

Fermi is led by a seasoned management team with over a century of deep expertise across energy infrastructure, large-scale project development, and operational execution led by co-founders Rick Perry, Toby Neugebauer, Larry Kellerman, Mesut Uzman and Griffin Perry.

| ● | Governor Rick Perry, Co-Founder and Director, brings decades of executive-level leadership and energy policy experience to Fermi. As U.S. Secretary of Energy from 2017 to 2019, he oversaw the DOE’s $30 billion annual budget and led major policy initiatives to modernize the U.S. nuclear energy sector, including reviving efforts for advanced reactor licensing and securing international energy partnerships. During his tenure, he was instrumental in launching DOE programs that expanded support for nuclear innovation, LNG export infrastructure, and low-carbon baseload power, while reinforcing U.S. energy independence on the global stage. Prior to his federal role, Perry served as Governor of Texas for 15 years—the longest tenure in state history—where he was pivotal in transforming Texas into a global energy powerhouse through regulatory reform, private capital mobilization, and pro-growth policies. |

| ● | Toby Neugebauer, Co-Founder, President and Chief Executive Officer, is a seasoned investor and entrepreneur in energy infrastructure, with a career spanning private equity, investment banking, and strategic development. He co-founded and served as co-managing partner of Quantum Energy Partners, one of the largest dedicated energy private equity firms in the United States with approximately $28 billion of capital deployed (or to be deployed) in upstream, midstream, LNG, and energy services oil and gas investments and traditional and renewable power investments. At Quantum, Toby was involved in early investments in the Barnett Shale and the formation and development of Linn Energy and Meritage Energy Partners. Before Quantum, he founded Windrock Capital, which was later acquired by Macquarie, marking a successful exit in the financial services sector. He has served on numerous boards across the energy value chain and has led projects in private water infrastructure and fintech ventures. Toby holds a B.B.A. in Finance from NYU and is also a minority owner of Major League Soccer team Austin FC. |

| ● | Larry Kellerman, Chief Power Officer, boasts a nearly 40-year career in the power generation business, including the building of multi-billion-dollar energy asset portfolios as a Senior Management Partner at El Paso Corporation, Partner and Managing Director at Goldman Sachs and CEO of Quantum Utility Generation backed by Quantum Energy Partners. Larry has also advised private equity leaders, including I Squared Capital, on their power portfolios and currently serves as Managing Partner of Twenty First Century Utilities, where he focuses on the acquisition, operation and transformative improvement of assets and enterprises in the North American power generation sector. |

| ● | Mesut Uzman, Chief Nuclear Officer, is an international nuclear technology expert and has extensive experience leading high-profile nuclear projects and delivering complex reactor businesses in the UAE, China and Bulgaria. Mr. Uzman previously served as the Vice President of Engineering and Technical Services of Emirates Nuclear Energy Corporation, where he led the successful development of the 5.6 GW Barakah nuclear project, which comprises four APR-1400 nuclear reactors. Mr. Uzman has also served as a Senior Manager of Physical Protection System Engineering at Jacobs where he focused on solving physical and cybersecurity challenges for critical infrastructure projects, including nuclear power plants. In his early career, Mr. Uzman was the Director of Engineering at Westinghouse. |

| ● | Griffin Perry, Co-Founder and Director, is a veteran energy investor with deep expertise in capital formation and upstream oil & gas strategy. He is a Co-Founder and Managing Director at Grey Rock Energy Partners, where he has overseen the deployment of over $1 billion in investor capital across North American shale basins. Most notably, he led Grey Rock’s $1.3 billion merger forming Granite Ridge Resources (NYSE: GRNT), a publicly traded exploration and production (“E&P”) company where he serves as Co-Chairman. In addition to his leadership in capital markets transactions, Griffin has been central to raising multiple private funds focused on non-operated working interests and mineral rights strategies. Prior to Grey Rock, he worked at UBS and Deutsche Bank, advising high-net-worth energy clients and institutions. He also sits on the board of the Cotton Bowl Athletic Association. |

The Fermi team brings a proven track record of navigating complex regulatory environments, structuring and financing multi-billion-dollar energy assets, and delivering mission-critical infrastructure on time and on budget. Our collective expertise spans nuclear, natural gas, renewables, and digital infrastructure. We believe that our management team uniquely equips Fermi to deliver on time and at scale from early-stage development through online operations. Fermi’s management team is optimally positioned to create a unique platform to help power the AI era by helping advance the United States’ strategic priority to win the international AI development race. In addition, Fermi’s mission is consistent with recent U.S. initiatives prioritizing nuclear deployment. We believe our leadership team has key attributes that could materially assist the United States in achieving each of these strategic goals.

Project Matador

Project Matador is a first-of-its-kind energy campus to be built to power the AI revolution. Project Matador is a multi-phased project designed to deliver up to 11 GW of behind-the-meter energy and support up to 18 million square feet of AI-ready hyperscale compute infrastructure by 2035. Fully developed, Project Matador is expected to be one of the world’s largest integrated nuclear-, natural gas -, and solar-powered data center developments.

| 2 |

We believe Project Matador’s 5,769-acre site (the “Project Matador Site”) is ideal for pursuing our mission as it is unique in its combination of attributes critical to the success of this type of development. The Project Matador Site is secured under the Lease, which provides Fermi with exclusive long-term development rights and potential public-sector coordination, which we believe will accelerate entitlement and permitting processes. We are currently in the development and construction preparation stages with several foundational engineering, utility infrastructure, and interconnection assets under contract or in the final permitting or contracting stages. In addition, we are working diligently to satisfy all of the requisite conditions precedent contained in the Lease to enable Phase 1 development, as described in more detail below. See “Business and Properties—Facilities—TTU Lease Agreement.”

