As filed with the Securities and Exchange Commission on July 2, 2026.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| 7374 | ||||

| (State

or other Jurisdiction of Incorporation Or Organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S.

Employer Identification Number) |

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies of all communications, including communications sent to agent for service, should be sent to:

Michael Blankenship, Esq.

Beniamin Smolij, Esq.

Winston Taylor LLP

800 Capitol St Suite 2400

Houston, TX 77002

(713) 651-2600

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| ☒ | Smaller reporting company | |||||

| Emerging growth company | ||||||

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 2, 2026

PRELIMINARY PROSPECTUS

BOOST RUN INC.

58,738,753 Shares of Class A Common Stock

(Inclusive

of 29,533,018 shares of Class A Common Stock Issuable Upon Conversion of Class B Common Stock, 4,007,216 shares of Class A

Common Stock Underlying Private Warrants, 14,229,769 Shares of Class A Common Stock held by Certain

Selling Holders and

10,968,750 Earnout Shares)

4,007,216 Warrants to Purchase Shares of Class A Common Stock

This prospectus relates to the offer and sale, from time to time, by the selling holders identified in this prospectus (collectively, the “Selling Holders”), or their permitted transferees, of (i) up to 9,601,095 shares of our Class A common stock, par value $0.0001 (“Class A Common Stock”), held by certain Selling Holders who received such shares in connection with the Business Combination, (ii) up to 4,628,674 shares of Class A Common Stock issued to the Sponsor and its distributees in exchange for the Founder Shares purchased prior to the Willow Lane IPO, (iii) up to 4,007,216 shares of Class A Common Stock underlying warrants to purchase shares of Class A Common Stock held by certain Selling Holders (the “Private Warrants”), (iv) up to 29,533,018 shares of Class A Common Stock issuable upon the conversion of 29,533,018 shares of our Class B common stock, par value $0.0001 per share (“Class B Common Stock” and, together with the Class A Common Stock, the “Common Stock”), held by certain Selling Holders, (v) up to 10,968,750 shares of Class A Common Stock issued as earnout consideration (the “Earnout Shares”), consisting of up to 7,875,000 shares of Class A Common Stock issuable to Andrew Karos and up to 3,093,750 shares of Class A Common Stock issuable to the Sponsor and the SPV pursuant to the Earnout Agreement (as defined below), and (vi) 4,007,216 Private Warrants held by certain Selling Holders. The shares of Class A Common Stock and Private Warrants that may be sold by the Selling Holders are collectively referred to in this prospectus as the “Offered Securities.” We will not receive any of the proceeds from the sale by the Selling Holders of the Offered Securities.

We will receive all of the proceeds from the exercise of the Private Warrants for cash, if any, to the extent they are exercised for cash. We believe the likelihood that the Selling Holders will exercise their Private Warrants, and therefore the amount of cash proceeds that we would receive, is dependent upon the trading price of our Class A Common Stock. If the trading price for our Class A Common Stock is less than $11.50 per share, we believe holders of our Private Warrants are unlikely to exercise their Private Warrants. Conversely, these holders are more likely to exercise their Private Warrants the higher the price of our Class A Common Stock is above $11.50 per share. The Private Warrants are exercisable on a cashless basis under certain circumstances specified in the Warrant Agreement (as defined herein). To the extent that any Private Warrants are exercised on a cashless basis, the aggregate amount of cash we would receive from the exercise of the Private Warrants will decrease.

We will bear all costs, expenses and fees in connection with the registration of Offered Securities. The Selling Holders will bear all commissions and discounts, if any, attributable to their respective sales of Offered Securities. We are registering the Offered Securities for sale by certain of the Selling Holders pursuant to registration rights agreements with certain of the Selling Holders. See the section of this prospectus titled “Selling Holders” for more information.

The Selling Holders may offer and sell the Offered Securities owned by them covered by this prospectus from time to time. The Selling Holders may offer and sell the Offered Securities owned by them covered by this prospectus in a number of different ways and at varying prices. If any underwriters, dealers or agents are involved in the sale of any of the securities, their names and any applicable purchase price, fee, commission or discount arrangement between or among them will be set forth, or will be calculable from the information set forth, in any applicable prospectus supplement. See the sections of this prospectus titled “About this Prospectus” and “Plan of Distribution” for more information. No securities may be sold without delivery of this prospectus and any applicable prospectus supplement describing the method and terms of the offering of such securities. You should carefully read this prospectus and any applicable prospectus supplement before you invest in our securities.

The Offered Securities being offered by the Selling Holders were purchased by the Selling Holders at, or are exercisable at, various prices, certain of which are below the current trading price of our Class A Common Stock. The sale or the possibility of the sale of the Offered Securities being offered pursuant to this prospectus may negatively impact the market price of the Class A Common Stock.

The Class A Common Stock being offered for resale in this prospectus (including the shares of Class A Common Stock underlying the Class B Common Stock and the Private Warrants) represent approximately 77% of our total outstanding Common Stock on a fully diluted basis as of July 2, 2026. The sale of all the securities being offered in this prospectus could result in a significant decline in the public trading price of our Class A Common Stock. Despite such a decline in the public trading prices, the Selling Holders may still experience a positive rate of return on the securities they purchased due to the differences in the trading price and the purchase prices at which they purchased the securities as described herein. See “Risk Factors - Future sales, or the perception of future sales, of our Class A Common Stock by us or our stockholders in the public market could cause the market price for our Class A Common Stock to decline” and “Risk Factors - Certain existing securityholders acquired their securities in the Company at prices below the current trading price of such securities, and may experience a positive rate of return based on the current trading price. Future investors in our Company may not experience a similar rate of return.”

We are a “controlled company” within the meaning of the listing rules of The Nasdaq Stock Market, LLC (“Nasdaq”). As a controlled company, we are exempt from certain Nasdaq governance requirements that otherwise apply to the composition and function of our board of directors (the “Board”). As a result, (i) our Board does not have a majority of independent directors, (ii) the compensation of our executive officers is not determined by a majority of the independent directors or a committee of independent directors, and (iii) director nominees are not selected or recommended by a majority of the independent directors or a committee of independent directors. As of July 1, 2026, Andrew Karos beneficially owned approximately 90% of the voting power of our outstanding Common Stock. If at any time we cease to be a controlled company, we will take all action necessary to comply with the listing rules of Nasdaq, including appointing a majority of independent directors to our Board and ensuring our compensation committee and nominating and corporate governance committee are each composed entirely of independent directors, subject to any permitted “phase-in” periods.

Our Class A Common Stock is listed on Global Market tier of Nasdaq under the symbol “BRUN.” On June 30, 2026, the last reported sales price of the Class A Common Stock was $38.81 per share. We are an “emerging growth company” as defined under U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. The closing price of our warrants on the Capital Market tier of Nasdaq was $27.18 on June 30, 2026.

See “Risk Factors” beginning on page 13 to read about factors you should consider before investing in shares of our Class A Common Stock and Warrants.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2026

TABLE OF CONTENTS

| i |

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 (the “Registration Statement”) that we are hereby filing with the Securities and Exchange Commission (the “SEC”) using the “shelf” registration process. Under this shelf registration process, we and the Selling Holders may, from time to time, sell or otherwise distribute the Offered Securities as described in the section titled “Plan of Distribution” in this prospectus. We will not receive any proceeds from the sale by such Selling Holders of the Offered Securities offered by them described in this prospectus. We may receive proceeds from the exercise of Warrants registered hereunder by a person other than the original holder of the Warrants or its affiliates to the extent they are exercised for cash.