Fermi’s integrated energy platform is specifically designed to deliver compute-optimized power systems purpose-built for hyperscale AI. We believe our behind-the-meter energy model avoids significant impediments existing today for many other planned AI data center projects that largely rely on public grids for power. Project Matador’s key strengths consist of its HyperRedundant™ and high-availability factor generation ecosystems designed to operate adjacent to but semi-independent of traditional infrastructure. Our power systems will be purpose-built for hyperscale AI with high reliability and leading environmental performance consistent with our tenants’ objectives over the multi-decade lifecycle of Project Matador’s planned operations. Fermi’s integrated energy platform is not focused solely on speed-to-market at the expense of long-term environmental integrity as we believe our efficient, scaled and environmentally responsible behind-the-meter energy model that is supplemented by grid connections for additional redundancy avoids the most significant bottlenecks facing many other currently planned AI data center projects.

At Project Matador, our mission is to build HyperRedundant™, utility-scale operations at hyperscale speed. We strive to think nimbly, act decisively and operate purposefully with an integrated perspective of developing a high quality, long lifecycle, and reliable portfolio of diverse and integrated power generation assets. In building utility-scale integrated systems planning and operations, we are looking to develop a high reliability, low cost and option-rich asset and contract portfolio. We believe that we will be able to provide our data center and hyperscaler tenants the quality of power, agility of growth optionality and security of pricing that exceeds any other behind-the-meter powered land option nation-wide and equals the quality and reliability of any utility or grid offering. We intend to use our utility-scale thinking and planning to build and deploy multiple core layers of power generation supported by readily accessible critical infrastructure that will create a highly efficient, optimally reliable, and execution-ready platform that collectively includes:

| ● | Natural Gas: Project Matador’s HyperRedundant™ site is adjacent to the Panhandle-Hugoton Gas Field, which is one of the largest known natural gas fields in the United States at the crossroads of historically significant natural gas infrastructure that includes Energy Transfer LP’s (“Energy Transfer”) Panhandle Eastern Gas Pipeline and ONEOK, Inc.’s (“ONEOK”) WesTex Transmission Pipeline. These pipelines carry significant volumes of natural gas between the Waha Hub in the Permian Basin and the Amarillo-area Texas Panhandle. Our planned direct interconnection to these two major gas transmission networks is expected to provide long-term, firm commitment natural gas volumes to fuel our base load natural gas generation facilities with the uptime our tenants will expect. Fermi is in active, advanced discussion with ETC and ONEOK to finalize natural gas supply agreements. Project Matador is designed to include at least 4.5 GW of efficient natural gas-fired generation, with the first 580 MW of this power supply equipment secured through completed natural gas turbine purchases. Fermi, through a wholly-owned indirect subsidiary, is party to a turnkey equipment purchase contract (the “Siemens Contract”) to acquire in new and fully warranted condition, the equipment that we will need to develop and construct an efficient frame class combined cycle natural gas power generation project, including six Siemens Energy AG (“Siemens”) frame class SGT-800 natural gas turbines, six heat recovery steam generators (“HRSGs”) and one Siemens SST-600 steam turbine (collectively, the “Siemens System”), which provide best-in-class heat rate and low greenhouse gas emissions with strong reliability as each unit is fitted with exhaust stacks to allow for simple cycle operation in the event of outage conditions in the downstream steam cycle. The Siemens System is projected to supply base load power of approximately 400 MW at the Project Matador Site. Fermi has closed the acquisition of effectively all material equipment on the natural gas turbine and steam turbine cycles of a General Electric Company (“GE”) frame class 6B combined cycle configuration that include three used GE 6B gas turbines and one used GE steam turbine that came from a United States domiciled project that successfully operated these assets in combined cycle cogeneration mode. Fermi plans to overhaul and rejuvenate these assets by utilizing qualified GE maintenance and overhaul service providers. Fermi also plans to acquire a new set of HRSGs to complete the combined cycle configuration that are projected to provide roughly 180 MW of base load capacity at the Project Matador Site. |

| 3 |

We intend to supplement the initial 580 MW of our natural gas-fired generation with additional natural gas-fired, predominantly combined cycle assets phased into service to meet the needs of Project Matador’s hyperscaler and large-scale data center tenants as our plans include the eventual deployment of at least 4.5 GW of on-site natural gas-fired generation. This site will also host rapidly deployable, mid-scale (20 to 50 MW) aeroderivative and reciprocating engine natural gas generation for short-term reserve and back-up purposes to enable the high levels of reliability demanded by our tenants. While Fermi’s intention is to expand beyond natural gas-fired generation, we believe our unique access to large volumes of natural gas feedstock, ample space on the Project Matador Site to build additional natural gas power plants, and a continued advantaged pathway to secure critical path natural gas power generation assets may enable us to deliver up to 11 GW of purely natural gas-fired base load power.

| ● | Nuclear: Project Matador is designed to accommodate up to 6.4 GW of nuclear capacity via 4.0 GW of bifurcated Westinghouse Reactors and 2.4 GW of small modular nuclear reactors (“SMRs”) under planned development agreements with Westinghouse and other key nuclear industry vendors and intellectual property suppliers. Westinghouse is a leading player in the global nuclear industry, with a proven track record and technology that is already operational. There are six Westinghouse Reactors currently operational with twelve additional reactors under construction and five more under contract, and Fermi is in active discussions with Westinghouse regarding the procurement of the Westinghouse Reactors we intend to develop at the Project Matador Site. Our proposed, bifurcated system design segregates the nuclear reactor and other nuclear energy production and associated safety systems from the “non-nuclear” steam-driven power generation side of the nuclear island. In this manner, we are planning to achieve multiple interwoven objectives, including faster speed of execution, a simpler regulatory process, lower total system capital and operating costs, and more cost- and time-effective maintenance protocols. From a commercial and financial structuring perspective, the nuclear projects will utilize Special Purpose Entities (“SPEs”) with economic and risk ring-fencing to support project-level financings and available federal and state tax and funding incentives. Fermi filed a COL Application on June 18, 2025, which has been accepted for processing by the NRC as we begin our journey toward prospective approvals. As each new nuclear reactor is approved, Fermi expects to file additional COL Applications to create one of the world’s largest nuclear power campuses at Project Matador. Our approach to nuclear design, licensing, construction and operations aligns both with the (i) accelerating tenant demand for low-carbon, reliable baseload power and (ii) the objectives of federal and state leaders and policy makers focused on developing additional nuclear generation in the United States. |

| ● | Solar PV: Project Matador is designed to accommodate up to 500 MW of on-site utility-scale solar photovoltaic systems, which will operate in tandem with an on-site battery energy storage system (“BESS”). Initial designs are underway, and discussions with multiple prospective solar development partners are ongoing. In addition, up to 500 MW of additional solar generation may be sited on adjacent acreage, and the power from these off-site solar projects will be integrated into the Project Matador campus (if completed). Located in a nationally top-tier solar insolation region, the Project Matador Site enables significant renewable capacity that can be used to reduce a portion of our natural gas-fired generation during peak solar production hours whilst reducing our costs as well as our carbon emissions. |

| 4 |

| ● | Battery Storage: Project Matador’s design also includes a 1 MW x 4 hour array of integrated BESS designed to provide multiple value streams for Project Matador’s operations, including: (1) enhanced reliability of the overall power supply system by bridging periods of reduced generation capability, (2) voltage stability, (3) managing intra-second load variability resulting from data center IT processing volatility to prevent negative impacts on the generation or transmission assets servicing the data center loads and (4) enhancing overall power quality for the data center loads. |

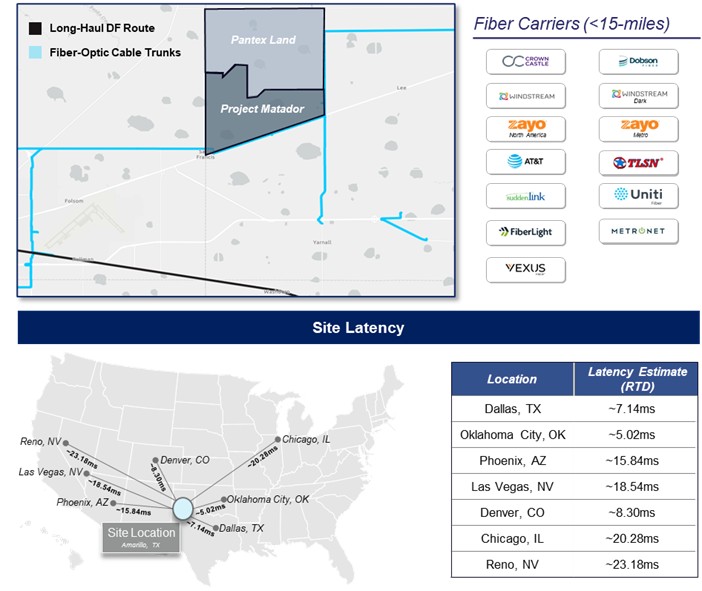

| ● | Fiber: Project Matador is strategically designed to transform the Amarillo area into a high-performance connectivity hub that will support the intensive demands of next-generation graphics processing unit (“GPU”) infrastructure and AI. Providers have scalable capacity up to 400 Gigabits per second (“Gbps”) that is enabled through provider-led amplification and dedicated dark fiber. |

Existing fiber infrastructure from FiberLight, LLC (“FiberLight”) has been identified on both the east and south boundaries of the Project Matador Site, with precise fiber access coordinates already in hand. Additionally, AT&T Inc. (“AT&T”) fiber is present on the south boundary of the Project Matador Site, and efforts are underway to acquire the geographic data to pinpoint the exact location of AT&T’s fiber access nodes. A third potential provider, Zayo Group, LLC (“Zayo”), maintains infrastructure approximately 12 miles southwest of Project Matador that could provide extended dark fiber connectivity to the Project Matador Site.

By integrating these fiber assets and working collaboratively with FiberLight, AT&T, and Zayo, Project Matador is poised to deliver low-latency, high-bandwidth connectivity across the Amarillo area.

| ● | Water: Our intent is to efficiently use water supplies for power generation and data center cooling applications by using advanced technologies and by utilizing available municipal water supplies (particularly municipal supplies that would otherwise be wasted or that represent a treatment and disposal problem for the municipal water authority). We have entered into a letter of intent with the Amarillo Utilities Department for up to 2 million gallons per day (“MGD”) initially that we expect to grow as high as 5.5 MGD of both potable and municipal graywater supplies to serve the Project Matador Site with additional supplies of graywater available in the near to medium term to the extent we build supply pipelines from Amarillo’s water treatment facilities to the Project Matador Site. Additionally, we plan on utilizing water conservation technologies on our power generation assets where viable, including air-cooled condensers in lieu of water cooling for many of our combined cycle plants. While we believe that municipal water supplies are sufficient for the Project Matador Site’s projected usage and the most cost-effective option, Project Matador’s groundwater lease with Texas Tech University (the “Groundwater Lease”) includes dual-aquifer fresh and salt water rights, which provides a resilient, scalable water supply for cooling and other operations. Project Matador is located directly above the Ogallala Aquifer, which had an available volume of 3.2 million acre-feet per year as of 2020 and is expected to have approximately 2 million acre-feet per year availability by 2080 according to the Texas Water Development Board Groundwater Division. Additionally, the Dockum Aquifer had an available volume of 288,000 acre-feet per year availability as of 2020 and is expected to decrease slightly to 241,000 acre-feet per year by 2080. |

| 5 |

Fermi’s energy strategy reflects an approach tailored to the needs of hyperscaler tenants and is positively differentiated from options being developed by many of our competitors. Our four-pronged strategy has the following, inter-operative and mutually supportive objectives:

| 1. | Long-term reliability equal to or greater than the conventional grid or non-diversified behind-the-meter options; |

| 2. | Cost structure lower than (and more predictable than) grid or non-diversified behind-the-meter options; |

| 3. | Emissions that are materially lower than the marginal emissions rate of the average US regional grid; and |

| 4. | Significant future-proofing through a high degree of future-build optionality to address data center and hyperscaler needs for adaptive and option-rich ability to secure additional, one-stop shopping for land, power, water and fiber. |

We are planning to deliver up to 1 GW of operational capacity by the end of 2026 using efficient Siemens and GE combined cycle natural gas power generation projects and grid and leased mobile natural gas-fired equipment to bridge our construction efforts. Phase 1 development of approximately one million square feet of AI compute capacity is currently expected to launch in April 2026.