Neither we nor the Selling Holders have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the Selling Holders take responsibility for and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the Selling Holders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

We may also provide a prospectus supplement or post-effective amendment to the registration statement to add information to, or update or change information contained in, this prospectus. You should read both this prospectus and any applicable prospectus supplement or post-effective amendment to the registration statement together with the additional information to which we refer you in the sections of this prospectus titled “Where You Can Find Additional Information.”

On September 15, 2025, Willow Lane Acquisition Corp., a Cayman Islands exempted company (“SPAC” or “Willow Lane”), entered into a Business Combination Agreement (the “Business Combination Agreement,” as amended by Amendment No. 1 to the Business Combination Agreement, dated January 13, 2026 “Amendment No 1. To the Business Combination Agreement”), with Boost Run Inc., a Delaware corporation (“Boost Run”), Benchmark Merger Sub I Inc., a Delaware corporation and wholly-owned subsidiary of Boost Run (“SPAC Merger Sub”), Boost Run Holdings, LLC, a Delaware limited liability company (“Legacy Boost Run”), Benchmark Merger Sub II LLC, a Delaware limited liability company and wholly-owned subsidiary of Boost Run (“Company Merger Sub”), Andrew Karos, solely in his capacity as the representative of the holders of Legacy Boost Run’s issued and outstanding membership interests, and George Peng, solely in his capacity as the representative of Willow Lane shareholders.

On April 30, 2026, Willow Lane held an extraordinary general meeting of its shareholders (the “Meeting”), in connection with the Business Combination. At the Meeting, Willow Lane shareholders voted to approve the Business Combination and the other related proposals. In connection with the Meeting, no Willow Lane shareholders exercised their rights to redeem any ordinary shares for a pro rata portion of the approximately 134.5 million in the trust account of Willow Lane (the “Trust Account”).

On May 8, 2026 (the “Closing Date” and such consummation, the “Closing”), the parties consummated the transactions contemplated by the Business Combination Agreement (the “Business Combination”), as follows:

On the Closing Date, among other things, SPAC caused the continuation and the domestication of SPAC as a corporation incorporated under the laws of the State of Delaware (the “Conversion”), immediately followed by the deregistration of SPAC as an exempted company in the Cayman Islands. The Conversion occurred in accordance with the Delaware General Corporation Law (the “DGCL”) and Part XII of the Companies Act (As Revised) of the Cayman Islands (the “Companies Act”). Upon the Conversion, each issued and outstanding SPAC security remained outstanding and became a substantially identical security of SPAC as a Delaware corporation.

Following the Conversion, and on the Closing Date, SPAC Merger Sub merged with and into SPAC, with SPAC surviving as a wholly-owned subsidiary of Boost Run (the “SPAC Merger”). Simultaneously with the SPAC Merger, Company Merger Sub merged with and into Legacy Boost Run, with, pursuant to the Certificate of Merger, the surviving entity continuing as Boost Run Services, LLC and a wholly-owned subsidiary of Boost Run (the “Company Merger”, and together with the SPAC Merger, the “Mergers”). As a result of the Business Combination, SPAC and Legacy Boost Run became wholly-owned subsidiaries of Boost Run and Boost Run became a publicly traded company.

| 1 |

Pursuant to the terms of the Business Combination Agreement, at 5:00 p.m. New York City Time on the Closing Date (the “Effective Time”), by virtue of the Mergers, without any action on the part of any party or any other person:

● Each share of capital stock of SPAC Merger Sub issued and outstanding immediately prior to the completion of the SPAC Merger (the “SPAC Merger Effective Time”) was automatically cancelled and converted into one share of common stock of Willow Lane, with the same rights, powers and privileges as the shares so converted.

● Each Willow Lane Public Unit that was issued and outstanding immediately prior to the SPAC Merger Effective Time was automatically separated, and the holder was deemed to hold one Willow Lane Ordinary Share and one-half of one Willow Lane Public Warrant. Each Willow Lane Ordinary Share that was issued and outstanding immediately prior to the SPAC Merger Effective Time was automatically cancelled and converted into the right to receive one share of Boost Run Class A Common Stock, par value $0.0001 per share (“Boost Run Class A Common Stock”). Each Willow Lane Public Warrant was converted into one Boost Run Public Warrant and each Willow Lane Private Warrant was converted into one Boost Run Private Warrant.

● Each membership interest of Company Merger Sub outstanding immediately prior to the completion of the Company Merger (the “Company Merger Effective Time”) was converted into an equal number of membership interests of Legacy Boost Run.

● Each issued and outstanding membership interest of Legacy Boost Run (“Company Interest”) issued and outstanding immediately prior to the Company Merger Effective Time was automatically cancelled and ceased to exist in exchange for the right to receive (i) to the holder of the Class A Units, an installment note in the initial principal amount of $8,500,000 (the “Note”), and (ii) a number of newly issued shares of Boost Run Common Stock (defined below) equal to $441,500,000 divided by $10.00 per share (the “Merger Consideration”), consisting of 14,616,982 shares of Boost Run Class A Common Stock and 29,533,018 shares of Boost Run Class B Common Stock, par value $0.0001 per share (“Boost Run Class B Common Stock”, and together with the Boost Run Class A Common Stock, the “Boost Run Common Stock”), plus (iii) the contingent right to receive up to 7,875,000 Karos Earnout Shares (as defined below) as described below.

On the Closing Date, Boost Run issued an aggregate of 44,150,000 shares of Boost Run Common Stock to the former holders of Company Interests of Legacy Boost Run (collectively, the “Sellers”) in exchange for their equity interests in Legacy Boost Run, consisting of 14,616,982 shares of Boost Run Class A Common Stock and 29,533,018 shares of Boost Run Class B Common Stock, representing aggregate merger consideration with a value of $441,500,000 based on a per share value of $10.00. In addition, Boost Run issued the Note in the initial principal amount of $8,500,000 to Andrew Karos, Chief Executive Officer of Legacy Boost Run.

In connection with the Business Combination, the holder of Class A Units of Legacy Boost Run (“Andrew Karos”) has the contingent right to receive up to 7,875,000 newly issued shares of Boost Run Class A Common Stock (the “Karos Earnout Shares”), based on the performance of the Boost Run Class A Common Stock during the three-year period following the Closing (the “Earnout Period”), as follows: (i) if the VWAP of the Boost Run Class A Common Stock equals or exceeds $12.50 per share for any 20 trading days within any consecutive 30 trading days during the Earnout Period, 2,625,000 Karos Earnout Shares; (ii) if the VWAP equals or exceeds $15.00 per share under the same conditions, an additional 2,625,000 Karos Earnout Shares; and (iii) if the VWAP equals or exceeds $17.50 per share under the same conditions, an additional 2,625,000 Karos Earnout Shares.