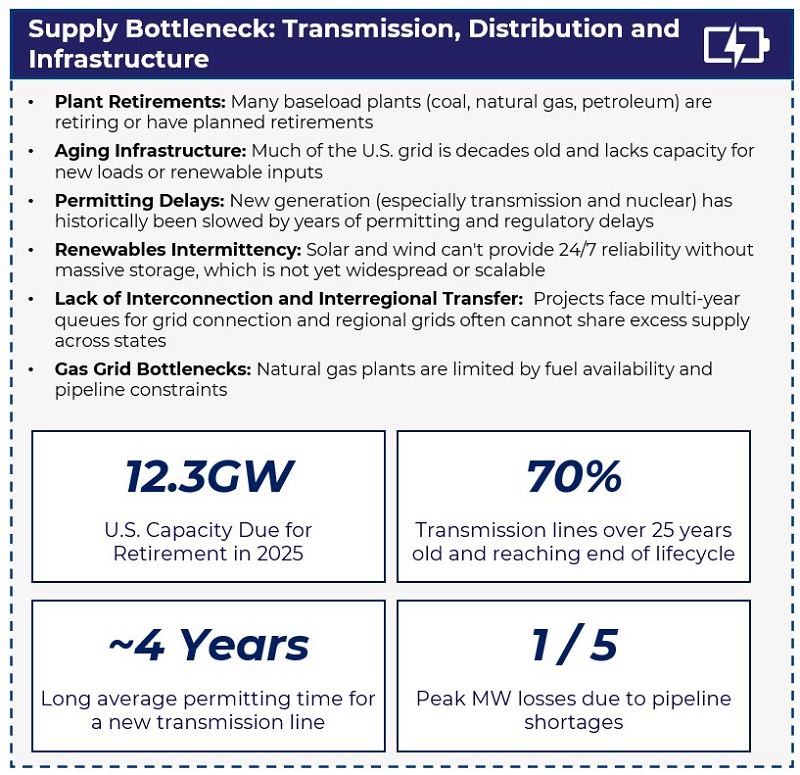

Industry and Market Opportunity: Shortage of Transmission and Electric Generation Constraining the AI Revolution

Fermi is positioned to address one of the most pressing constraints on the continued expansion of AI infrastructure: access to scalable, reliable, low-carbon and cost-effective power. As AI workloads and chip density grow exponentially across sectors, we believe the availability of high-capacity, low-latency, and low-carbon energy has become the most significant limiting factor to hyperscale data center deployment, surpassing land availability in many jurisdictions.

Power shortages are becoming increasingly common due to rapidly growing demand outpacing generation capacity expansion and grid modernization, which is creating an impending power shortfall and infrastructure bottleneck. Overall demand is expected to significantly outpace supply, with the United States expected to see data centers account for almost half of its electricity demand growth in the coming years. Rapid electrification coupled with a lack of interconnection and interregional transfers is creating multi-year queues, further constrained by the inability of many grids to adequately share power across state or regional lines.

| 6 |

Our vertically integrated model is designed to address growing power shortfalls head on by delivering a thoughtfully constructed, diversified mix of behind-the-meter and grid-supplemented power infrastructure leveraging a curated portfolio of efficient natural gas-fired, grid-supplied, nuclear and solar generation, with BESS robustly deployed to manage power quality and intra-day reliability. This approach enables the delivery of highly reliable base load, tenant-direct energy, largely independent of regional grid operators and utilities but while retaining interconnections to provide a modest ballast of low-cost grid power as well as system reliability and energy exchange potential to enable optimized operations. While we expect our owned assets will largely eliminate the timing, reliability, and cost challenges associated with traditional interconnection and power supply queue and regulatory processes, we also have built a strong relationship with the regional utility, SPS. We intend to build upon this relationship in a mutually beneficial manner through mutual resource development and sharing, a material strengthening of the interconnection between the Project Matador Site and the SPS system, and the exploration of mutually advantageous system energy exchange and reliability initiatives.

Adjacent infrastructure components—including fuel and water access, fiber, and cooling systems—are co-located to support seamless compute deployment at scale. Unlike traditional data center development, which frequently relies on phased grid upgrades or utility-scale renewable procurement without the security of a firm capacity resource backing or a robustly predictable pricing model, Fermi’s model is not contingent upon utility expansion or dynamically evolving grid, standardization and regulatory policies that increasingly position data center tenants at the lowest priority with respect to both pricing and to firm access to power during curtailment conditions. Numerous prior data center projects in the United States have either failed to achieve operational status or are at risk due to utility delays, changing regulatory policies or unmet interconnection commitments, resulting in undeveloped, underutilized or abandoned projects. We at Fermi have addressed this issue head-on in our engagement with SPS, providing transparent and timely information on our project, the capital spend we have deployed and committed to date and the general state of advanced dialogue with end-use data center and hyperscaler tenants, enabling Fermi to demonstrate, not simply through words but through confirmed actions, our strong credibility to utility, as well as other mission-critical stakeholders. Fermi’s control over energy sourcing and site development mitigates these risks and enables predictable, scalable infrastructure delivery.

| 7 |

Comparable business models are far more limited in scope than Project Matador. The closest analogues are powered land platforms, which typically utilize gas-fired generation with battery or renewable redundancy. These projects frequently maintain partial reliance on grid-based infrastructure. By contrast, Fermi is uniquely positioned to deliver up to 11 GW of low-carbon, dispatchable capacity over the coming years, supported by redundant natural gas supply infrastructure and a robust development roadmap. We anticipate that our short-term reliance on grid capacity will reduce dramatically as our behind-the-meter roll-out continues, with its long-term role being additional redundancy. This ambition is underpinned by a combination of advanced planning and permitting operations, strategic land positions, and nearby long-established grid interconnection pathways. Powered land platforms generally pursue one of two commercialization paths: (i) monetizing power in advance of tenant engagement; or (ii) entering partnerships with tenants or operators with a predefined development trajectory. Fermi intends to incorporate both strategies while maintaining end-to-end control of the underlying energy assets.