In addition, pursuant to the Earnout Agreement (as defined below), Willow Lane Sponsor, LLC (the “Sponsor”) earned 1,125,000 newly issued shares of Boost Run Class A Common Stock (the “Sponsor Earnout Shares”) and Goodrich ILMJS LLC (the “SPV”) earned 1,968,750 newly issued shares of Boost Run Class A Common Stock (the “SPV Earnout Shares”), for a total of 3,093,750 shares, based on the performance of the Boost Run Class A Common Stock during the Earnout Period, with the same VWAP thresholds of $12.50, $15.00 and $17.50 per share described above.

In connection with the SPAC Merger, each outstanding Willow Lane Public Warrant was converted into one Boost Run Public Warrant and each outstanding Willow Lane Private Warrant was converted into one Boost Run Private Warrant. Each Boost Run Public Warrant entitles the holder thereof to purchase one share of Boost Run Class A Common Stock at an exercise price of $11.50 per share, subject to adjustment. The Boost Run Private Warrants have substantially the same terms as the Boost Run Public Warrants, subject to certain limited exceptions. As of the Closing Date, Boost Run had 6,325,000 Boost Run Public Warrants and 5,145,722 Boost Run Private Warrants issued and outstanding.

References to “Boost Run,” the “Company,” “we,” “us,” “our,” prior to the Business Combination refer to Legacy Boost Run, and such references following the Business Combination refer to Boost Run Inc. in its current corporate form as a Delaware corporation called “Boost Run Inc.” or “BRUN.”

| 2 |

MARKET AND INDUSTRY DATA

Certain industry data and market data included in this prospectus were obtained from independent third-party surveys, market research, publicly available information, reports of governmental agencies and industry publications and surveys. All of the estimates of the Company’s management presented herein are based upon review of independent third-party surveys and industry publications prepared by a number of sources and other publicly available information by the Company’s management. Third-party industry publications and forecasts state that the information contained therein has been obtained from sources generally believed to be reliable, yet not independently verified. The industry data, market data and estimates used in this prospectus involve assumptions and limitations, and you are cautioned not to give undue weight to such data and estimates. Although we have no reason to believe that the information from industry publications and surveys included in this prospectus is unreliable, we have not verified this information and cannot guarantee its accuracy or completeness. We believe that industry data, market data and related estimates provide general guidance, but are inherently imprecise. The industry in which the Company operates is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section titled “Risk Factors” and elsewhere in this prospectus.

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This document contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this registration statement may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

| 3 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Examples of forward-looking statements include, but are not limited to, statements with respect to the expectations, hopes, beliefs, intentions, plans, prospects, financial results or strategies regarding the Company, statements regarding the plans and use of proceeds, future financial condition of the Company and performance and expected financial impacts of the Business Combination on the Company’s business, and the Company’s expectations, intentions, strategies, assumptions or beliefs about future events, results of operations or performance that do not solely relate to historical or current facts.

These forward-looking statements generally are identified by the words “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “potential,” “should,” “will,” “would,” and similar expressions or the negative of such terms or other comparable terminology. Forward-looking statements are based on assumptions as of the time they are made and are subject to risks, uncertainties and other factors that are difficult to predict with regard to timing, extent, likelihood and degree of occurrence, which could cause actual results to differ materially from anticipated results expressed or implied by such forward-looking statements. Such risks, uncertainties and assumptions, include, but are not limited to:

| ● | the failure to realize the anticipated benefits of the Business Combination and any transactions contemplated thereby; |

| ● | the failure of the Company to maintain the listing of its securities on Nasdaq; |

| ● | costs related to the Business Combination and as a result of the Company becoming a public company; |

| ● | changes in business, market, financial, political and regulatory conditions; |

| ● | the ability of the Company to grow and manage growth profitably; |

| ● | risks relating to the Company’s anticipated operations and business, including the success of any future acquisitions; |

| ● | the Company’s ability to retain its management and key employees; |

| ● | the risk that issuances of equity or debt securities, including issuances of equity securities in connection with the Company’s acquisition strategy, may adversely affect the value of the Company’s common stock and dilute its stockholders; |

| ● | the risk that the Company experiences difficulties managing its growth and expanding operations following the consummation of the Business Combination; |

| ● | challenges in implementing the Company’s business plan, due to lack of an operating history, operational challenges, significant competition and regulation; and |

| ● | the other risks and uncertainties discussed in “Risk Factors” and elsewhere in this prospectus. |

In addition, there may be events that the Company’s management is not able to predict accurately or over which the Company has no control.

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this prospectus, which are incorporated by reference herein. If one or more events related to these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may differ materially from what we anticipate. Many of the important factors that will determine these results are beyond our ability to control or predict. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise. New factors emerge from time to time, and it is not possible for us to predict which will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

| 4 |

PROSPECTUS SUMMARY

Overview

Boost Run provides purpose-built infrastructure and cloud services for high-performance AI workloads by providing the latest NVIDIA graphics processing unit (“GPU”) servers within top-tier data centers allowing customers to run High-Performance Compute (“HPC”), inference and training jobs in certified, affordable and secure environments. Our company is designed to meet the operational, compliance, and performance needs of organizations deploying production AI systems, where infrastructure performance directly impacts business outcomes. As AI transforms enterprise operations, traditional cloud infrastructure often falls short for workloads requiring microsecond-level latency, continuous availability, and specialized hardware optimization.

We combine powerful GPU hardware with stringent security measures and compliance to deliver a platform for AI and HPC to maximize the value of data, models and intellectual property. We offer a diverse range of GPU servers hosted within top-tier datacenter facilities. These AI-compute solutions are designed to enable our users to maximize the value of their data, models, and intellectual property. By combining powerful GPU hardware with stringent security measures and compliance, we provide an ideal platform for running AI and other high-performance computing workloads.

We operate a distributed network of data centers through strategic partnerships with TierPoint and other parties, where Boost Run maintains four active facilities as of the third quarter of 2025; Lenovo as OEM partner; and Lumen for connectivity infrastructure. Our partnership with Carahsoft expands our reach into government contracts, enabling us to serve regulated public sector environments with stringent security and compliance requirements.

We have designed our platform from the ground up to anticipate and thrive in the regulated AI industry by being operator-certified, beyond just data center certification, enabling compliant AI solutions that our peers trust us to provide. In addition, we are audited to top standards, trusted to run sensitive AI workloads for the world’s largest companies, including governments, regulated industries and large corporations by focusing on enterprise grade compliance, security and owner-level certifications. We understand the critical importance of compliance and security when it comes to handling sensitive data and leveraging powerful AI technologies. Our unwavering commitment to industry-leading standards ensures that customers’ data, models, and intellectual property are safeguarded with the utmost care and diligence.

Our business model combines on-demand consumption with variable-term contracts, providing both revenue predictability and customer flexibility. We cater to organizations’ unique and specialized requirements through our Request for Build (“RFB”) program by enabling customers to work closely with our experts to design and deploy fully customized cluster solutions tailored to their specific needs. Customers are able to (i) choose from our extensive range of GPU options to ensure optimal performance for their AI applications; (ii) specify their storage requirements, whether they need high-performance NVMe SSDs, scalable object storage, or a combination of solutions to meet their data storage and access demands; and (iii) define their network requirements, including dedicated IP addresses, bandwidth allocation, and connectivity options, to ensure seamless data transfer and communication for their AI workloads.

Recent Developments

Business Combination with Willow Lane

On May 8, 2026, the SPAC, Boost Run and the additional parties thereto consummated the Business Combination, as follows:

| 5 |

On the Closing Date, among other things, SPAC caused the continuation and the domestication of SPAC as a corporation incorporated under the laws of the State of Delaware, immediately followed by the deregistration of SPAC as an exempted company in the Cayman Islands. The Conversion occurred in accordance with the DGCL and Part XII of the Companies Act. Upon the Conversion, each issued and outstanding SPAC security remained outstanding and became a substantially identical security of SPAC as a Delaware corporation.

Following the Conversion, and on the Closing Date, SPAC Merger Sub merged with and into SPAC, with SPAC surviving as a wholly-owned subsidiary of Boost Run (the “SPAC Merger”). Simultaneously with the SPAC Merger, Company Merger Sub merged with and into Legacy Boost Run, with, pursuant to the Certificate of Merger, the surviving entity continuing as Boost Run Services, LLC and a wholly-owned subsidiary of Boost Run (the “Company Merger”, and together with the SPAC Merger, the “Mergers”). As a result of the Business Combination, SPAC and Legacy Boost Run became wholly-owned subsidiaries of Boost Run and Boost Run became a publicly traded company.

Pursuant to the terms of the Business Combination Agreement, at 5:00 p.m. New York City Time on the Closing Date (the “Effective Time”), by virtue of the Mergers, without any action on the part of any party or any other person:

● Each share of capital stock of SPAC Merger Sub issued and outstanding immediately prior to the SPAC Merger Effective Time was automatically cancelled and converted into one share of common stock of Willow Lane, with the same rights, powers and privileges as the shares so converted.

● Each Willow Lane Public Unit that was issued and outstanding immediately prior to the SPAC Merger Effective Time was automatically separated, and the holder was deemed to hold one Willow Lane Ordinary Share and one-half of one Willow Lane Public Warrant. Each Willow Lane Ordinary Share that was issued and outstanding immediately prior to the SPAC Merger Effective Time was automatically cancelled and converted into the right to receive one share of Boost Run Class A Common Stock, par value $0.0001 per share (“Boost Run Class A Common Stock”). Each Willow Lane Public Warrant was converted into one Boost Run Public Warrant and each Willow Lane Private Warrant was converted into one Boost Run Private Warrant.

● Each membership interest of Company Merger Sub outstanding immediately prior to the Company Merger Effective Time was converted into an equal number of membership interests of Legacy Boost Run.

● Each issued and outstanding membership interest of Legacy Boost Run (“Company Interest”) issued and outstanding immediately prior to the Company Merger Effective Time was automatically cancelled and ceased to exist in exchange for the right to receive (i) to the holder of the Class A Units, an installment note in the initial principal amount of $8,500,000 (the “Note”), and (ii) a number of newly issued shares of Boost Run Common Stock (defined below) equal to $441,500,000 divided by $10.00 per share (the “Merger Consideration”), consisting of 14,616,982 shares of Boost Run Class A Common Stock and 29,533,018 shares of Boost Run Class B Common Stock, par value $0.0001 per share (“Boost Run Class B Common Stock”, and together with the Boost Run Class A Common Stock, the “Boost Run Common Stock”), plus (iii) the contingent right to receive up to 7,875,000 Karos Earnout Shares (as defined below) as described below.

On the Closing Date, Boost Run issued an aggregate of 44,150,000 shares of Boost Run Common Stock to the former holders of Company Interests of Legacy Boost Run (collectively, the “Sellers”) in exchange for their equity interests in Legacy Boost Run, consisting of 14,616,982 shares of Boost Run Class A Common Stock and 29,533,018 shares of Boost Run Class B Common Stock, representing aggregate merger consideration with a value of $441,500,000 based on a per share value of $10.00. In addition, Boost Run issued the Note in the initial principal amount of $8,500,000 to Andrew Karos, Chief Executive Officer of Legacy Boost Run.

In connection with the Business Combination, the holder of Class A Units of Legacy Boost Run (“Andrew Karos”) has the contingent right to receive up to 7,875,000 newly issued shares of Boost Run Class A Common Stock (the “Karos Earnout Shares”), based on the performance of the Boost Run Class A Common Stock during the three-year period following the Closing (the “Earnout Period”), as follows: (i) if the VWAP of the Boost Run Class A Common Stock equals or exceeds $12.50 per share for any 20 trading days within any consecutive 30 trading days during the Earnout Period, 2,625,000 Karos Earnout Shares; (ii) if the VWAP equals or exceeds $15.00 per share under the same conditions, an additional 2,625,000 Karos Earnout Shares; and (iii) if the VWAP equals or exceeds $17.50 per share under the same conditions, an additional 2,625,000 Karos Earnout Shares.

| 6 |

In addition, pursuant to the Earnout Agreement (as defined below), Willow Lane Sponsor, LLC (the “Sponsor”) may earn up to 1,125,000 newly issued shares of Boost Run Class A Common Stock (the “Sponsor Earnout Shares”) and Goodrich ILMJS LLC (the “SPV”) may earn up to 1,968,750 newly issued shares of Boost Run Class A Common Stock (the “SPV Earnout Shares”), for a total of 3,093,750 shares, based on the performance of the Boost Run Class A Common Stock during the Earnout Period, with the same VWAP thresholds of $12.50, $15.00 and $17.50 per share described above.

Assumption of Warrants

In connection with the SPAC Merger, each outstanding Willow Lane Public Warrant was converted into one Boost Run Public Warrant and each outstanding Willow Lane Private Warrant was converted into one Boost Run Private Warrant. Each Boost Run Public Warrant entitles the holder thereof to purchase one share of Boost Run Class A Common Stock at an exercise price of $11.50 per share, subject to adjustment. The Boost Run Private Warrants have substantially the same terms as the Boost Run Public Warrants, subject to certain limited exceptions. As of the Closing Date, Boost Run had 6,325,000 Boost Run Public Warrants and 5,145,722 Boost Run Private Warrants issued and outstanding.

Lock-up Agreement

In connection with the Business Combination, on the Closing Date, Boost Run entered into Lock-Up Agreements (the “Lock-Up Agreements”) with certain stockholders of Legacy Boost Run, pursuant to which each of the parties to the Lock-Up Agreements agreed not to effect any sale or distribution of any equity securities of Boost Run held by any of them during the lock-up period set forth therein, which ends on the earlier of (i) six months after the Closing or (ii) the date on which the closing price of Boost Run Class A Common Stock equals or exceeds $12.00 per share for any 20 trading days within any 30-trading day period, subject to certain permitted transfers and other exceptions.

Registration Rights Agreement

In connection with the Business Combination, on the Closing Date, Boost Run, Willow Lane and the Sponsor entered into an Amended and Restated Registration Rights Agreement (the “Registration Rights Agreement”) with BTIG, LLC, Craig-Hallum Capital Group, LLC and certain members of Legacy Boost Run (collectively with the Sponsor, BTIG, LLC and Craig-Hallum Capital Group, LLC, the “Holders”), pursuant to which Boost Run agreed to register for resale shares of Boost Run Common Stock and other securities held by the Holders, subject to the terms and conditions described therein.