The markets in which Fermi operates represent a significant and rapidly expanding opportunity:

| ● | Global Generative AI Market: The global generative AI market is expected to grow from $64 billion in 2023 to $457 billion by 2027. This includes $287 billion allocated to generative AI hardware, $62 billion to generative AI software, and $108 billion to other generative AI-related spending, including gaming, ads, focused IT services and business services. |

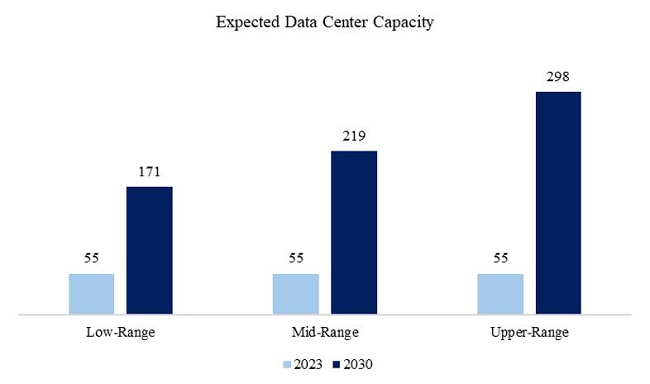

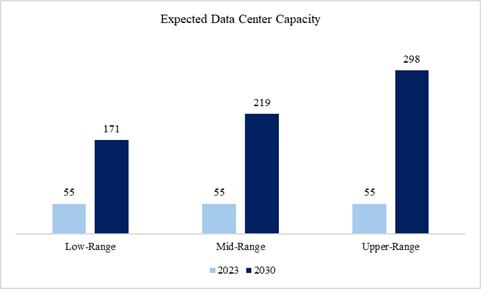

| ● | Global Data Center Power Demand: Total AI power demand is projected to grow from 55 GW in 2023 to up to 219 GW by 2030. AI workloads are forecasted to increase by a factor of 3.5 over the same period, necessitating an estimated $5.2 trillion in related infrastructure investment. |

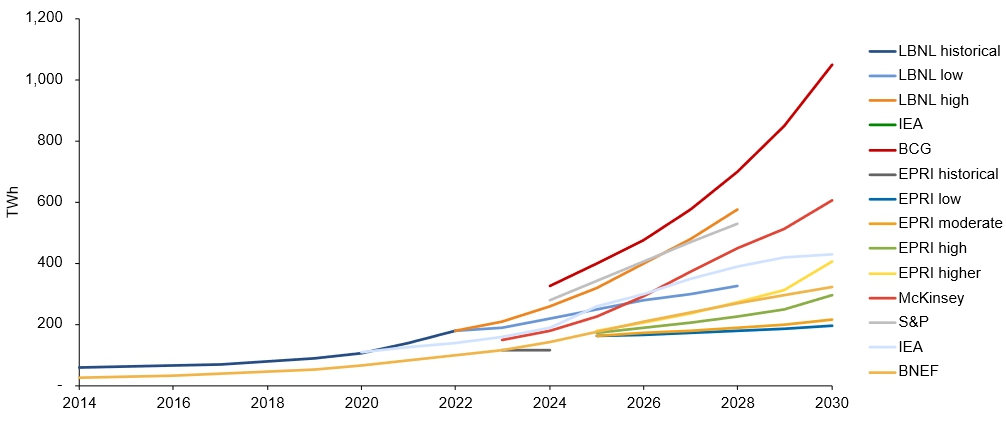

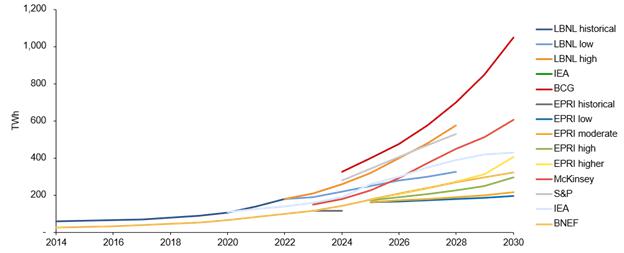

| ● | US Data Center Power Demand: U.S. Data Center Demand by 2030 is expected to land between 200 Terawatt-hour (“TWh”) and over 1,000 TWh per year across a range of sources. |