Indemnification Agreements

In connection with the Business Combination, on the Closing Date, Boost Run entered into indemnification agreements (the “Indemnification Agreements”) with each of its directors and executive officers. Subject to certain exceptions, the Indemnification Agreements provide that Boost Run will indemnify each of its directors and executive officers for certain expenses, which may include attorneys’ fees, judgments, fines and settlement amounts, incurred by a director or officer in any action or proceeding arising out of their services as one of Boost Run’s directors or officers or any other company or enterprise to which the person provides services at Boost Run’s request.

The foregoing description of the Indemnification Agreements is qualified in its entirety by reference to the form of Indemnification Agreement, a copy of which is attached as Exhibit 10.3 to this Current Report on Form 8-K and is incorporated herein by reference.

Earnout Agreement

In connection with the Business Combination, on September 15, 2025, Boost Run, the Sponsor and the SPV entered into an Earnout Agreement (the “Earnout Agreement” as amended on January 13, 2026, “Amendment to the Earnout Agreement”), providing that the Sponsor may earn up to 1,125,000 Sponsor Earnout Shares and the SPV may earn up to 1,968,750 SPV Earnout Shares based on the performance of the Boost Run Class A Common Stock during the Earnout Period.

| 7 |

Employment Agreements

In connection with the Business Combination, on the Closing Date, Boost Run entered into an employment agreement with Andrew Karos (the “Karos Employment Agreement”), pursuant to which Mr. Karos serves as Chief Executive Officer of Boost Run. Under the Karos Employment Agreement, Mr. Karos receives a base salary of $1.00 per year, subject to annual review by the Boost Run board of directors (the “Boost Run Board” or the “Board”) (or a duly authorized committee thereof). Mr. Karos’s employment may be terminated by either party at any time and for any reason in accordance with applicable law. The Karos Employment Agreement contains customary confidentiality, intellectual property assignment and non-disparagement covenants. The Karos Employment Agreement is governed by the laws of the State of Illinois.

In connection with the Business Combination, on the Closing Date, Boost Run entered into an employment agreement with Erik Guckel (the “Guckel Employment Agreement”), pursuant to which Mr. Guckel serves as Chief Financial Officer of Boost Run. Under the Guckel Employment Agreement, Mr. Guckel receives an annual base salary of $400,000, subject to annual review by the Boost Run Board or its compensation committee. Mr. Guckel is eligible to earn an annual cash bonus with a target of 75% of his base salary, with the ability to earn between 0% and 150% of such target based on Company and individual performance metrics determined by the Boost Run Board or the compensation committee.

In addition, Mr. Guckel is eligible to receive a one-time long-term incentive award under the Boost Run Inc. 2026 Omnibus Incentive Plan (the “Incentive Plan”) consisting of 1,156,304 time-based restricted stock units, 722,691 performance-based restricted stock units and a nonqualified stock option to purchase 1,011,766 shares of Boost Run Class A Common Stock, subject to the terms and conditions of the Incentive Plan and applicable award agreements.

If Mr. Guckel’s employment is terminated by Boost Run without cause or by Mr. Guckel for good reason (other than in connection with a change in control), Mr. Guckel is entitled to, among other things, receive (i) 12 months of base salary continuation, (ii) any earned but unpaid annual bonus for the prior fiscal year, (iii) a pro-rata annual bonus for the year of termination based on actual performance and (iv) treatment of outstanding equity in accordance with the Incentive Plan and applicable award agreements, in each case subject to his execution and non-revocation of a release of claims. If such termination occurs within 12 months following a change in control, Mr. Guckel is entitled to enhanced severance consisting of, among other things, (i) 18 months of base salary payable in a lump sum, (ii) any earned but unpaid annual bonus for the prior fiscal year, (iii) 100% of the higher of his target bonus or the prior year’s actual bonus and (iv) 100% acceleration of outstanding unvested equity awards, in each case subject to his execution and non-revocation of a release of claims.

The Guckel Employment Agreement also contains customary confidentiality, intellectual property assignment, non-competition, non-solicitation and non-disparagement covenants. The non-competition and non-solicitation covenants apply during employment and for 12 months following termination of employment. The Guckel Employment Agreement is governed by the laws of the State of Illinois.

Corporate Information

Boost Run’s principal executive offices are located at 5 Revere Drive, Suite 200 Northbrook, IL 60062 and its telephone number is (847) 489-3367. Boost Run’s website is www.boostrun.com. Information found on or accessible through our website is not incorporated by reference into this prospectus and should not be considered part of this prospectus.

| 8 |

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). For so long as we remain an emerging growth company, we are permitted, and currently intend, to rely on the following provisions of the JOBS Act that contain exceptions from disclosure and other requirements that otherwise are applicable to public companies and file periodic reports with the SEC. These provisions include, but are not limited to:

| ● | being permitted to present only two years of audited financial statements and selected financial data and only two years of related “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our periodic reports and registration statements, including this prospectus, subject to certain exceptions; |

| ● | not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley”), as amended; |

| ● | reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements, and registration statements, including in this prospectus; |

| ● | not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements; and |

| ● | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

We will remain an emerging growth company until the earliest to occur of:

| ● | the fifth anniversary of the date of our first sale of common equity securities pursuant to an effective registration statement; |

| ● | the last day of the fiscal year, in which we have total annual gross revenue of at least $1.235 billion, adjusted yearly for inflation; |

| ● | the date on which we are deemed to be a “large accelerated filer,” as defined in the Exchange Act; and |

| ● | the date on which we have issued more than $1 billion in non-convertible debt over a three-year period. |

We have elected to take advantage of certain of the reduced disclosure obligations in this prospectus and may elect to take advantage of other reduced reporting requirements in our future filings with the SEC. As a result, the information that we provide to holders of our stockholders may be different than what you might receive from other public reporting companies in which you hold equity interests.

We have elected to avail ourselves of the provision of the JOBS Act that permits emerging growth companies to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. As a result, we will not be subject to new or revised accounting standards at the same time as other public companies that are not emerging growth companies.

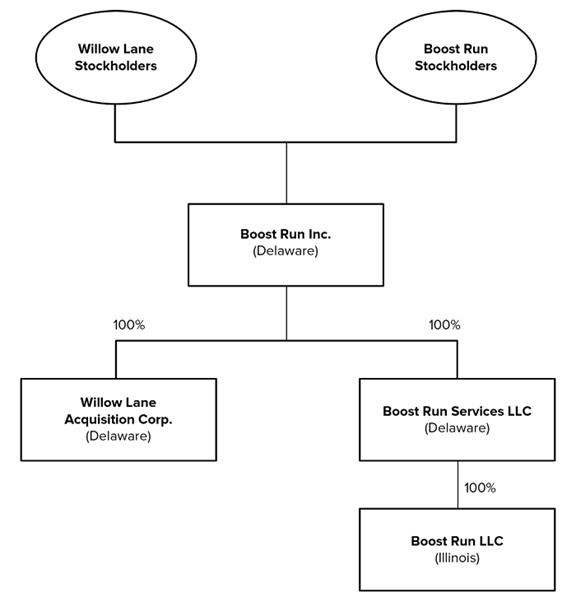

Organizational Structure

Current Structure

The following simplified diagram illustrates the ownership structure of the Company. The percentage ownerships of shares of our common stock are presented assuming, among other things, that no shares of our common stock are issued pursuant to the Incentive Plan.