| 8 |

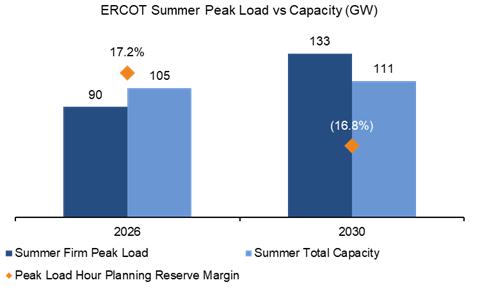

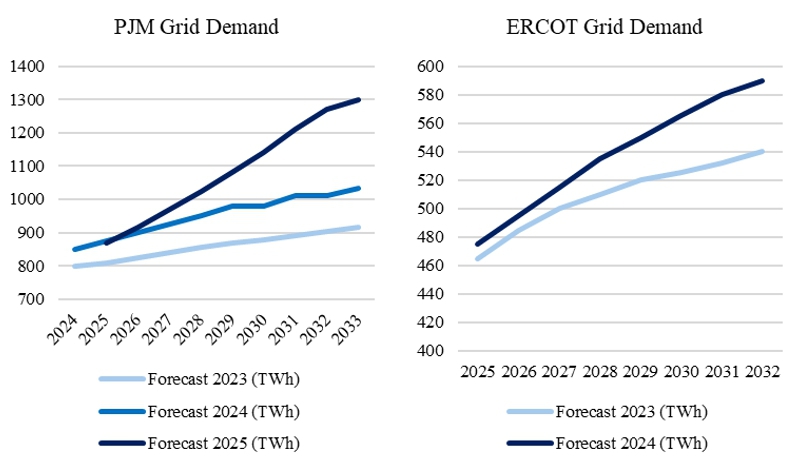

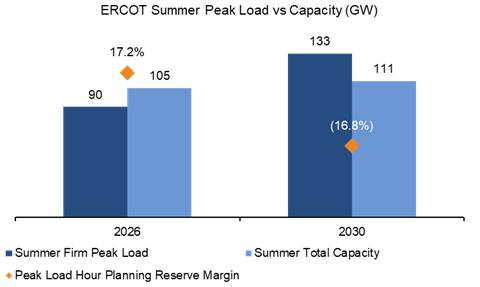

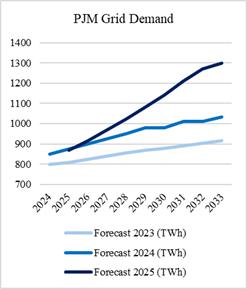

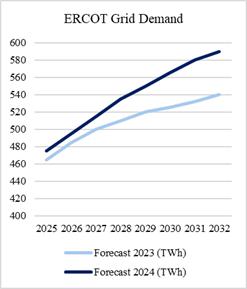

| ● | The key growth in data center capacity is driven by demand for AI, where over the same period, demand for AI capacity is expected to grow at a Compound Annual Growth Rate (“CAGR”) of 33%. This is especially true for data center dense markets, such as those serviced by PJM Interconnection LLC (“PJM”) and the Electric Reliability Council of Texas, Inc. (“ERCOT”). In PJM, grid demand forecasts have moved up materially over the last few years, putting pressure on reserve margins. In ERCOT, peak summer load is anticipated to exceed generation supply by approximately 17% by 2030. These dynamics are illustrated in the charts below. |

| 9 |

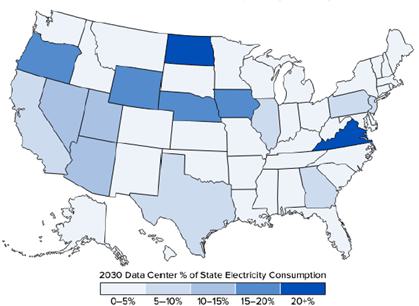

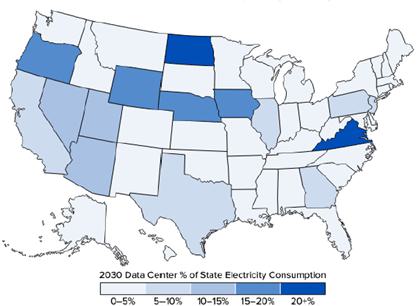

| ● | With data centers also growing in size, largely due to hyperscaler demand, new data centers are ranging from 100 MW to 1000 MW and require much more power. Aggregate data center consumption can potentially account for up to 20% of a state’s total consumption. The need for behind-the-meter solutions that are not reliant on grid expansion is clear. |

| ● | Capital Deployment Trends: In 2024, capital expenditure on AI-focused data center development reached $210 billion, with only $39 billion allocated to ongoing operating costs, indicating significant emphasis on upfront infrastructure buildout. |

| 10 |

| 2024 AI Data Center Spend | 2024 Data Center Operating Costs | |||||||||||||||||||||||

| (in billions) | GPUs and Other Chips | Other AI Spend | Total AI CapEx | Training and R&D | Inference | Total Op. Costs | ||||||||||||||||||

| Microsoft | $ | 20 | $ | 20 | $ | 40 | $ | 3 | $ | 3 | $ | 6 | ||||||||||||

| Meta | 11 | 12 | 23 | 2 | 2 | 4 | ||||||||||||||||||

| 14 | 15 | 29 | 3 | 1 | 4 | |||||||||||||||||||

| Amazon | 8 | 8 | 16 | 2 | 1 | 3 | ||||||||||||||||||

| Tier 2 Cloud | 26 | 26 | 52 | 8 | 3 | 11 | ||||||||||||||||||

| Enterprises & Government | 26 | 26 | 52 | 8 | 2 | 10 | ||||||||||||||||||

| Total | $ | 105 | $ | 107 | $ | 212 | $ | 26 | $ | 12 | $ | 38 | ||||||||||||

| ● | Powered Land and Data Center Real Estate: Between January 2023 and January 2025, data center development accounted for 24% of all U.S. industrial site acquisitions, up from 7% between 2017 and 2019. Hyperscaler-led transactions represented 12% of all development activity in 2024, compared to less than 2% in 2017. |

| ● | Low-Carbon Energy Supply: Meeting global net zero targets will require the addition of approximately 21,400 GW of wind, solar and battery storage capacity by 2040. Due to intermittency limitations, renewable sources alone are insufficient to meet continuous AI compute requirements, reinforcing the role of technologies that supply firm capacity, not simply as-available energy, such as natural gas fired combined cycle units and nuclear generation, along with BESS for intra-day shaping and reliability optimization. |

| ● | Power Density Increasing: The rise of generative AI (“GenAI”) is revolutionizing data center infrastructure requirements, particularly with respect to compute intensity and associated power demands. Traditional data centers (run on central processing units) were designed to support rack-level power densities of 3-10 kW per rack. Recent deployments are averaging 10-20 kW per rack, with certain next-generation AI deployments (run on GPUs) targeting 50-100 kW per rack and, in some cases, up to 240 kW per rack. This unprecedented rise in power density needs is a fundamental contributor to the acute constraints on available utility power across the United States, as existing transmission infrastructure and utility frameworks have not kept pace with the tremendous growth in power demand. As a result, hyperscale tenants are increasingly seeking programmatic infrastructure solutions that offer dedicated, reliable, redundant and scalable power delivery. We believe this market shift supports demand for an integrated energy and data infrastructure platform at scale, such as Project Matador, that is best-suited to meet the demands of the high-density AI workloads of the future. |

| ● | “Gravitational Pull”: Latency is not a primary constraint for many large-scale GenAI workloads, particularly AI model training. As a result, hyperscalers are prioritizing access to power and speed-to-market over proximity to traditional Tier 1 data center markets. This shift coincides with severe power constraints in legacy Tier 1 markets such as northern Virginia, where utility moratoriums and lack of available power and infrastructure have stymied new data center development. Accordingly, new data center builds are rapidly expanding into previously Tier 2 and Tier 3 markets which are rapidly emerging as new centers of compute infrastructure activity due to available grid capacity. This trend reflects a broader decentralization of compute infrastructure in the AI era, where access to grid-independent, scalable, massive amounts of power is driving hyperscalers’ decisions. We believe that Project Matador, with its plan to deliver energy at multi-GW scale, is uniquely positioned to capitalize on this opportunity. The Project Matador Site, due to its sheer scale and integrated energy strategy, has the potential to create its own gravitational pull in attracting hyperscale tenants and major AI operators, potentially establishing Project Matador as a hub for the future of AI and cloud computing. |

| 11 |

Fermi’s strategy addresses the convergence of these trends by enabling tenant-direct infrastructure delivery at the current scale and prospective scalability demanded by data center tenants. The Company believes its model offers significant differentiation relative to existing solutions in terms of speed-to-market, power supply reliability, absolute cost and forward pricing predictability and infrastructure control.

Project Matador Development Phases

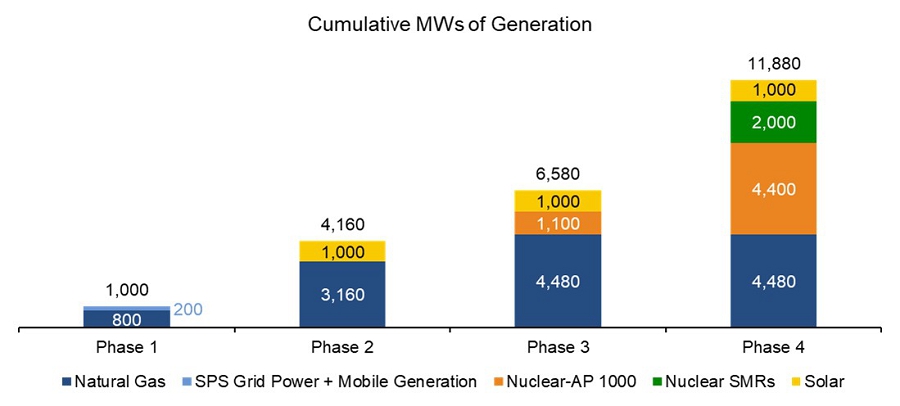

We have designed Project Matador with optimal scalability for data center tenants and hyperscalers who are the focus of our planning process. Over time, Project Matador is designed to deliver up to 11 GW of total generation capacity to serve tenants’ critical loads, with up to 18 million square feet of dedicated AI computing space. Development is organized into five main phases, some of which will occur concurrently:

| ● | Phase 0: We plan to establish critical external infrastructure to prepare the Project Matador Site for construction. During Phase 0, we plan to secure essential inputs, including an approximately 200 MW expected power supply from SPS, fiber connections, water services from the City of Amarillo, and large-scale natural gas delivery to support on-site energy needs as well as satisfaction of all conditions precedent under the Lease. See “Business and Properties—Facilities—TTU Lease Agreement.” Additionally, we intend to construct a pad for our Siemens turbine units, build a campus road for operational access, and establish a laydown yard for critical equipment and asset storage. Phase 0 plans also include foundational groundwork for the initial development of one million square feet of data center capacity as well as assuring the Project Matador Site is fully equipped to support subsequent construction phases and the operational demands of our tenants. |

| ● | Phase 1 (1 GW of Power by End of 2026): During Phase 1, we intend to develop one million square feet of data center capacity and deploy at least 1 GW of power by the end of 2026 from owned combined cycle gas projects, SPS grid-supplied power, temporary mobile generation sets and BESS systems, with solar photovoltaic generation for energy displacement. Fermi plans to complete site preparation, tenant acquisition, and early-stage interconnection and development work during this phase, with a target date to commence operations of April 2026 and a Phase 1 completion target date of December 2026. |

| ● | Phase 2: This phase contemplates development of a second one million square feet of data center space, served by 1 GW or greater of incremental firm power supplies, along with required reserve generation capability. This second phase is designed to be predominantly powered by a Fermi-owned, on-site natural gas fired combined cycle generation fleet in conjunction with additional solar for energy displacement purposes and incremental BESS assets, all operating on an integrated basis with the Phase 1 power supply portfolio. |

| ● | Phase 3: We plan to pursue dual track development of additional tenant-contracted data center capacity, served by a combination of new on-site, owned combined cycle natural gas fired generation and the development and construction of the initial 1.1 GW nuclear plant, utilizing a Westinghouse Reactor. We anticipate a construction period from the granting of the COL and any associated regulatory permits and approvals of 60 months per reactor from start of construction to project initial commercial operations. |

| ● | Phase 4: Fermi intends to complete expansion of tenant infrastructure, grid-scale interconnection, energy redundancy, and supplemental data center capacity, alongside the staged buildout of additional Westinghouse Reactors—totaling up to five additional reactors across two nuclear islands—and the full energy campus, including non-energy amenities. |

| 12 |

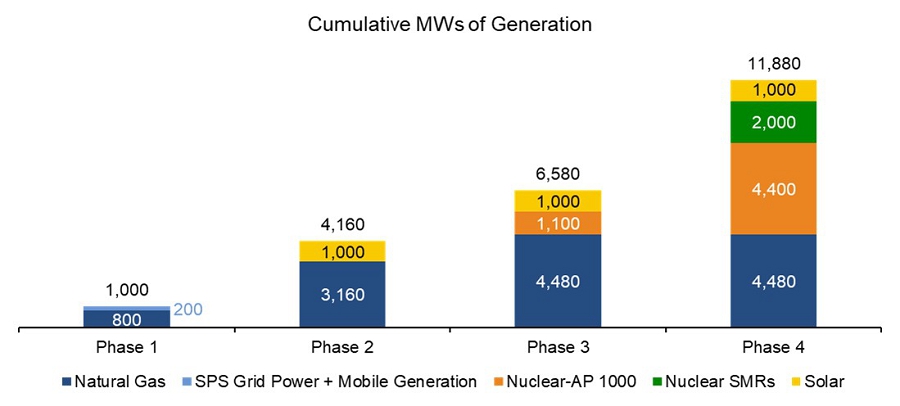

The below chart illustrates our plan to bring power online categorized by phase and energy mix.