| 9 |

| 10 |

Summary of Risk Factors

The risk factors summarized below could materially harm our business, operating results and/or financial condition, impair our future prospects and/or cause the price of our ordinary shares to decline. These risks are discussed more fully following this summary. Material risks that may affect our business, operating results and financial condition include, but are not necessarily limited to, the following:

| ● | Boost Run’s recent growth may not be indicative of its future growth, and if it does not effectively manage its future growth, its business, operating results, financial condition, and prospects may be adversely affected. | |

| ● | Boost Run has a limited number of suppliers for significant components of the equipment it uses to build and operate its platform and provide its solutions and services. Any disruption in the availability of these components could delay Boost Run’s ability to expand or increase the capacity of its infrastructure or replace defective equipment. | |

| ● | Boost Run’s business would be harmed if it were not able to access sufficient power or by increased costs to procure power, prolonged power outages, shortages, or capacity constraints. | |

| ● | Boost Run depends entirely on third-party partners, including data center operators, to host Boost Run’s GPU infrastructure and provide various services in support of its business, and any disruption to these relationships or the performance of these partners could materially harm Boost Run’s business, financial condition, and results of operations. | |

| ● | If Boost Run’s data center providers fail to meet the requirements of its business, or if the data center facilities experience damage, interruption, or a security breach, its ability to provide access to its infrastructure and maintain the performance of its network could be negatively impacted. | |

| ● | Boost Run’s ability to grow its business and serve customer demand is dependent on the availability of suitable colocation capacity from third-party partners, and constraints on partner capacity or partners’ willingness to expand could significantly limit Boost Run’s growth prospects. | |

| ● | Boost Run’s platform may become less competitive if it fails (i) to efficiently enhance its platform, (ii) develop and sell new solutions and services and (iii) respond effectively to rapidly changing technology, evolving industry standards, changing regulations, and changing customer needs, requirements, or preferences. | |

| ● | The broader adoption, use, and commercialization of AI technology, and the continued rapid pace of developments in the AI field, are inherently uncertain. Failure by Boost Run’s customers to continue to use its Boost Run Cloud Platform to support AI use cases in their systems, or Boost Run’s ability to keep up with evolving AI technology requirements and regulatory frameworks, could have a material adverse effect on its business, operating results, financial condition, and prospects. | |

| ● | Boost Run’s operations require substantial capital expenditures, and it will require additional capital to fund its business and support its growth, and any inability to generate or obtain such capital on acceptable terms, if at all, or to lower its total cost of capital, may adversely affect its business, operating results, financial condition, and prospects. | |

| ● | The unaudited pro forma financial information included elsewhere in this prospectus may not be indicative of our future operating results or financial performance. | |

| ● | If the Business Combination’s benefits do not meet the expectations of investors or securities analysts, the market price of Boost Run’s securities may decline. | |

| ● | We are a “controlled company” under Nasdaq listing rules. As a result, our stockholders do not have, and may never have, certain corporate governance protections that are available to stockholders of companies that are not controlled companies. | |

| ● | Our management team has limited experience managing a public company. |

| 11 |

THE OFFERING

| Issuer | Boost Run Inc. | |

| Resale of Class A Common Stock | ||

| Shares of Class A Common Stock offered by the Selling Holders | We are registering the resale by the Selling Holders, or their permitted transferees, of up to 58,738,753 shares of Class A Common Stock, consisting of (i) up to 9,601,095 shares held by certain Selling Holders who received such shares in connection with the Business Combination, (ii) up to 4,628,674 shares issued to the Sponsor and its distributees in exchange for the Founder Shares purchased prior to the Willow Lane IPO, (iii) up to 4,007,216 shares underlying the Private Warrants, (iv) up to 29,533,018 shares issuable upon the conversion of Class B Common Stock held by certain Selling Holders, and (v) up to 10,968,750 shares issued as earnout consideration pursuant to the Earnout Agreement. | |

| Warrants offered by the Selling Holders | We are registering the resale by the Selling Holders, or their permitted transferees, of up to 4,007,216 Private Warrants. | |

| Use of proceeds | We will not receive any proceeds from the sale of the shares of Class A Common Stock by the Selling Holders. We will receive proceeds from the exercise of the Private Warrants to the extent they are exercised for cash. We intend to use any such proceeds for general corporate purposes. See “Use of Proceeds.” | |

| Nasdaq listing | Our Class A Common Stock is listed on the Global Market tier of Nasdaq under the symbol “BRUN.” Our Warrants are listed on Capital Market tier of Nasdaq under the symbol “BRUNW.” | |

| Risk factors | Investing in our Class A Common Stock involves risks. See “Risk Factors” beginning on page 13 of this prospectus for a discussion of certain factors you should carefully consider before deciding to invest in our Class A Common Stock. |

For additional information concerning the offering, see “Plan of Distribution” beginning on page 135.

| 12 |

RISK FACTORS

Any investment in our securities involves a high degree of risk. You should carefully consider all of the information contained in this prospectus and any subsequent prospectus supplement, including our financial statements and related notes thereto, before investing in our securities. However, such risks and those discussed elsewhere in any subsequent prospectus supplement are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect us. If any of the risks described in any subsequent prospectus supplement or others not specified therein materialize, our business, financial condition and results of operations could be materially and adversely affected. In that case, you may lose all or part of your investment.

Unless the context otherwise requires, all references in this subsection to the “Company,” “Boost Run,” “we,” “us,” or “our” refer to the business of Boost Run and its consolidated subsidiaries.

General Risks Related to Boost Run’s Business and Industry

Boost Run’s recent growth may not be indicative of its future growth, and if it does not effectively manage its future growth, its business, operating results, financial condition, and prospects may be adversely affected.

Boost Run was founded in 2023 and launched its Cloud Services Platform at the end of 2024 and has experienced significant growth in a short period of time. Investors should not rely on the revenue growth of any prior quarterly or annual period as an indication of Boost Run’s future performance. Even if Boost Run’s revenue continues to increase, its revenue growth rate is expected to decline in the future as a result of a variety of factors, including the maturation of its business. Overall growth of Boost Run’s revenue will depend on a number of factors, including but not limited to its ability to:

| ● | operate its cloud infrastructure, including due to supply chain limitations and data center or power availability; | |

| ● | compete with other companies in its industry, including those with greater financial, technical, marketing, sales, and other resources; | |

| ● | continue to develop new solutions and services and new functionality for its platform and successfully further optimize its existing infrastructure, solutions, and services; | |

| ● | retain existing customers and increase sales to existing customers, as well as attract new customers and grow its customer base; | |

| ● | successfully expand its business domestically and internationally; | |

| ● | generate sufficient cash flow from operations and raise additional capital, including through indebtedness, to support continued investments in its platform to maintain its technological leadership and the security of its platform; | |

| ● | strategically expand its direct sales force and leverage its existing sales capacity; | |

| ● | introduce and sell its solutions and services to new markets and verticals; | |

| ● | recruit, hire, train, and manage additional qualified personnel for its research and development activities; | |

| ● | maintain its existing, and enter into new, more cost-efficient, financing structures; and | |

| ● | successfully identify and acquire or invest in businesses, products, or technologies that it believes could complement or expand its platform. |

| 13 |

In addition to the factors discussed above, Boost Run’s revenue growth may also be impacted by industry-specific factors, particularly the continued development of AI (including advancements in AI technology that may lead to further compute efficiencies), the broader adoption, use, and commercialization of AI and any impacts of the developing AI regulatory environment.