Below is a chart detailing our planned square footage and power buildout, excluding grid power:

| Year | Incremental Shell Build (000’s sq. ft.) | Type of Incremental Generation Built | Incremental MW Built | |||||||

| 2025 | 120 | Natural Gas | 130 | |||||||

| 2026 | 880 | Natural Gas | 1,120 | |||||||

| 2027 | 1,545 | Natural Gas | 1,650 | |||||||

| 2028 | 1,545 | Natural Gas | 200 | |||||||

| 2029 | 1,545 | Natural Gas | 1,500 | |||||||

| 2030 | 1,545 | |||||||||

| 2031 | 1,545 | Nuclear-AP 1000 | 1,100 | |||||||

| 2032 | 1,545 | |||||||||

| 2033 | 1,545 | Nuclear-AP 1000 | 1,100 | |||||||

| 2034 | 1,545 | SMRs | 1,000 | |||||||

| 2035 | 1,545 | SMRs | 1,000 | |||||||

| 2036 | 1,545 | Nuclear-AP 1000 | 1,100 | |||||||

| 2037 | 1,545 | Nuclear-AP 1000 | 1,100 | |||||||

| Total | 17,995 | 11,000 | ||||||||

The following presents in-depth descriptions of current plans for each of the planned five main development phases, from site preparation and initial development through construction and expansion of our nuclear reactors. These phases run concurrently with each other, and site preparation and third-party coordination across all phases has already commenced.

Phase 0: Preparation of the Acquired Site ( Targeted Completion Date: YE 2025)

Phase 0 is dedicated to laying the groundwork for Project Matador by connecting critical external infrastructure to the project site, including 200 MW expected power supply from SPS, fiber optic connections, water services from the City of Amarillo, and large-scale natural gas delivery to meet on-site energy demands.

| 13 |

In addition to bringing off-site infrastructure on-site, we intend to construct a pad tailored for our Siemens turbine units, build a campus road to provide operational access, and establish a laydown yard for the storage of critical equipment and assets. Additionally, we plan to conduct preparatory groundwork for the initial development of one million square feet of data center capacity. Our site preparation project is designed to ensure the Project Matador Site is primed for subsequent construction phases. Commencement of Phase 1 construction additionally requires us to obtain a notice to proceed from Texas Tech University and the Texas Tech University System and the conditions to obtaining the notice include, among other things, to obtain an executed lease with a hyperscaler tenant, receipt of all permits and approvals for Phase 1 construction, and securing unconditional funding and financing for Phase 1 construction. See “Business and Properties—Facilities—TTU Lease Agreement.”

Phase 1: Initial Development & Construction of the First Gigawatt ( Targeted Completion Date: YE 2026)

Phase 1 is designed to deliver approximately 1 GW of operational power and approximately one million square feet of data center capacity by the end of 2026, serving up to two anchor tenants. Phase 1 is designed to include a mix of owned and operated, utility grid-supplied, and leased and interim generation sources. Phase 1 is expected to include the deployment of owned combined cycle natural gas generation, “bridge” operation of leased mobile equipment, grid-based utility supplied firm power and the development of solar photovoltaic (“PV”) systems and procurement and construction of supporting substation and transmission infrastructure.

To date, Fermi has contracted for approximately 800 MW of generating capacity, and has a letter of intent for an additional 200 MW of expected capacity, comprised of the following key assets:

| ● | 400 MW Siemens 6x1 SGT-800 Combined Cycle System Purchase: On May 9, 2025, Fermi entered into an Equipment Purchase Agreement (the “Firebird EPA”) with Firebird LNG, LLC (“Firebird”) to acquire the Siemens Contract. On July 29, 2025, Fermi, through its indirect wholly-owned subsidiary Fermi Equipment Holdco, LLC, consummated the Firebird Acquisition pursuant to a Membership Interest Purchase Agreement (“MIPA”) with MAD Energy Limited Partnership (“MAD”), thereby subsuming the Firebird EPA and acquiring all of the membership interests in Firebird Equipment Holdco, LLC (“Fermi Equipment Holdco”), a newly formed subsidiary of MAD, that, following a series of pre-closing restructuring steps involving Firebird and related entities, is a party to the Siemens Contract. While the Siemens System has been fully fabricated and is ready for shipment, it remains warehoused at Siemens staging facilities in Germany, Sweden, Vietnam and China pending final delivery and assembly. In connection with the closing under the MIPA, the parties negotiated an amendment to the Siemens Contract pursuant to which Siemens will deliver the Siemens System to Free Trade Zone 84 in Houston, Texas. Energization of the Siemens System is expected by April 2026. Under the MIPA, the aggregate consideration paid by Fermi for the Firebird Acquisition consisted of: |

| ● | A $145 million Series B Convertible Note issued to MAD by Fermi that is convertible, at the holder’s option or upon certain qualified events (including a qualified financing, including this offering, a change of control, or entry into certain definitive leases with a hyperscaler tenant), into Class A Units of Fermi at a price based on a $3 billion pre-money valuation or the price of securities issued in such qualified event. The Series B Convertible Note bears interest at a rate of 11% per annum, payable in kind quarterly in arrears, and matures on January 1, 2026. | |

| ● | A $20 million Secured Promissory Note issued to MAD by Fermi that provides for monthly installment payments by Fermi, which bears simple interest at a rate of 4.5% per annum and matures on December 1, 2025. As of the date of this prospectus, there is $ aggregate principal amount outstanding. | |

| ● | The grant of a net profits interest to MAD, entitling MAD to 2.5% of net operating income from the first 1,000 MW of dispatchable generation capacity at Project Matador, up to a net present value cap of $100 million. |

As a part of the Firebird Acquisition, the Company indirectly acquired all of the rights and obligations of Firebird Equipment Holdco under the Siemens Contract. Under the Siemens Contract, the Company owes approximately $134 million in remaining contractual payments plus shipping costs for the Siemens System which are currently estimated to be between approximately $10 million and $12 million. The Company will also owe additional amounts related to retrofitting expenses, which are not readily ascertainable as of the date of this prospectus. The payments due under the Siemens Contract are denominated in Swedish Kroner and are subject to exchange rate fluctuations.