As many of these factors are beyond Boost Run’s control, it is difficult for it to accurately forecast its future operating results. If the assumptions that Boost Run uses to plan its business are incorrect or change in reaction to changes in its market, it may be unable to maintain consistent revenue or revenue growth, the value of its stock could be volatile, and it may be difficult to achieve and, if achieved, maintain profitability. In addition, changes in the macroeconomic environment, including actual or perceived global banking and finance related issues, domestic and foreign regulatory uncertainty, changes in trade policies (including the imposition of tariffs, trade controls and other trade barriers), labor shortages, supply chain disruptions, volatile interest rates and inflation, spending environments, geopolitical instability, warfare and uncertainty, including the effects of the conflicts in the Middle East and Ukraine and tensions between China and Taiwan, weak economic conditions in certain regions, or a reduction in AI spending regardless of macroeconomic conditions may impact Boost Run’s growth.

In addition, as Boost Run has grown, its number of customers has also increased, and it has increasingly managed more complex deployments of its infrastructure in more complex computing environments. The rapid growth and expansion of Boost Run’s business places a significant strain on its management, operational, engineering, and financial resources. To manage any future growth effectively, Boost Run must continue to improve and expand its infrastructure, including information technology (“IT”) and financial infrastructure, its operating and administrative systems and controls, and its ability to manage headcount, capital, and processes in an efficient manner.

If Boost Run does not manage future growth effectively, its business, operating results, financial condition, and prospects would be harmed. If Boost Run continues to experience rapid growth, it may not be able to successfully implement or scale improvements to its systems, processes, and controls in an efficient, timely, or cost-effective manner. As Boost Run grows, its existing systems, processes, and controls may not prevent or detect all errors, omissions, or fraud. Any future growth will continue to add complexity to Boost Run’s organization and require effective coordination throughout its organization. Failure to manage any future growth effectively could result in increased costs, cause difficulty or delays in deploying Boost Run’s platform to new and existing customers, reduce demand for its platform, and cause difficulties in introducing new solutions and services or other operational difficulties, and any of these difficulties would adversely affect its business, operating results, financial condition, and prospects.

Boost Run has a limited number of suppliers for significant components of the equipment it uses to build and operate its platform and provide its solutions and services. Any disruption in the availability of these components could delay Boost Run’s ability to expand or increase the capacity of its infrastructure or replace defective equipment.

Boost Run does not manufacture the components it uses to build the technology infrastructure underlying its platform. Boost Run has a limited number of suppliers that it uses to procure and configure significant components of the technology infrastructure that it uses to operate its platform and provide its solutions and services to its customers. Utilizing a limited number of suppliers of the components for Boost Run’s technology infrastructure exposes it to risks, including:

| ● | asymmetry between component availability and contractual performance obligations, including where specified components are required; | |

| ● | shifts in market-leading technologies away from those offered by its current suppliers that could impact its ability to offer its customers the solutions and services that they are seeking; |

| 14 |

| ● | reduced control over production costs and constraints based on the then current availability, terms, and pricing of these components, including any delays in its supply chain; | |

| ● | limited ability to control aspects of the quality, performance, quantity, and cost of its infrastructure or of its components; | |

| ● | the potential for binding price or purchase commitments with its suppliers at higher than market rates; |

| ● | reliance on its suppliers to keep up with technological advancements at the same pace as its business and customer demands, including their ability to continue to deliver next generation components that are substantially better than the prior generation; | |

| ● | consolidation among suppliers in its industry, which may harm its ability to negotiate and obtain favorable terms from its suppliers and the third-party suppliers that its suppliers rely on; | |

| ● | labor and political unrest at facilities it does not operate or own; | |

| ● | geopolitical disputes disrupting its or any of its suppliers’ supply chains; | |

| ● | business, legal compliance, litigation, and financial concerns affecting its suppliers or their ability to manufacture and ship components in the quantities, quality, and manner Boost Run requires; | |

| ● | impacts on its supply chain from adverse public health developments, including outbreaks of contagious diseases or pandemics; and | |

| ● | disruptions due to floods, earthquakes, storms, and other natural disasters, particularly in countries with limited infrastructure and disaster recovery resources, or regional conflicts. |

Boost Run’s technology infrastructure components suppliers fulfill its supply requirements on the basis of individual purchase orders, which it often places on a just-in-time basis. Boost Run currently has no long-term contracts or arrangements with its suppliers that guarantee capacity or the continuation of any particular payment terms. Accordingly, Boost Run’s suppliers are not obligated to continue to fulfill its supply requirements, and the prices it is charged for its products and, if applicable, services could be increased on short notice. Further, because Boost Run often submits purchase orders to its suppliers on a just-in-time basis, any delay from its suppliers may result in its inability to provide its infrastructure and platform to its customers on a timely basis and fulfill its contractual requirements under its customer contracts. If Boost Run is required to change suppliers, its ability to meet its obligations to its customers, including scheduled compute access, could be adversely affected and its solutions may not be as performant, which could cause the loss of sales from existing or potential customers, delayed revenue, or an increase in its costs, which could adversely affect its margins. Any production or shipping interruptions for any reason, such as a natural disaster, epidemics, pandemics, capacity shortages, quality problems, or strike or other labor disruption at one of Boost Run’s supplier locations or at shipping ports or locations, could adversely affect sales of its solution and services offerings.

In addition, Boost Run is continually working to expand and enhance its infrastructure features, technology, and network and other technologies to accommodate substantial increases in the computing power required by more compute-intensive workloads on its platform, the amount of data it hosts, and its overall number of total customers. Boost Run may be unable to project accurately the rate or timing of these increases or to allocate resources successfully to address such increases and may underestimate the data center capacity needed to address such increases. Boost Run’s limited number of suppliers, in turn, may not be able to quickly respond to its needs, which would have a negative impact on customer experience and contractual performance. In the future, Boost Run may be required to allocate additional resources, including spending substantial amounts, to build, purchase, or lease or license data centers and equipment and upgrade its technology and network infrastructure in order to handle increased customer usage, and its suppliers may not be able to satisfy such requirements. In addition, Boost Run’s network or its suppliers’ networks might be unable to achieve or maintain data transmission capacity high enough to effectively deliver its services. Boost Run may also face constraints on its ability to deliver its platform, solutions, and services if there is limited power supply. Boost Run’s failure, or its suppliers’ failure, to achieve or maintain high data transmission capacity and sufficient electrical services would impact its ability to meet customer needs and could significantly reduce consumer demand for its services. Such reduced demand and resulting loss of compute, cost increases, or failure to upgrade its equipment or adapt to new technologies would harm its business, operating results, financial condition, and prospects.

| 15 |

Moreover, Boost Run’s suppliers themselves rely on a complex network of third-party suppliers for semiconductor manufacturing, hardware components, and other critical inputs, which introduces additional risks to its supply chain. For example, NVIDIA relies on suppliers such as Taiwan Semiconductor Manufacturing Company for semiconductor fabrication and other manufacturers for compute and networking components. Any disruption in the operations of these upstream suppliers, whether due to equipment failures, geopolitical factors such as the potential for military conflict between China and Taiwan, or supply chain constraints, could affect Boost Run’s suppliers’ ability to supply the significant components of the equipment it uses to operate its platform and provide its solutions and services to its customers, which would, in turn, affect the availability of its solutions and services, as well as lead times.

In addition, to the extent any of Boost Run’s suppliers’ businesses are impacted by business, legal compliance, litigation, and financial concerns, including regulatory scrutiny and export controls, its business, operating results, financial condition, and prospects may be adversely affected. For example, increasing use of tariffs, economic sanctions and export controls has impacted and may in the future impact the availability and cost of GPUs and other components of Boost Run’s platform. The current U.S. presidential administration has discussed imposing broadbased tariffs on imported goods, which, if implemented on components of Boost Run’s infrastructure and other products it uses, could increase its costs. Further, the former U.S. presidential administration had recently released new export controls targeting semiconductor manufacturing equipment and other items related to advanced integrated circuits. It is possible that these and additional restrictions could impede the supply chain in this industry. Additional export restrictions imposed on components of Boost Run’s technologies by the U.S. government may also provoke responses from foreign governments that negatively impact its supply chain, increase the costs for affected imported goods, or limit its ability to obtain additional hardware components, which would also substantially reduce its ability to provide or develop its platform, solutions, and services.

In the event of a supplier unavailability, component shortage, or supply interruption, Boost Run may not be able to secure alternate sources in a timely manner. Securing alternate sources of supply for these components or services may be time-consuming, difficult, and costly and Boost Run may not be able to source these components or services on terms that are acceptable to it, or at all, which may undermine its ability to fill its orders in a timely manner. Any interruption or delay in the supply of any of these components or services, or the inability to obtain these components or services from alternate sources at acceptable prices and within a reasonable amount of time, would harm Boost Run’s ability to meet the demand of its customers, which in turn would have an adverse effect on its business, operating results, financial condition, and prospects.

Boost Run’s business would be harmed if it were not able to access sufficient power or by increased costs to procure power, prolonged power outages, shortages, or capacity constraints.

Boost Run depends on being able to secure power, which powers its data center facilities, in a cost-effective manner. Boost Run’s inability to secure sufficient power or any power outages, shortages, supply chain issues, capacity constraints, or significant increases in the cost of securing power could have an adverse effect on its business, operating results, financial condition, and prospects.

Boost Run relies on third parties to provide enough power to maintain its leased data center facilities and meet the needs of its current and future customers. Boost Run has in the past experienced, and it may in the future experience, insufficient power to service a customer’s project. Any limitation on the delivered energy supply would limit Boost Run’s ability to operate its platform. These limitations would have a negative impact on a given data center or limit Boost Run’s ability to grow its business which could negatively affect its business, operating results, financial condition, and prospects. Limitations on generation, transmission, and distribution may also limit its ability to obtain sufficient power capacity for potential expansion sites in new or existing markets. Power providers, other participants in the power market, and those entities that regulate it may impose onerous operating conditions to any approval or provision of power or Boost Run may experience significant delays and substantial increased costs to provide the level of electrical service required by its current or future leased or licensed data centers, or any data centers it may choose to construct in the future. Boost Run’s ability to find appropriate sites for expansion, including existing sites to lease, will also be limited by access to power.

| 16 |

Boost Run’s leased data center facilities are affected by problems accessing electricity sources, such as planned or unplanned power outages and limitations on transmission or distribution of power. Unplanned power outages, including, but not limited to those relating to large storms, earthquakes, fires, tsunamis, cyberattacks, physical attacks on utility infrastructure, war, and any failures of electrical power grids more generally, and planned power outages by public utilities, could harm Boost Run’s customers and its business. Further, Boost Run’s leased data center facilities are located in leased buildings where, depending upon the lease requirements and number of tenants involved, it may or may not control some or all of the infrastructure, including generators and fuel tanks. As a result, in the event of a power outage, Boost Run could be dependent upon the landlord, as well as the utility company, to restore the power. Even if Boost Run attempts to limit its exposure to system downtime by using backup generators, which are in turn supported by onsite fuel storage and through contracts with fuel suppliers, these measures may not always prevent downtime or solve for long-term or large-scale outages. Any outage or supply disruption could adversely affect Boost Run’s customer experience, as well as its business, operating results, financial condition, and prospects.

The global energy market is currently experiencing inflation and volatility pressures. Various macroeconomic and geopolitical factors are contributing to the instability and global power shortage, including the war in Ukraine, severe weather events, governmental regulations, government relations, and inflation. Boost Run expects the cost for power to continue to be volatile and unpredictable and subject to inflationary pressures, which could materially affect its financial forecasting, business, operating results, financial condition, and prospects.

Boost Run depends entirely on third-party partners, including data center operators, to host Boost Run’s GPU infrastructure and provide various services in support of its business, and any disruption to these relationships or the performance of these partners could materially harm Boost Run’s business, financial condition, and results of operations.

Boost Run does not own or operate data centers. Instead, Boost Run relies exclusively on third-party colocation providers to house, power, cool, and provide connectivity to Boost Run’s GPU servers and infrastructure. Boost Run also relies on third-party partners to provide various services in support of its business, including hardware delivery, installation, service and technical support, as well as the provision of equipment and personnel. If a local partner is unwilling or unable to deliver its services for any reason including, but not limited to, a dispute with Boost Run, the deterioration of its financial condition or a loss of personnel, Boost Run may be unable to engage an alternative partner or subcontractors to perform the same services, or on terms substantially similar to those with its existing partners. The failure to do so may cause Boost Run to breach the terms of existing contracts, impede its ability to complete orders, and/or result in damage to its customer relationships, any of which may damage Boost Run’s reputation and have a material adverse effect on its business and results of operations.

Boost Run’s business model requires Boost Run to deploy significant capital investment in GPU equipment that Boost Run installs in facilities controlled by third parties. If any of Boost Run’s colocation partners experience financial distress, operational difficulties, or elects to terminate or not renew their agreements with Boost Run, Boost Run could lose access to the facilities housing Boost Run’s equipment. Such a loss of access could result in:

| ● | Immediate service disruptions to Boost Run’s customers; | |

| ● | Breach of Boost Run’s customer service level agreements and contractual obligations; | |

| ● | Significant costs to relocate equipment to alternative facilities; | |

| ● | Extended downtime during equipment migration, resulting in lost revenue; | |

| ● | Physical damage to equipment during relocation; | |

| ● | Inability to recover equipment if colocation partner enters bankruptcy or receivership; | |

| ● | Stranded capital if equipment cannot be economically relocated; | |

| ● | Customer attrition and reputational damage; and | |

| ● | Litigation from customers whose services are disrupted. |

| 17 |

The number of data center facilities with sufficient power capacity, cooling capabilities, and network infrastructure to support high-density GPU deployments is limited, particularly as demand for AI infrastructure has increased substantially. Boost Run may rely on a concentrated number of colocation partners, and the loss of any single major partner relationship could have a disproportionate impact on Boost Run’s business. If Boost Run is unable to secure alternative colocation capacity on acceptable terms, or at all, Boost Run may be unable to fulfill commitments to existing customers or pursue new business opportunities.